Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:SAIA

Can Saia’s (SAIA) Margin Pressures Shift Its Network Expansion Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Rothschild Redburn initiated coverage on Saia Inc. with a Neutral rating and highlighted the company's ongoing network expansion and robust five-year revenue growth trajectory, while also noting recent margin pressures.

- An interesting insight is that, despite margin challenges from accepting lower-quality shipments, Saia exceeded third-quarter 2025 earnings forecasts, reflecting operational strength in a competitive transportation market.

- We will explore how the recent analyst coverage and earnings beat could influence Saia's margin outlook and investment narrative going forward.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Saia Investment Narrative Recap

To be a shareholder in Saia, you have to believe in the company’s ability to successfully scale its national terminal network and unlock efficiencies that outweigh near-term cost and margin pressures. The recent Neutral rating from Rothschild Redburn and ongoing margin concerns have not materially shifted the short-term catalyst, which remains the maturation and ramp-up of newly opened terminals; however, margin degradation due to network expansion continues to present the biggest risk right now.

Among recent developments, Saia’s third-quarter 2025 earnings beat stands out as most relevant: despite margin pressures and flat sales, the company exceeded analyst expectations for both adjusted EPS and revenue. This suggests operational resilience that could support its ongoing expansion story, even as competitive pressures and cost challenges remain in focus for the months ahead.

Yet, on the other hand, investors should not ignore the persistent earnings pressures tied to rising costs and underutilized new facilities...

Read the full narrative on Saia (it's free!)

Saia's narrative projects $3.9 billion revenue and $456.7 million earnings by 2028. This requires 6.6% yearly revenue growth and a $166.6 million earnings increase from $290.1 million today.

Uncover how Saia's forecasts yield a $323.37 fair value, a 16% upside to its current price.

Exploring Other Perspectives

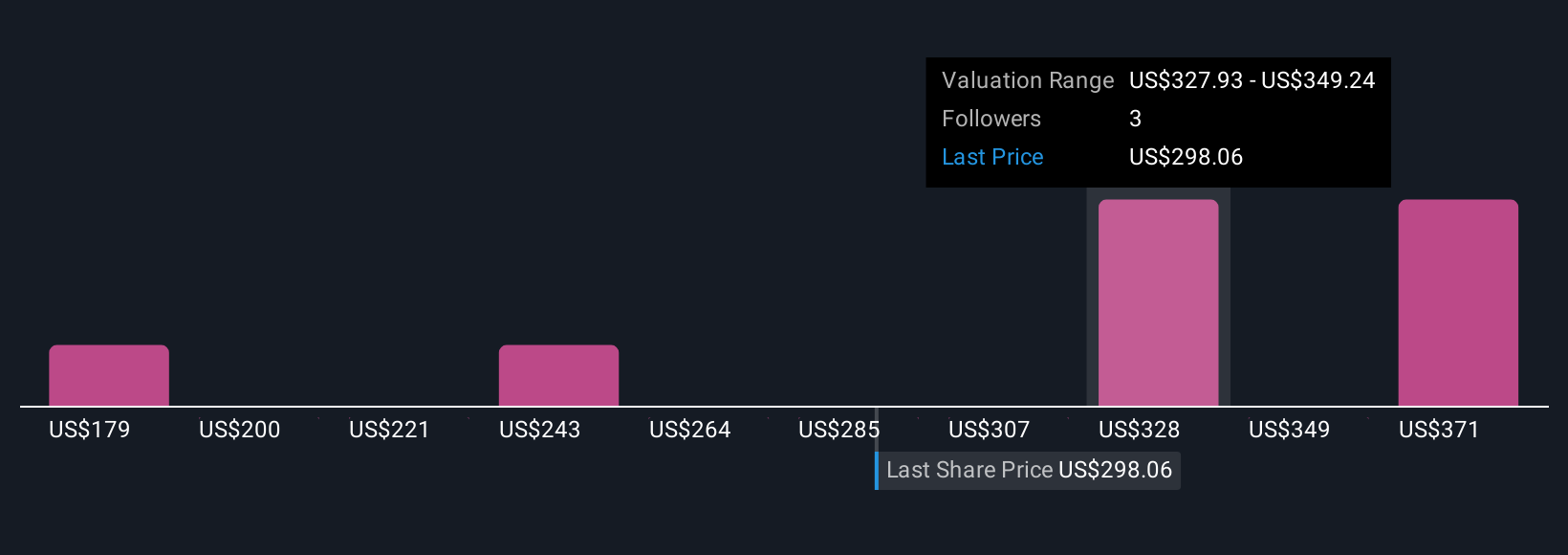

Simply Wall St Community members provided four distinct fair value estimates for Saia, ranging from US$71.48 to US$323.37 per share. While opinions differ on valuation, many keep a close eye on the margin pressures fueled by Saia’s aggressive expansion, reminding you to examine both upside and risks in your own research.

Explore 4 other fair value estimates on Saia - why the stock might be worth less than half the current price!

Build Your Own Saia Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Saia research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Saia research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Saia's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SAIA

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative