Advertisement

Assessing Keysight Technologies (KEYS) Valuation After Material CES 2026 Satellite Connectivity Breakthrough

Keysight Technologies (KEYS) is back in focus after its CES 2026 showcase of an end to end live NR NTN connection in band n252 using Samsung’s next generation modem chipset, a step with clear industry implications.

See our latest analysis for Keysight Technologies.

The recent CES announcements land against a backdrop where Keysight’s share price has reached US$208.73, with a 90 day share price return of 26.63% and a 1 year total shareholder return of 29.56%. This suggests momentum has been building rather than fading.

If satellite connectivity and AI testing tools have your attention, this could be a useful moment to widen your watchlist. You may want to consider high growth tech and AI stocks as potential comparison ideas.

With the shares at US$208.73, trading only around 5% below the average analyst price target and with an internal model pointing to a premium, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 5% Undervalued

With Keysight closing at US$208.73 and the most followed narrative pointing to fair value of about US$219.77, the gap between price and intrinsic estimate is not large but it is meaningful enough to merit a closer look at what is driving that number.

Expansion of software and recurring service offerings, now comprising 36% and 28% of total revenue respectively, increases gross and net margins by enhancing revenue stability, improving product mix, and reducing cyclicality from traditional hardware segments.

Curious what kind of revenue growth, margin uplift, and future P/E this narrative assumes to justify that higher fair value line? The underlying model leans heavily on earnings expansion and a richer profit mix to support a premium multiple. If you want to see exactly how those moving parts come together, the full narrative lays out the numbers in detail.

Result: Fair Value of $219.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case still depends on assumptions that tariffs do not squeeze margins more than planned and that AI driven demand does not cool faster than expected.

Find out about the key risks to this Keysight Technologies narrative.

Another View: What The P/E Is Telling You

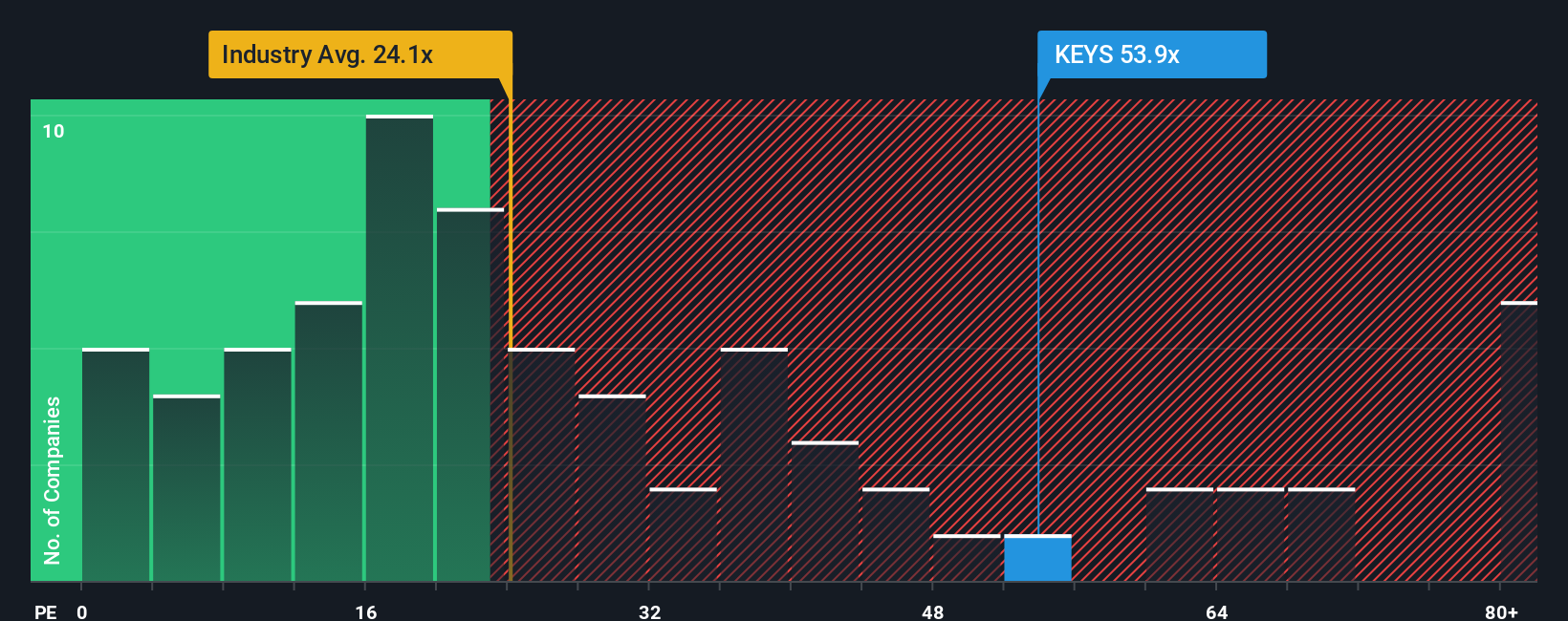

Our narrative-based fair value of US$219.77 points to some upside, but the P/E story is more cautious. At US$208.73, Keysight trades on a 41.3x P/E, above both the US Electronic industry average of 26x and an estimated fair ratio of 28x, even if it sits below peer averages at 44.2x. That gap suggests some valuation risk if expectations cool. The key question is whether the earnings story can keep justifying this premium.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Keysight Technologies Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own assumptions in detail, you can build a custom Keysight view yourself in just a few minutes: Do it your way.

A great starting point for your Keysight Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Keysight has sharpened your thinking, do not stop here, widen your opportunity set now so you are not relying on a single story.

- Spot potential mispricings quickly by scanning these 880 undervalued stocks based on cash flows that may offer more for each dollar of expected cash flow.

- Target growth themes by lining up these 26 AI penny stocks that are tied to real business models, not just hype.

- Boost your income focus by screening these 12 dividend stocks with yields > 3% that could add consistent cash returns to your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keysight Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KEYS

Keysight Technologies

Provides electronic design and test solutions worldwide.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

11 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative