J.B. Hunt Transport Services (JBHT) shares have captured attention recently as investors evaluate the company’s latest stock performance. With a one-month return of 4 percent and a rise of nearly 20 percent over the past three months, JBHT is seeing renewed interest.

The momentum behind J.B. Hunt’s recent run is starting to stand out, with a 20% three-month share price return that contrasts sharply with its lower long-term total shareholder returns. While gains in recent weeks have caught the market’s interest, the stock’s mixed longer-term total returns show that sentiment is still in a period of transition, as new optimism is balanced against past challenges.

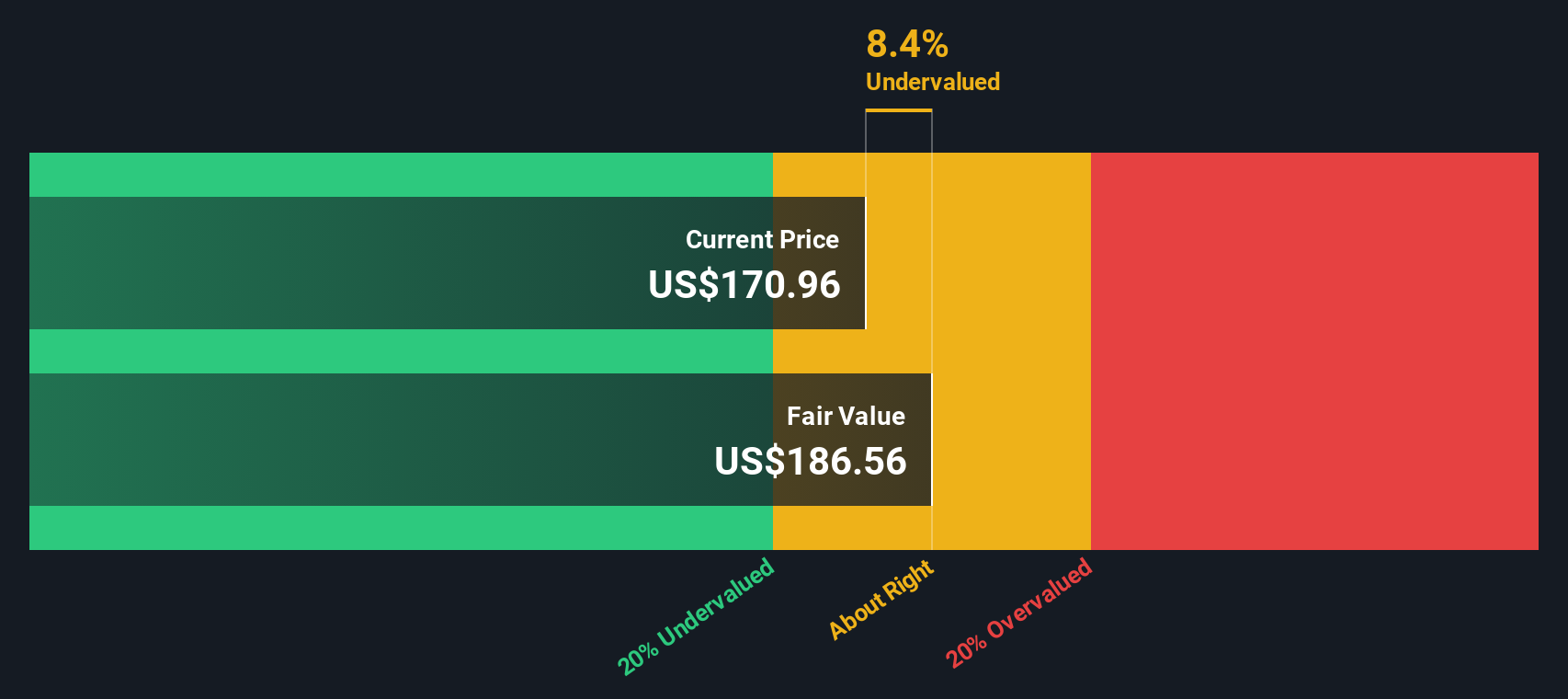

With shares rebounding over the last three months, yet still trailing on longer-term returns, the key question emerges: is J.B. Hunt trading below its true value, or has the market already factored in all anticipated growth?

Advertisement

Most Popular Narrative: 5.1% Overvalued

According to the leading narrative, J.B. Hunt’s fair value sits just below its recent share price, highlighting a premium that the market is willing to pay. With analysts settling on a discount rate narrowly above 8%, the valuation relies on measured optimism about the company’s growth path.

Strategic investments in technology and capacity expansion may provide a platform for long-term revenue growth by better serving large addressable markets. Successful bid season outcomes, including modest rate increases and filling costly empty lanes, could drive better revenue and profitability metrics.

Want to see the real story driving this high valuation? The narrative centers around margin improvement, operational optimization, and growth assumptions that might surprise you. Think you know what’s fueling the premium? The full narrative spells out bold expectations for both profits and revenue in the years ahead. Click through for the details that could shake up your outlook.

However, ongoing inflationary pressures and persistent uncertainty in freight demand could challenge the company’s margin improvement and earnings outlook in the future.

While the current valuation signals J.B. Hunt trades at a premium, our SWS DCF model points in a different direction. The DCF analysis estimates a fair value above today’s share price. This suggests the stock could actually be undervalued if future cash flows meet expectations. Could the market be underestimating J.B. Hunt’s earnings potential?

Build Your Own J.B. Hunt Transport Services Narrative

If you want to examine the data from your own perspective or challenge these views, crafting a personalized narrative is easier than you might think. Give it a try and Do it your way.

A great starting point for your J.B. Hunt Transport Services research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Opportunities?

Don't let a hot stock pass you by when breakthrough investments are just a click away. Expand your horizons and unlock new ways to build wealth.

Tap into tomorrow's technology by scanning these 25 AI penny stocks which is setting the pace for artificial intelligence innovation and smart automation trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks