- United States

- /

- Logistics

- /

- NYSE:EXPD

Expeditors International of Washington (NYSE:EXPD) CEO Transition 발표

Reviewed by Simply Wall St

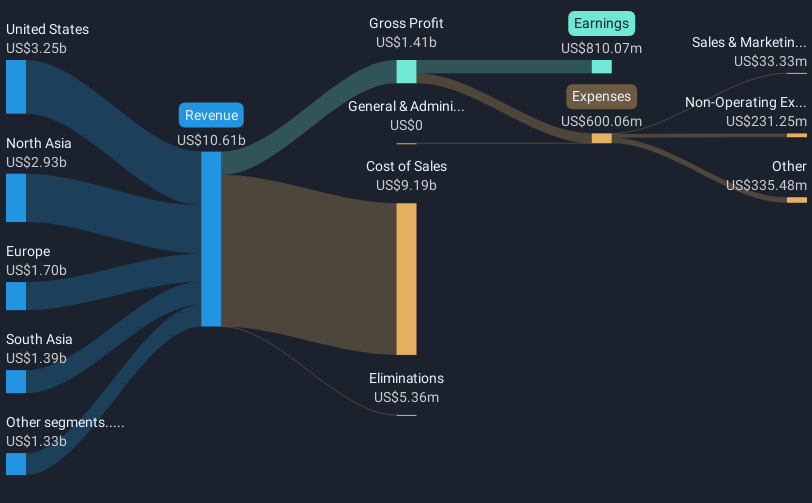

Expeditors International of Washington (NYSE:EXPD) announced the upcoming retirement of CEO Jeffrey S. Musser and the appointment of Daniel R. Wall as his successor. This leadership transition, alongside a strong earnings report showing increased revenue and net income, initially seemed positive for the company. However, despite these developments, Expeditors' stock price decreased by 9% last quarter. This decline aligns with broader market volatility, notably fueled by global trade uncertainties and escalating tariffs, which overshadowed company-specific events. The share buyback activity likely cushioned larger declines, but the market's overall downward trend dictated performance.

Despite the recent dip in Expeditors International of Washington's stock price, the company has delivered a total return of 54.30% over the past five years. This performance reflects its ability to provide value to shareholders through dividends and share price appreciation. When comparing its recent one-year performance, which lagged behind the US market's decline of 3.8%, the longer-term results suggest a more resilient investment over the extended period.

Considering the fluctuations in revenue and earnings, recent executive changes and positive earnings reports tend to support future growth forecasts. However, global trade uncertainties continue to pose potential risks, which may weigh on revenue and earnings projections. Meanwhile, the share price, currently at a discount to the consensus analyst price target of US$115.54, indicates potential room for upward movement. While the company trades at a premium compared to the Global Logistics industry average, its historical performance and lower P/E ratio relative to peers highlight its strength as an investment in the logistics sector.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Expeditors International of Washington, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Expeditors International of Washington might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EXPD

Expeditors International of Washington

Provides logistics services in the Americas, North Asia, South Asia, Europe, and MAIR.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives