Advertisement

- United States

- /

- Wireless Telecom

- /

- NYSE:AD

Array Digital Infrastructure (AD) Valuation Check After Recent Share Price Move

Array Digital Infrastructure: recent move and performance snapshot

Array Digital Infrastructure (AD) has been drawing attention after a recent positive daily move, with the share price closing at US$50.88. Short term and longer term returns show a mix of gains and pullbacks.

See our latest analysis for Array Digital Infrastructure.

Recent gains sit against a mixed backdrop, with a 7 day share price return of 4.37% and a 30 day share price decline of 11.97%. At the same time, the 1 year total shareholder return of 30.08% and 3 year total shareholder return above 2x suggest longer term momentum has been stronger than the latest pullback.

If Array Digital Infrastructure’s move has you thinking about other ways to get exposure to telecom and network build out, take a look at our screen of 25 power grid technology and infrastructure stocks as a starting list of ideas.

With AD trading at US$50.88 and sitting at a 36% discount to one intrinsic value estimate and 17% below one analyst target, you have to ask: Is there real value here, or is the market already pricing in future growth?

Most Popular Narrative: 11.8% Undervalued

Array Digital Infrastructure’s most followed narrative points to a fair value of about $57.71 per share, which sits above the latest close at $50.88 and frames the current discount in a specific way.

The price target moved from US$54.50 to about US$57.71, representing a modest upward adjustment in the modeled estimate.

The future P/E multiple is reduced from about 117.59x to 65.79x, so the new valuation relies less on very high earnings multiples.

If you want to see what is sitting underneath that fair value band, the key ingredients are future earnings power, margin assumptions and how long the market is expected to pay up for those profits.

Result: Fair Value of $57.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on the AT&T spectrum sale translating into lasting cash flow benefits, and on regulators and competitors not disrupting the underlying tower and spectrum plans.

Find out about the key risks to this Array Digital Infrastructure narrative.

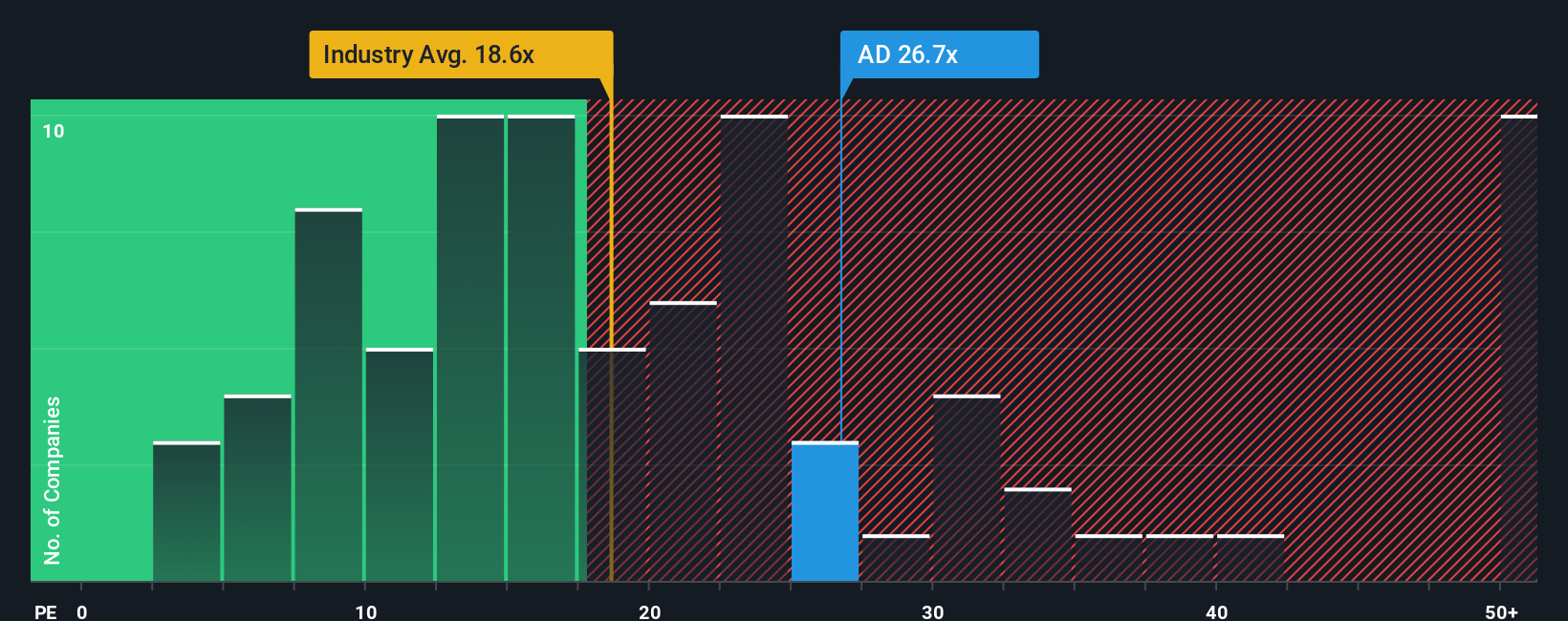

Another View: Earnings Multiple Sends A Different Signal

While the SWS model and analyst fair value work point to AD trading below some intrinsic estimates, the current P/E of 23.5x tells a different story. It sits above the global wireless telecom average of 19.6x and almost double the SWS fair ratio of 12.4x, even though it is below the 34x peer average.

In plain terms, the market is already paying a premium versus the wider industry and the fair ratio, which could limit upside if expectations cool, yet it looks cheaper than closer peers. Which reference point do you think matters more for your own thesis?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Array Digital Infrastructure Narrative

If you see the data differently or simply prefer to test your own assumptions, it is quick to build a custom view of Array Digital Infrastructure and Do it your way in under three minutes.

A great starting point for your Array Digital Infrastructure research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Array Digital Infrastructure has caught your eye, do not stop there. Broaden your watchlist with a few focused stock ideas built from clear fundamentals.

- Target long term compounding potential by reviewing our list of 53 high quality undervalued stocks that pair quality fundamentals with prices that sit below one assessment of fair value.

- Prioritise stability and capital protection by checking companies in our 85 resilient stocks with low risk scores, where business risk scores sit on the lower side of the spectrum.

- Hunt for early stage opportunities with robust finances through our 29 elite penny stocks with strong financials, so you do not miss smaller names that meet strict quality filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AD

Array Digital Infrastructure

Owns and operates shared wireless communications infrastructure in the United States.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7829.0% undervalued

32 followersusers have followed this narrative

6 commentsusers have commented on this narrative

19 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Kratos Defense & Security Solutions ·

Kratos Defense & Security Solutions (KTOS): Scaling "Attritable" Dominance in a New Era of Aerial Conflict.

Fair Value:US$11821.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on BWX Technologies ·

BWX Technologies (BWXT): Powering the Nuclear Renaissance from Naval Depths to Medical Frontiers.

Fair Value:US$205.22.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Merck ·

Merck & Co. (MRK): Scaling the "Post-Keytruda Hill" Through Diversified Blockbusters.

Fair Value:US$144.4818.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1304 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative