- United States

- /

- Electric Utilities

- /

- NYSE:ETR

Benign Growth For Entergy Corporation (NYSE:ETR) Underpins Its Share Price

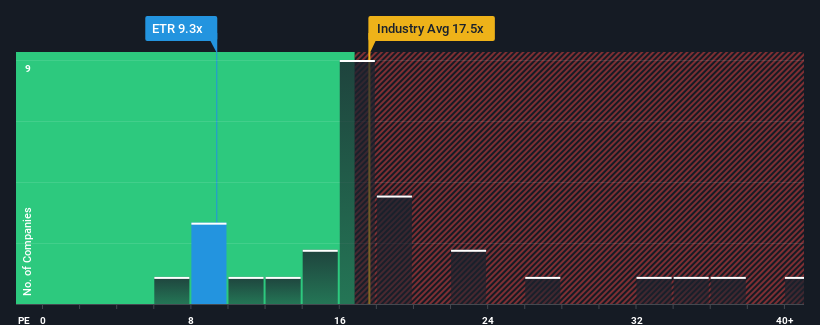

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 17x, you may consider Entergy Corporation (NYSE:ETR) as an attractive investment with its 9.3x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Entergy as its earnings have risen in spite of the market's earnings going into reverse. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Entergy

Is There Any Growth For Entergy?

There's an inherent assumption that a company should underperform the market for P/E ratios like Entergy's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 106%. The strong recent performance means it was also able to grow EPS by 59% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the analysts covering the company suggest earnings growth is heading into negative territory, declining 9.1% per year over the next three years. With the market predicted to deliver 10% growth each year, that's a disappointing outcome.

In light of this, it's understandable that Entergy's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Entergy's P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Entergy's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 4 warning signs for Entergy you should be aware of, and 2 of them don't sit too well with us.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Entergy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ETR

Entergy

Engages in the production and retail distribution of electricity in the United States.

Slight second-rate dividend payer.

Similar Companies

Market Insights

Community Narratives