Reassessing IDT’s Valuation After Recent Share Price Drift and 3-Month Pullback

Reviewed by Simply Wall St

IDT, the diversified communications and fintech company, has quietly kept its share price moving this month, and that drift can be useful for investors trying to reconcile recent gains with a weaker past 3 months.

See our latest analysis for IDT.

Zooming out, IDT’s $51.47 share price now sits above where it started the year, with a solid year to date share price return and a strong multi year total shareholder return. This suggests longer term momentum remains constructive despite the recent 90 day pullback.

If you like the mix of communications, fintech, and recurring revenue that IDT offers, it may also be worth exploring fast growing stocks with high insider ownership as potential sources of your next idea.

With shares still well below the average analyst target and trading on a modest value score despite resilient earnings, investors now face a key question: is IDT a contrarian buy or already discounting its future growth?

Most Popular Narrative: 35.7% Undervalued

With IDT last closing at $51.47 against a narrative fair value of $80, the gap points to significant upside if the thesis holds.

The company's intention to continue repurchasing shares and increasing dividends, backed by strong cash generation, suggests improved earnings per share (EPS) growth potential.

With ongoing subscription revenue growth and strategic investments in AI and digital channels, net2phone's future performance is expected to boost revenue and improve adjusted EBITDA margins.

Curious how modest revenue shrinkage can still support richer profits and a premium future earnings multiple? Usually, those numbers do not coexist. Want to see how this narrative blends stable margins, disciplined buybacks, and a higher valuation bar into one cohesive fair value story?

Result: Fair Value of $80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent forex headwinds or misjudged capital allocation between buybacks, dividends, and growth investments could easily derail the current undervaluation thesis.

Find out about the key risks to this IDT narrative.

Another Lens On Value

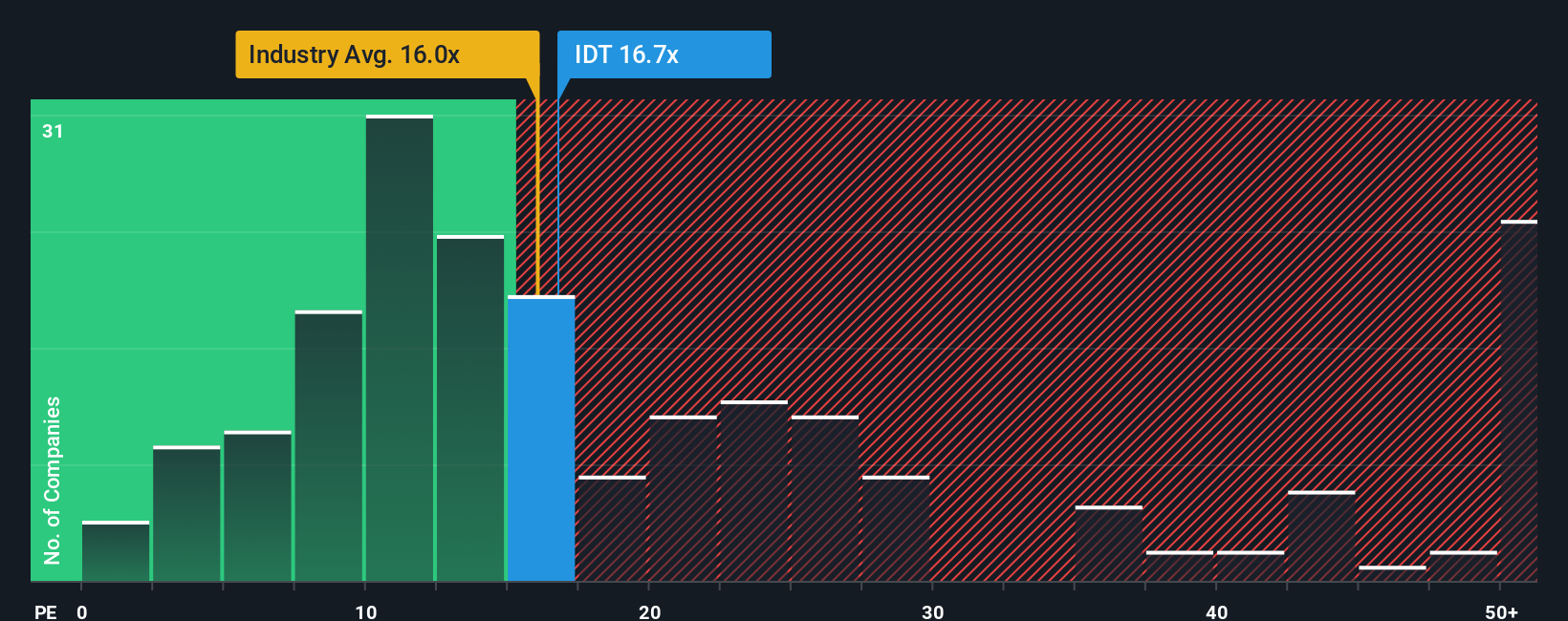

On earnings, the story looks less generous. IDT trades on a price to earnings ratio of 15.9 times, slightly richer than the global telecom average of 15.8 times, well above peers at 7.5 times, and above our fair ratio of 12.9 times. This points to valuation risk rather than clear upside.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own IDT Narrative

If you see the numbers differently or prefer to dig into the details yourself, you can build a personalized view in minutes: Do it your way.

A great starting point for your IDT research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity using the Simply Wall St Screener, where data backed ideas can keep your watchlist one step ahead.

- Capture early stage potential by scanning these 3632 penny stocks with strong financials that pair small market caps with balance sheets and earnings strong enough to support meaningful upside.

- Position yourself at the forefront of automation trends by targeting these 29 healthcare AI stocks that are reshaping diagnostics, treatment pathways, and operational efficiency across medicine.

- Strengthen your income stream with these 12 dividend stocks with yields > 3% that combine payouts above 3 percent with fundamentals aimed at sustaining those distributions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IDT

IDT

Provides communications and payment services in the United States, the United Kingdom, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion