- United States

- /

- Transportation

- /

- NasdaqGS:GRAB

Despite Lacking Profits Grab Holdings (NASDAQ:GRAB) Seems To Be On Top Of Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Grab Holdings Limited (NASDAQ:GRAB) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Grab Holdings

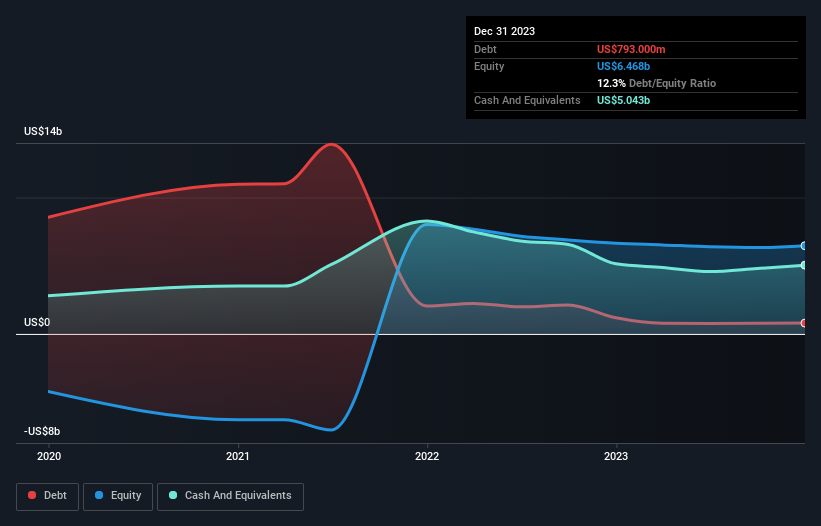

What Is Grab Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that Grab Holdings had debt of US$793.0m at the end of December 2023, a reduction from US$1.18b over a year. But on the other hand it also has US$5.04b in cash, leading to a US$4.25b net cash position.

How Healthy Is Grab Holdings' Balance Sheet?

The latest balance sheet data shows that Grab Holdings had liabilities of US$1.48b due within a year, and liabilities of US$846.0m falling due after that. On the other hand, it had cash of US$5.04b and US$468.0m worth of receivables due within a year. So it can boast US$3.19b more liquid assets than total liabilities.

This surplus suggests that Grab Holdings is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Simply put, the fact that Grab Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Grab Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Grab Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 65%, to US$2.4b. With any luck the company will be able to grow its way to profitability.

So How Risky Is Grab Holdings?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Grab Holdings lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$6.0m of cash and made a loss of US$434m. But the saving grace is the US$4.25b on the balance sheet. That means it could keep spending at its current rate for more than two years. With very solid revenue growth in the last year, Grab Holdings may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Grab Holdings's profit, revenue, and operating cashflow have changed over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:GRAB

Grab Holdings

Engages in the provision of superapps in Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives