Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:HE

Is Hawaiian Electric Industries (NYSE:HE) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Hawaiian Electric Industries, Inc. (NYSE:HE) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Hawaiian Electric Industries

What Is Hawaiian Electric Industries's Debt?

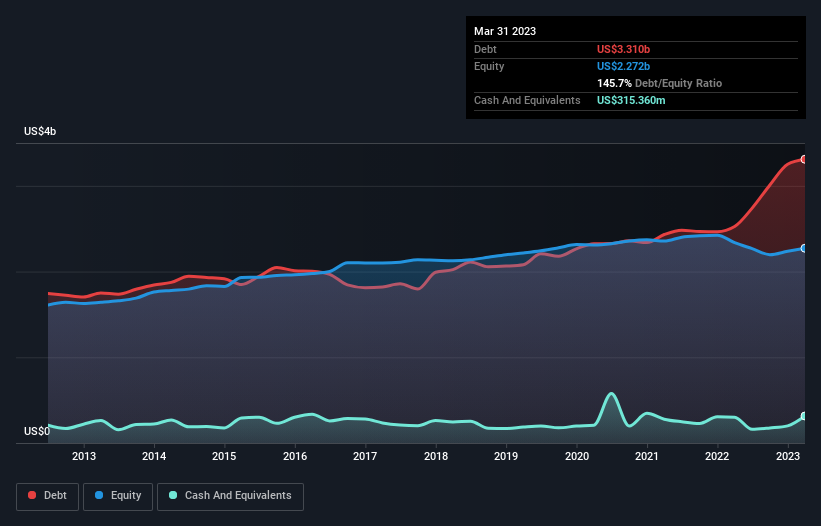

The image below, which you can click on for greater detail, shows that at March 2023 Hawaiian Electric Industries had debt of US$3.31b, up from US$2.52b in one year. On the flip side, it has US$315.4m in cash leading to net debt of about US$3.00b.

How Strong Is Hawaiian Electric Industries' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hawaiian Electric Industries had liabilities of US$1.11b due within 12 months and liabilities of US$13.1b due beyond that. Offsetting this, it had US$315.4m in cash and US$6.42b in receivables that were due within 12 months. So its liabilities total US$7.43b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$3.96b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Hawaiian Electric Industries would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hawaiian Electric Industries's debt is 4.4 times its EBITDA, and its EBIT cover its interest expense 3.5 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Even more troubling is the fact that Hawaiian Electric Industries actually let its EBIT decrease by 3.1% over the last year. If it keeps going like that paying off its debt will be like running on a treadmill -- a lot of effort for not much advancement. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hawaiian Electric Industries can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Hawaiian Electric Industries recorded free cash flow of 30% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

We'd go so far as to say Hawaiian Electric Industries's level of total liabilities was disappointing. But at least its EBIT growth rate is not so bad. We should also note that Electric Utilities industry companies like Hawaiian Electric Industries commonly do use debt without problems. Overall, it seems to us that Hawaiian Electric Industries's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Hawaiian Electric Industries is showing 3 warning signs in our investment analysis , and 1 of those is a bit concerning...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Hawaiian Electric Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HE

Hawaiian Electric Industries

Engages in the electric utility business in the United States.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor