Advertisement

- United States

- /

- Other Utilities

- /

- NYSE:AEE

Is Ameren Still Attractive After Its 12% 2025 Rally?

Simply Wall St

Reviewed by Bailey Pemberton

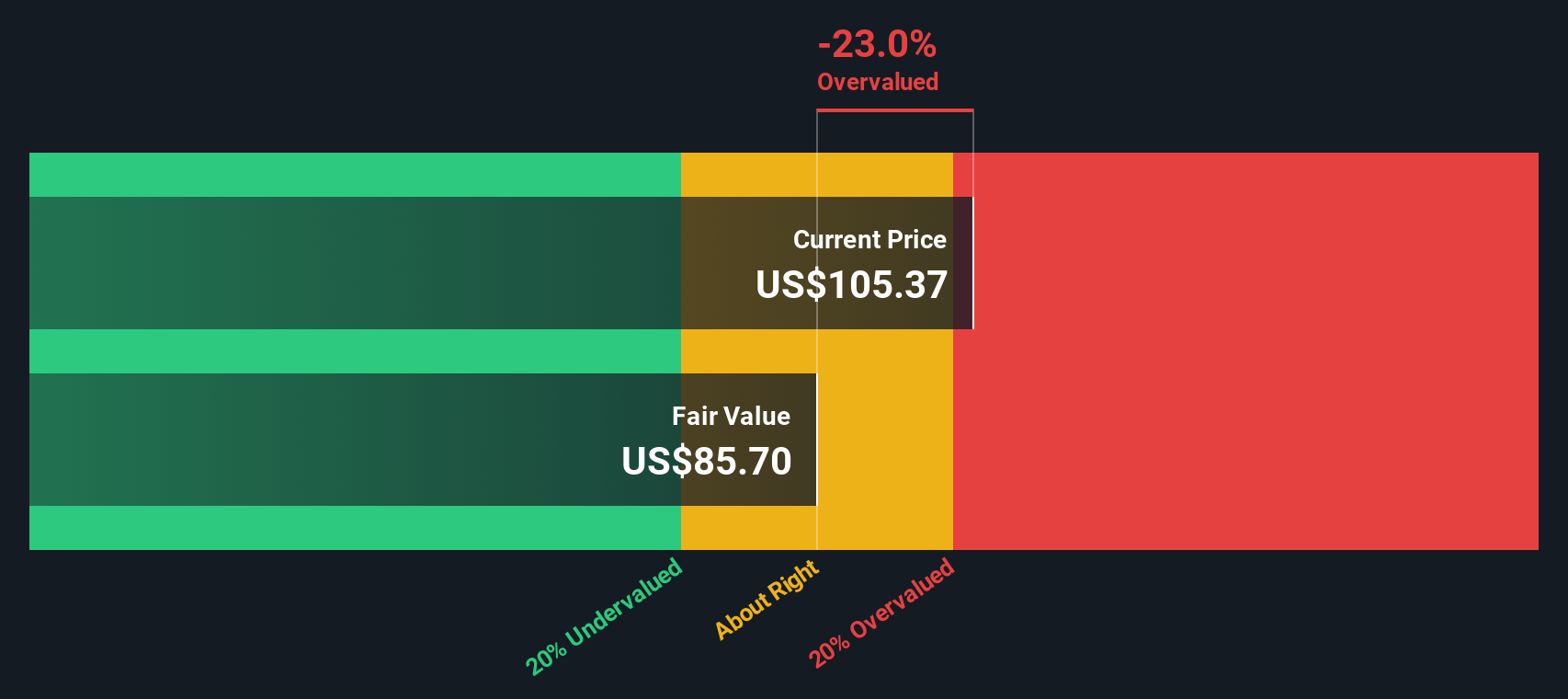

- If you are wondering whether Ameren is still worth buying after its recent run, you are not alone. This article will walk through what the current share price really implies.

- The stock is up 12.2% year to date and 12.0% over the last year, even after a recent 6.1% pullback over the past week and a softer 1.4% dip across the last 30 days.

- Investors have been responding to a mix of regulatory decisions, long term grid modernization plans and accelerating investment in renewable and transmission projects, all of which shape expectations for Ameren's future cash flows. At the same time, shifting sentiment toward defensive utilities as interest rate expectations evolve has added another layer of momentum and risk perception around the stock.

- On our checks, Ameren currently earns a 2/6 valuation score. This suggests that while it screens as undervalued on some metrics, other measures are more demanding and need a closer look. Next we will unpack those different valuation approaches before circling back at the end to a more complete way of thinking about what the stock is really worth.

Ameren scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ameren Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what a stock is worth by projecting all future dividends and discounting them back to today, then comparing that value with the current share price.

For Ameren, the model starts with an annual dividend per share of about $3.16. The company earns a return on equity of roughly 10.4% and pays out about 58% of its earnings as dividends, which leaves room to reinvest and support future growth. Simply Wall St caps Ameren’s long term dividend growth at 3.26%, slightly lower than the 4.41% that might be implied by recent trends to avoid being overly optimistic.

Using those assumptions, the DDM produces an intrinsic value of roughly $85.40 per share. That output compares with the current market price and indicates that investors today may be paying a premium for Ameren’s dividend stream and expected growth.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests Ameren may be overvalued by 16.9%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

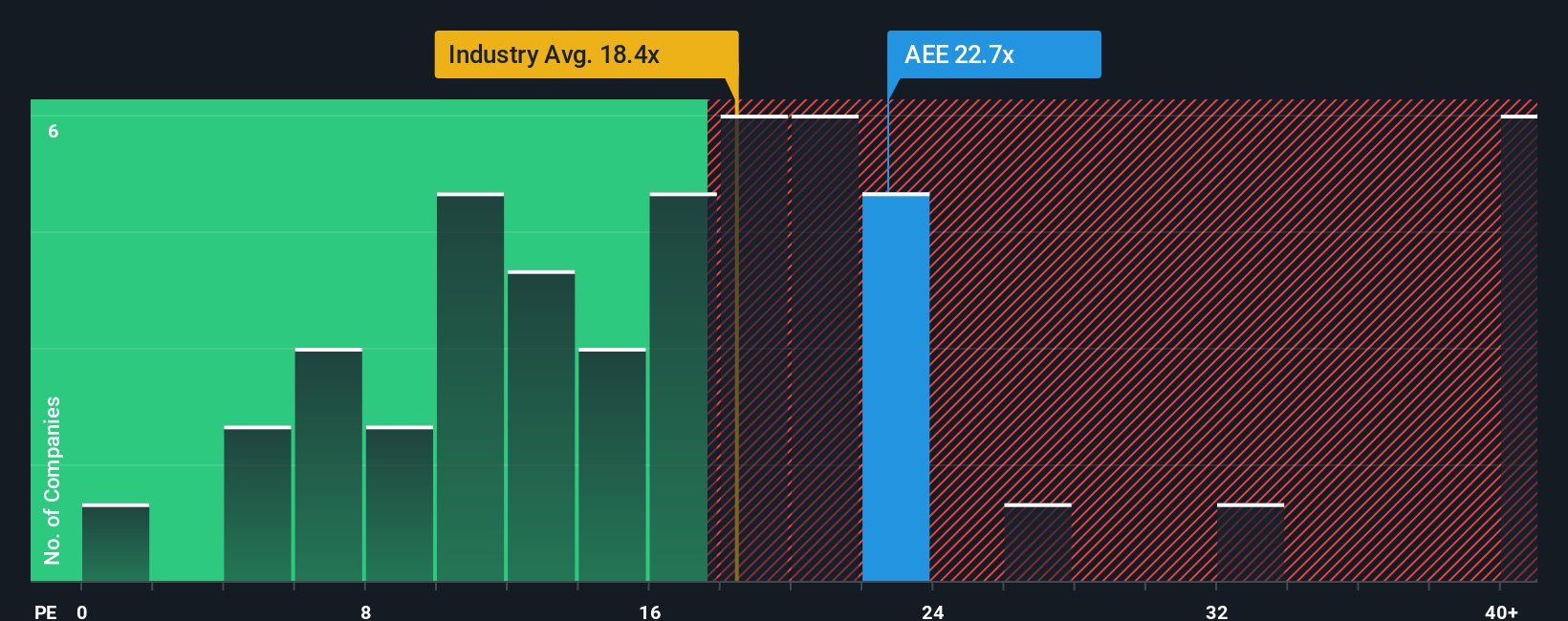

Approach 2: Ameren Price vs Earnings

For a mature, profitable utility like Ameren, the price to earnings (PE) ratio is a sensible yardstick because earnings are relatively stable and closely tied to its regulated asset base and allowed returns. Investors typically pay higher PE multiples when they expect faster, more reliable growth or see lower risk in a company’s cash flows, and they demand lower multiples when growth looks slower or riskier.

Ameren currently trades on a PE of about 19.14x. That sits above the Integrated Utilities industry average of roughly 17.80x, but below the 21.02x average of its listed peers. Simply Wall St’s Fair Ratio framework goes a step further by estimating what Ameren’s PE should be, given its earnings growth profile, profit margins, risk factors, industry and market cap. On this basis, Ameren’s Fair Ratio is 22.43x, which indicates that investors might reasonably be willing to pay a higher multiple than today’s market price reflects.

Because Ameren’s actual PE of 19.14x is meaningfully below the 22.43x Fair Ratio, the shares screen as undervalued on this preferred multiple approach.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ameren Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Ameren’s story with a financial forecast and a fair value estimate that you can easily compare with today’s share price. A Narrative is your version of the company’s future, where you plug in assumptions about revenue growth, earnings, margins and risk, and see how those beliefs translate into a fair value per share. On Simply Wall St’s Community page, used by millions of investors, Narratives turn these inputs into a live valuation that updates dynamically when fresh news, earnings or guidance arrives. This means your view can evolve as new information emerges. For Ameren, one bullish Narrative might lean on accelerating data center and electrification demand, strong regulatory support and rising margins to justify a fair value closer to $121. A more cautious Narrative might stress regulatory and execution risks, slower load growth and tighter returns to arrive nearer $90. This gives you a clear, number backed way to decide which story you believe and how the current price stacks up.

Do you think there's more to the story for Ameren? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AEE

Ameren

Operates as a public utility holding company in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative