- United States

- /

- Wireless Telecom

- /

- NasdaqGS:TMUS

T-Mobile (TMUS): Assessing Valuation After Launching SuperMobile Business Plan for Enterprise Connectivity

Reviewed by Simply Wall St

When a big player like T-Mobile US (TMUS) drops a new business plan, it is worth paying attention, especially when that plan combines features like intelligent network performance, built-in security, and seamless satellite coverage. The newly announced SuperMobile is more than a tweak to existing offerings; it is T-Mobile’s way of signaling to both enterprise customers and investors that the company intends to lead the next wave of connectivity solutions. With Delta Air Lines and Axis Energy Services already exploring the plan, it appears T-Mobile is taking its business ambitions up a notch.

All these moves come at a time when T-Mobile’s share price has shown solid momentum over the past year. The stock has climbed 29% in 12 months and is up nearly 15% so far this year, reflecting growing confidence in its strategy and innovations. Product launches like SuperMobile, along with investments in satellite connectivity and resilient networks, have contributed to this positive perception. These actions set T-Mobile apart from traditional rivals and enhance its growth-oriented reputation.

After this surge, the key question is whether T-Mobile’s future growth is already priced in, or if these advances are setting the stage for another increase in value. Is there a compelling buying opportunity here, or is the market ahead of itself?

Most Popular Narrative: 24.9% Overvalued

According to the narrative by WallStreetWontons, T-Mobile US appears significantly overvalued relative to its calculated fair value. This perspective is built on a detailed examination of growth drivers, profitability, and long-term projections.

"For T-Mobile US (TMUS), forecasts suggest that revenue is expected to grow at an average rate of about 4.3% to 4.4% per annum over the next three years. This growth is driven by factors such as continued customer acquisition, expansion of 5G services, and increasing demand for mobile data. Given the competitive landscape and T-Mobile’s strong market position, this growth trajectory seems plausible."

Want the real story behind T-Mobile’s premium price tag? The narrative reveals one big macro tailwind, and also hints at impressive margin gains and ambitious future multiples that few investors would expect. Curious about the bullish logic or hidden risks influencing this valuation call? Explore the full narrative to find out which bold projections are supporting and potentially inflating TMUS’s price.

Result: Fair Value of $201.69 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, risks such as regulatory challenges or unexpected cost pressures could quickly shift the outlook for T-Mobile’s valuation narrative.

Find out about the key risks to this T-Mobile US narrative.Another View: Our DCF Model Sees Value Differently

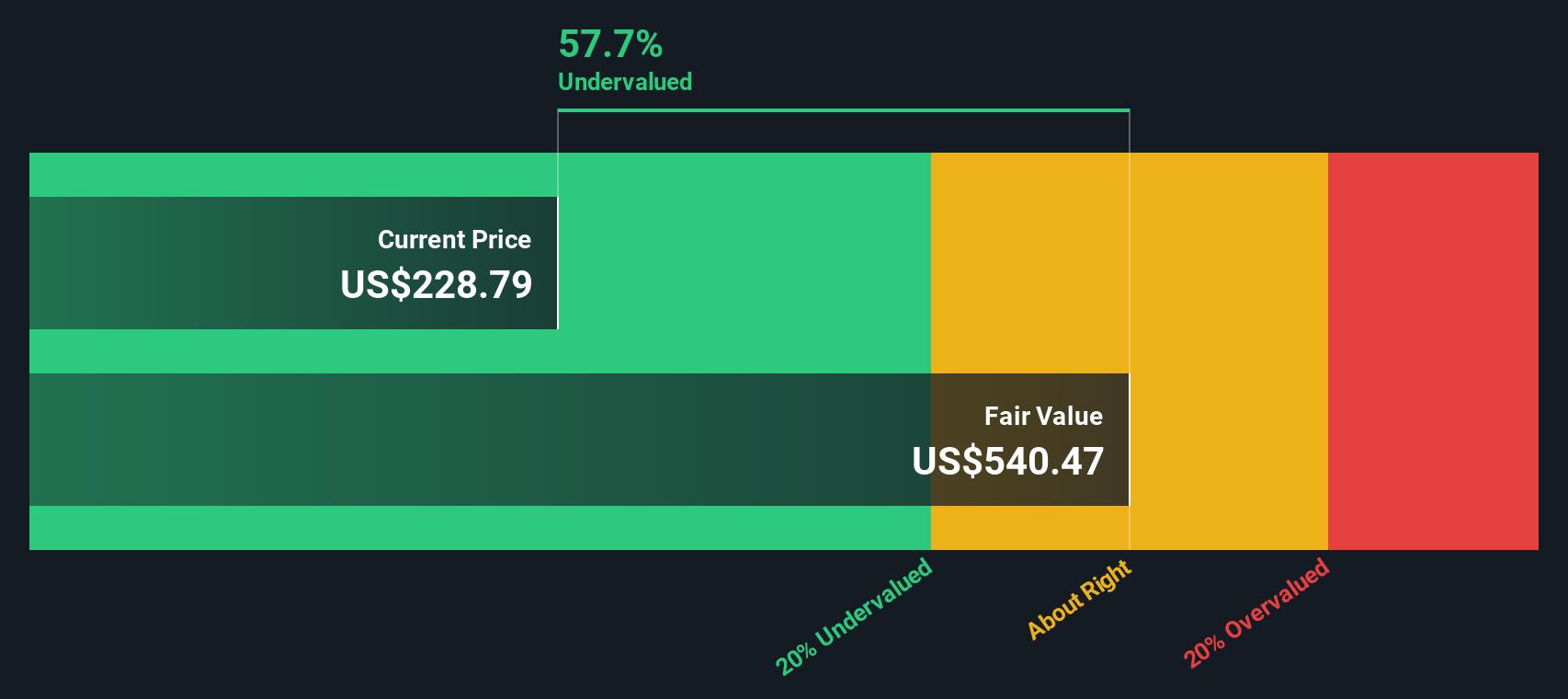

While some analyses suggest T-Mobile is trading above fair value by focusing on growth rates and future earnings, our SWS DCF model offers a different perspective and indicates considerable undervaluation. Which method better reflects reality?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own T-Mobile US Narrative

If you see things differently or want to dig into the numbers yourself, you can quickly build your own story in just a few minutes with Do it your way.

A great starting point for your T-Mobile US research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Stock markets never stand still, and the next big opportunity could be just around the corner. Don’t let the best prospects slip past you. Put your research to work with these timely ideas from Simply Wall Street’s powerful screener tools:

- Unearth value with companies trading well below their cash flow potential by using our undervalued stocks based on cash flows. This tool can help you spot stocks that the market may be overlooking right now.

- Maximize your income potential by focusing on dividend stocks with yields > 3%. Identify companies with strong yields that can boost your portfolio’s returns even in uncertain markets.

- Ride the wave of technological disruption by targeting AI penny stocks. Use this approach to get ahead of trends shaping tomorrow’s business landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if T-Mobile US might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:TMUS

T-Mobile US

Provides wireless communications services in the United States, Puerto Rico, and the United States Virgin Islands.

Good value with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion