- United States

- /

- Transportation

- /

- NYSE:UNP

Union Pacific (UNP): Reassessing Valuation After a Steady Share Price Grind Higher

Reviewed by Simply Wall St

Understanding the recent move in Union Pacific

Union Pacific (UNP) has quietly added to its gains over the past month, and with the stock now trading around 4% above its recent levels, investors are reassessing what they are actually paying for.

See our latest analysis for Union Pacific.

That recent 1 month share price return of 3.71% nudges Union Pacific a bit higher in what has otherwise been a steady grind, with a 1 year total shareholder return of 5.76% and a 3 year total shareholder return of 19.92%. This suggests momentum is positive rather than explosive at this stage.

If this kind of measured momentum appeals, it might be worth widening your watchlist to see how other industrial transport names stack up against growth focused plays like fast growing stocks with high insider ownership.

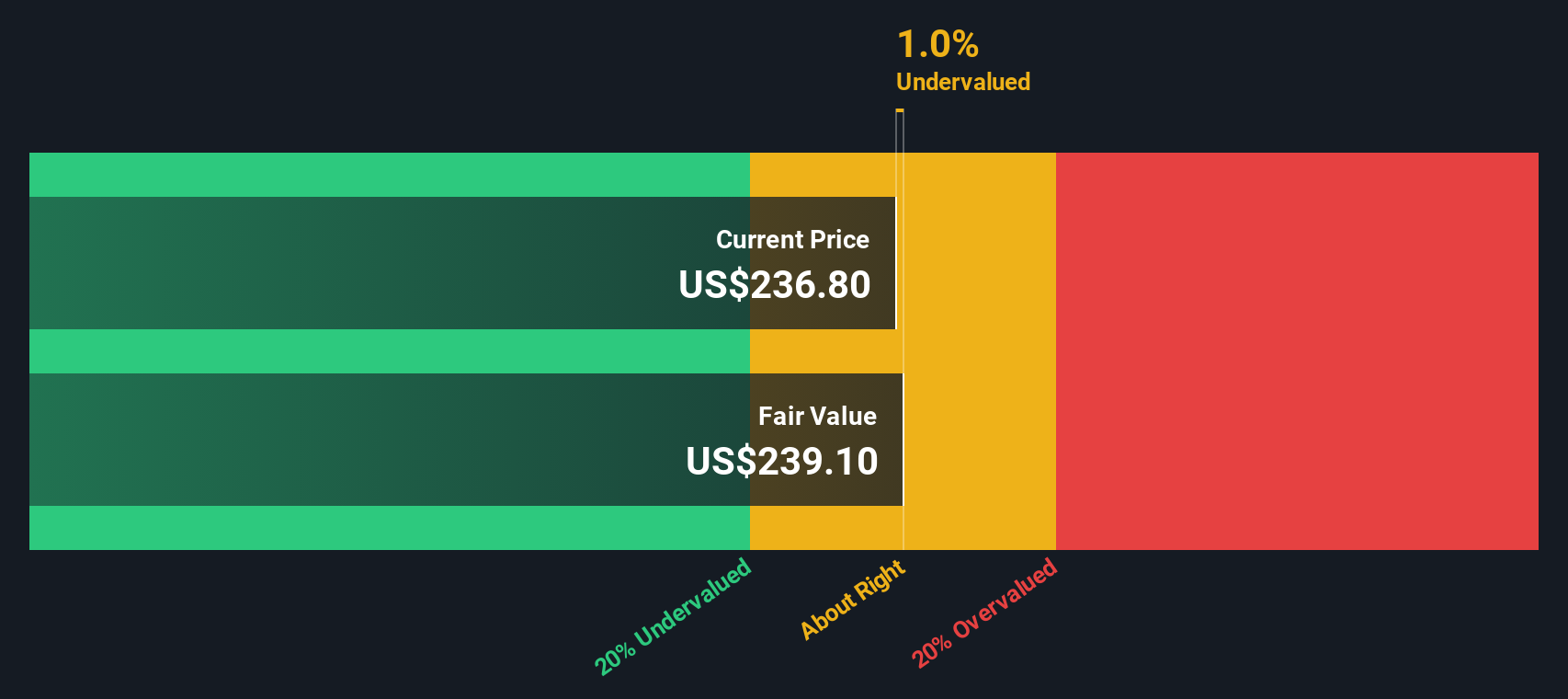

With shares modestly ahead of analyst targets and only a slight intrinsic premium implied, the key question is whether Union Pacific is quietly trading below its true value or if the market has already priced in its next leg of growth.

Most Popular Narrative: 9.8% Undervalued

With Union Pacific closing at $234.61 versus a narrative fair value near $260, the story behind that gap hinges on specific long term assumptions.

The analysts have a consensus price target of $256.92 for Union Pacific based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $294.0, and the most bearish reporting a price target of just $213.0.

Want to see what is powering that upside gap? The narrative leans on steady volume gains, firmer margins, and a richer future earnings multiple. Curious which assumptions really move the needle?

Result: Fair Value of $260.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, lingering uncertainty around trade policy and softer intermodal volumes could quickly challenge the upside case if demand fails to rebound as expected.

Find out about the key risks to this Union Pacific narrative.

Another Way to Look at Value

Our DCF view is slightly more conservative than the narrative fair value, with Union Pacific trading a bit above our estimate of fair value at $229.74. Rather than looking extremely cheap, this suggests a limited margin of safety. Is the market already paying a premium for execution and consolidation hopes?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Union Pacific for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 898 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Union Pacific Narrative

If you see the story differently or simply want to dig into the numbers yourself, you can build a custom narrative in minutes: Do it your way.

A great starting point for your Union Pacific research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Before you move on, lock in an edge by using the Simply Wall St Screener to uncover fresh ideas that match your goals and risk appetite.

- Strengthen your portfolio by targeting reliable income streams through these 11 dividend stocks with yields > 3% that can help anchor returns when markets turn volatile.

- Capitalize on structural growth in digital assets with these 79 cryptocurrency and blockchain stocks that highlight businesses building real value around blockchain and decentralised technology.

- Position ahead of the next wave of innovation by using these 28 quantum computing stocks focused on companies pushing boundaries in computing power and real world problem solving.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UNP

Union Pacific

Through its subsidiary, Union Pacific Railroad Company, operates in the railroad business in the United States.

Solid track record established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion