Advertisement

Vishay Intertechnology (VSH): Assessing Valuation After Recent Share Price Decline

Vishay Intertechnology (VSH) shares have been on investors’ minds lately, with the stock slipping over the past month. Some are curious what this means for longer-term portfolio positioning and whether the recent price action creates opportunity.

See our latest analysis for Vishay Intertechnology.

It’s been a choppy year for Vishay Intertechnology, with the 1-year total shareholder return down 16.5% and shorter-term price swings hinting at fading momentum. Investors are reassessing the company’s prospects and shifting risk profile. Despite occasional positive signals, the recent share price decline suggests sentiment is cooling over the short run.

If you’re interested in finding companies with momentum and potential, now’s the time to discover fast growing stocks with high insider ownership

With shares down but some value metrics still looking attractive, the big question now is whether the recent pullback reflects an undervalued opportunity, or if the market has already accounted for all future growth prospects.

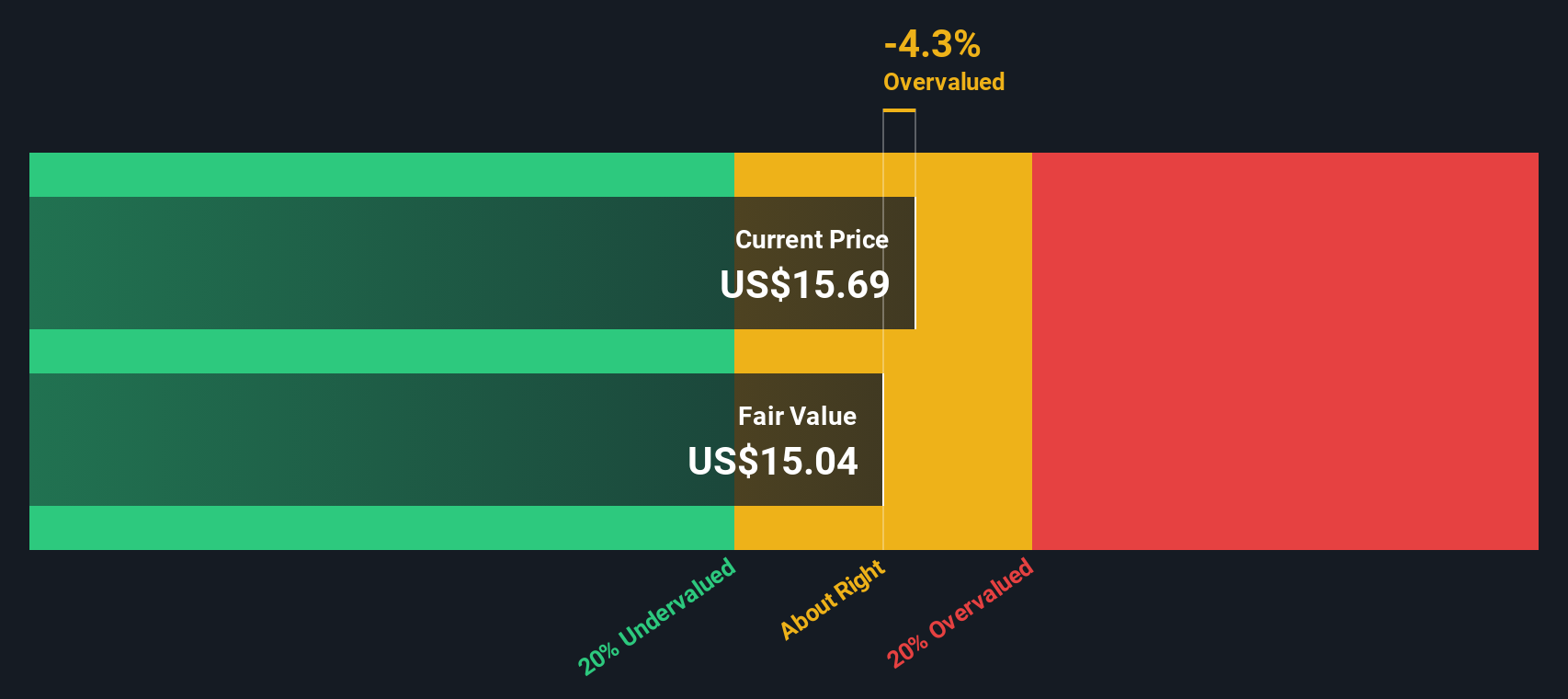

Most Popular Narrative: 4.1% Overvalued

With Vishay Intertechnology’s current price closing higher than the narrative’s fair value estimate, questions emerge about whether the market is too optimistic or simply pricing in a turnaround. Readers should look for what is supposed to drive growth from here.

With major multi-year investments in capacity expansion nearing completion, including readiness across nearly all product lines and the ramp of high-growth, higher-profit products, Vishay is well positioned to capture share as demand accelerates in areas like AI, smart grid infrastructure, data centers, and automotive electrification. This is expected to support higher future revenues and improved operating leverage.

Want to unlock the full story driving this price tag? The narrative’s fair value is built on ambitious revenue growth, fatter margins, and a bold profit turnaround in just a few years. Which specific financial forecasts and future assumptions make this possible? Only the full narrative reveals how these pieces fit together and whether they add up in reality.

Result: Fair Value of $14.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy spending and lingering profitability challenges could strain Vishay’s turnaround story if demand does not rebound as anticipated.

Find out about the key risks to this Vishay Intertechnology narrative.

Another View: What Does the SWS DCF Model Say?

Looking at Vishay Intertechnology from a discounted cash flow (DCF) perspective, our model points to a fair value of $17.16 per share, around 15% above the current price. This suggests the market may be overlooking long-term cash flow potential. Which outlook should investors trust: near-term worries or longer-range forecasts?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Vishay Intertechnology Narrative

If you have a different perspective or want to dig into the numbers yourself, you can craft your own take on Vishay Intertechnology’s outlook in just a few minutes. Do it your way.

A great starting point for your Vishay Intertechnology research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors continually expand their horizons. Don’t let lucrative opportunities pass you by. Propel your portfolio forward by checking out these standout stock picks right now:

- Unlock serious growth potential when you examine these 25 AI penny stocks powering tomorrow’s AI breakthroughs and automation revolutions.

- Boost your passive income by reviewing these 17 dividend stocks with yields > 3% that consistently deliver robust yields well above the market average.

- Get ahead of the next fintech surge and evaluate these 82 cryptocurrency and blockchain stocks at the forefront of digital assets and blockchain innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VSH

Vishay Intertechnology

Manufactures and sells discrete semiconductors and passive electronic components in the United States, Germany, rest of Europe, Israel, and Asia.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7461.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on CSL ·

Strong buy. World-leading healthcare company with steady growth

Fair Value:AU$143.1519.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative