Advertisement

- United States

- /

- Airlines

- /

- NasdaqGS:JBLU

How JetBlue’s Fort Lauderdale Expansion Could Influence Its Network Strategy and Growth Plans (JBLU)

Simply Wall St

Reviewed by Simply Wall St

- Earlier this month, JetBlue announced a major expansion of its service at Fort Lauderdale-Hollywood International Airport, adding nine new nonstop routes and increasing capacity on nine existing ones, further reinforcing its position as the airport’s largest carrier this winter with up to 113 daily departures.

- This expansion not only strengthens JetBlue’s footprint in South Florida but also highlights the airline’s ongoing focus on network optimization and reaching underserved destinations across the Americas.

- We'll assess how JetBlue's expanded Fort Lauderdale service may impact its growth strategy and support network optimization goals.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

JetBlue Airways Investment Narrative Recap

JetBlue's strategy centers on capturing growth from leisure travel demand by expanding and optimizing its network, while maintaining a strong cost discipline amid a highly competitive market. The recently announced Fort Lauderdale expansion strengthens JetBlue's market share in a key hub, though the immediate impact on the main near-term catalyst, sustained improvement in load factors and unit revenue, will depend on the pace of demand recovery and competitive responses; meanwhile, the primary risk remains margin pressure from rising labor costs and volatile jet fuel prices.

Among recent announcements, the partnership with Amazon's Project Kuiper to enhance Fly-Fi signals JetBlue's continued investment in improving customer experience and operational efficiency, aligning with catalysts like digital adoption and cost transformation to bolster competitiveness in a price-sensitive market. Both developments highlight how the company is attempting to deliver value while navigating persistent industry headwinds.

However, despite aggressive expansion and cost reduction efforts, the risk of margin compression from rising labor and fuel costs is one investors should watch...

Read the full narrative on JetBlue Airways (it's free!)

JetBlue Airways is projected to reach $10.6 billion in revenue and $728.0 million in earnings by 2028. This outlook implies annual revenue growth of 5.1% and an earnings increase of $1,114 million from current earnings of -$386.0 million.

Uncover how JetBlue Airways' forecasts yield a $4.42 fair value, a 13% downside to its current price.

Exploring Other Perspectives

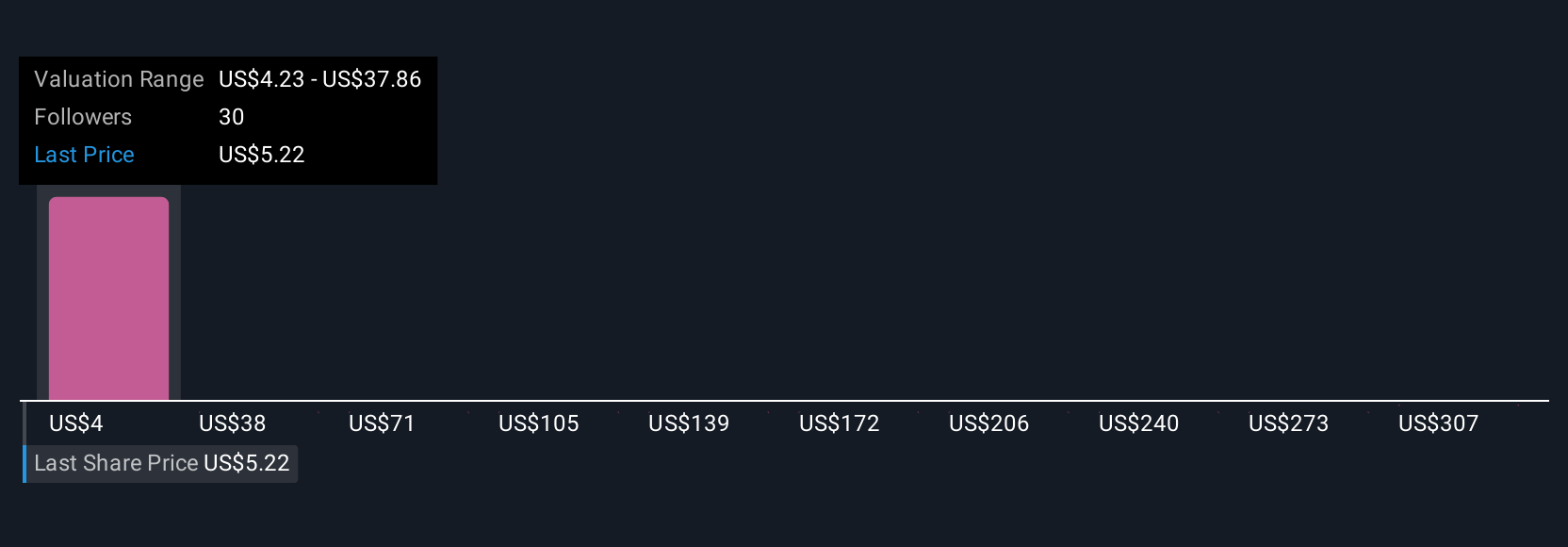

Seven fair value estimates from the Simply Wall St Community range from US$3 to US$340.49 per share, reflecting vastly different views on JetBlue’s valuation. In contrast, ongoing cost inflation and competitive pressures could still challenge profitability, reminding you that perspectives on the airline’s future can differ widely.

Explore 7 other fair value estimates on JetBlue Airways - why the stock might be worth 41% less than the current price!

Build Your Own JetBlue Airways Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your JetBlue Airways research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free JetBlue Airways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate JetBlue Airways' overall financial health at a glance.

No Opportunity In JetBlue Airways?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:JBLU

Undervalued with minimal risk.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor