Advertisement

Airlines might be complicated long-term investments, but they are dear to short-term speculators – as evident from Delta Air Lines, Inc.'s (NYSE: DAL) short-term volatility.

After losing over 30% in a few weeks, the stock rallied back up on a favorable sentiment shift, solid earnings results, and strong fuel cost management.

See our latest analysis for Delta Air Lines

Q1 2022 Earnings Results

- US$1.48 loss per share (from US$1.85 loss in 1Q 2021).

- Revenue: US$9.35b (up 125% from 1Q 2021).

- Net loss: US$940.0m (loss narrowed 20% from 1Q 2021).

Revenue exceeded analyst estimates by 3.5%. Earnings per share (EPS) missed analyst estimates by 13%.

Over the next year, revenue is forecast to grow 36%, compared to a 44% growth forecast for the industry in the US. Over the last 3 years, on average, earnings per share have fallen by 56% per year, but its share price has only decreased by 10% per year, which means it has not declined as severely as earnings.

Boeing Orders Speculations and Institutional Optimism

After years of preferring Airbus over Boeing, Delta is reportedly close to ordering up to 100 737 MAX 10 jets. This would be a big win for Boeing, which had a somewhat strained relationship with the airliner throughout the last decade. Especially at this moment, after Boeing had to move 141 orders into accounting limbo due to the Russian-Ukrainian war and escalating sanctions.

Meanwhile, institutions set an optimistic tone after the latest earnings results:

- Barclays: Upgrade to Overweight (from Equal Weight) quoting rapid recovery in travel demand and near-recovery to pre-pandemic levels. The price target is set at US$60.

- JPMorgan: Upgraded price target to US$69 (from US$57), quoting strong Q2 guidance exceeding the most optimistic forecast, as well as fuel savings from refinery ownership

Our Take on Delta's Intrinsic Value

For this purpose, we will use the Discounted Cash Flow (DCF) model. We would caution that there are many ways of valuing a company, and, like the DCF, each technique has advantages and disadvantages in specific scenarios. Anyone interested in learning a bit more about intrinsic value should have a read of the Simply Wall St analysis model.

We use what is known as a 2-stage model, which means we have two different periods of growth rates for the company's cash flows. Generally, the first stage is higher growth, and the second stage is a lower growth phase. To begin with, we have to get estimates of the next ten years of cash flows. A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we need to discount the sum of these future cash flows to arrive at a present value estimate:

10-year free cash flow (FCF) forecast

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | -US$258.8m | US$2.02b | US$3.19b | US$4.29b | US$3.78b | US$3.49b | US$3.33b | US$3.24b | US$3.19b | US$3.18b |

| Growth Rate Estimate Source | Analyst x5 | Analyst x7 | Analyst x4 | Analyst x3 | Analyst x1 | Est @ -7.57% | Est @ -4.73% | Est @ -2.73% | Est @ -1.34% | Est @ -0.36% |

| Present Value ($, Millions) Discounted @ 7.3% | -US$241 | US$1.7k | US$2.6k | US$3.2k | US$2.7k | US$2.3k | US$2.0k | US$1.8k | US$1.7k | US$1.6k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$19b

The second stage is also known as Terminal Value. This is the business's cash flow after the first stage. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 1.9%. We discount the terminal cash flows to today's value at the cost of equity of 7.3%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r – g) = US$3.2b× (1 + 1.9%) ÷ (7.3%– 1.9%) = US$60b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$60b÷ ( 1 + 7.3%)10= US$30b

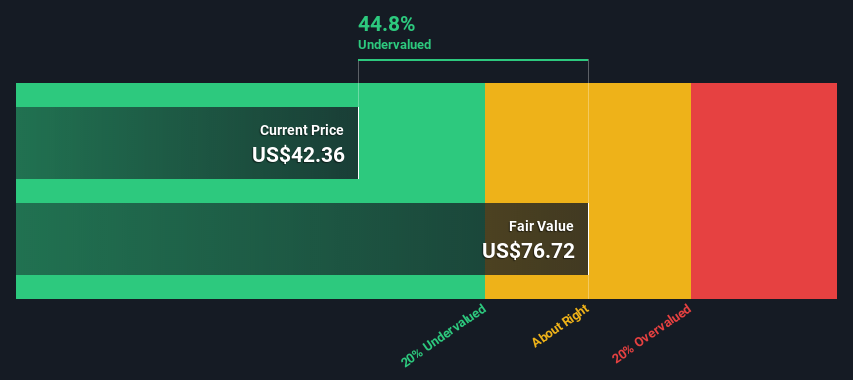

The total value is the sum of cash flows for the next ten years plus the discounted terminal value, which results in the Total Equity Value, which in this case is US$49b. The last step is to divide the equity value by the number of shares outstanding.

Compared to the current share price of US$42.4, the company appears relatively undervalued at a 45% discount to where the stock price trades currently.

Important assumptions

The calculation above is very dependent on two assumptions. The first is the discount rate, and the other is the cash flow.

The DCF does not consider the possible cyclicality of an industry or its future capital requirements, so it does not give a complete picture of a company's potential performance. Given that we are looking at Delta Air Lines as potential shareholders, the cost of equity is used as the discount rate rather than the cost of capital (or the weighted average cost of capital, WACC), which accounts for debt. We've used 7.3% in this calculation based on a levered beta of 1.275. Beta is a measure of a stock's volatility compared to the market.

Moving On:

While fuel prices seem to weigh on carriers, Delta seems confident in its ability to recover the fuel price run-up. This puts them in a unique position to profit from the sector's strong recovery. Furthermore, Boeing's pressure due to Russian sanctions put them in an excellent negotiation position to secure a good deal.

With those factors built into the analyst expectations, we're not surprised to see our intrinsic value calculation land in the same ballpark as those mentioned institutions.

Yet, the DCF calculation shouldn't be the only metric you look at when researching a company. For Delta Air Lines, we've put together three additional items you should assess:

- Risks: Every company has them, and we've spotted 4 warning signs for Delta Air Lines (of which 1 can't be ignored!) you should know about.

- Future Earnings: How does DAL's growth rate compare to its peers and the broader market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other High-Quality Alternatives: Do you like a good all-rounder? Explore our interactive list of high quality stocks to get an idea of what else is out there you may be missing!

PS. Simply Wall St updates its DCF calculation for every American stock every day, so if you want to find the intrinsic value of any other stock just search here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:DAL

Delta Air Lines

Provides scheduled air transportation for passengers and cargo in the United States and internationally.

Good value with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor