Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:STX

Seagate Technology Holdings (STX) Stock After A 4% Pullback And Huge Year-To-Date Rally

Reviewed by Bailey Pemberton

- Investors may be wondering whether Seagate Technology Holdings still offers value after a strong run, or if the stock is already priced for perfection.

- At a last close of US$1,025.36, the stock has fallen about 4.2% over the past week, after very large returns over the past year and multi year period, including a 21.2% gain over the last month and a 256.6% return year to date.

- Recent coverage has focused on Seagate Technology Holdings as a key player in data storage and related technologies, with investors reacting to how the company is positioned in areas like AI infrastructure and cloud demand. This context helps explain why the stock has seen both sharp gains and short term pullbacks as expectations reset.

- Simply Wall St currently assigns Seagate Technology Holdings a value score of 1 out of 6. This will be unpacked using different valuation methods before considering an additional approach that can help you make sense of the numbers.

Seagate Technology Holdings scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Seagate Technology Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what Seagate Technology Holdings could be worth today by projecting future cash flows and discounting them back to a present value. It focuses on cash the company may generate for shareholders rather than just reported earnings.

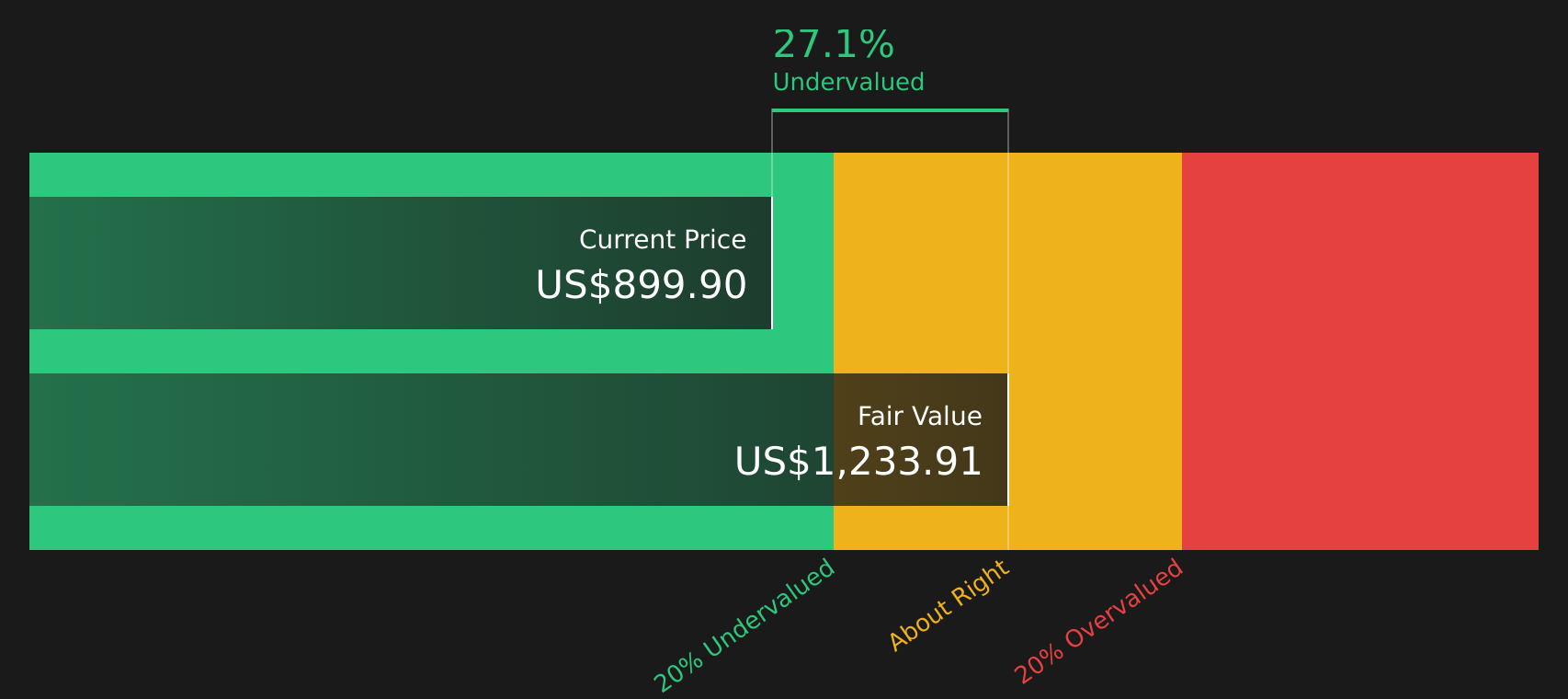

For Seagate Technology Holdings, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model. The latest twelve month free cash flow stands at about $2.47b. Based on analyst inputs for the next few years, and then extending those trends further out, Simply Wall St projects free cash flow reaching $11.72b in 2030. The full set of projections runs through 2035 in the $2.88b to $21.50b range before discounting.

Bringing all of those projected cash flows back to today results in an estimated intrinsic value of about $1,240.49 per share. Compared with the recent share price of $1,025.36, the model suggests Seagate Technology Holdings stock is around 17.3% undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Seagate Technology Holdings is undervalued by 17.3%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Approach 2: Seagate Technology Holdings Price vs Earnings

P/E is often the go to multiple for profitable companies like Seagate Technology Holdings because it links what you pay for each share directly to the earnings that support it. In general, higher expected earnings growth and lower perceived risk can justify a higher P/E, while slower growth or higher risk usually call for a lower, more conservative P/E.

Seagate Technology Holdings currently trades on a P/E of 97.56x. This compares with a Tech industry average P/E of 23.57x and a peer group average of 46.95x, so the stock is priced at a much higher multiple than these broad benchmarks. To add more context, Simply Wall St also calculates a “Fair Ratio” of 78.80x, which is the P/E that might be expected given factors such as the company’s earnings growth profile, margins, industry, market cap and risk characteristics.

This Fair Ratio is more tailored than a simple peer or industry comparison because it attempts to adjust for the specific qualities of Seagate Technology Holdings rather than treating all companies as alike. Comparing the current P/E of 97.56x with the Fair Ratio of 78.80x suggests the stock is trading above that indicated range.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Seagate Technology Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a simple story behind the numbers by letting you connect your view of Seagate Technology Holdings to explicit assumptions for future revenue, earnings and margins. These then flow into a Fair Value you can compare with the current share price to decide whether the stock looks attractive or expensive. Narratives update automatically when new news or earnings arrive, and they capture a wide range of perspectives. For example, one investor might build a cautious Seagate Technology Holdings Narrative around a Fair Value closer to US$566.86, while another uses a more optimistic Narrative closer to US$1,096.35. All of this is available within the Community page used by millions of investors.

For Seagate Technology Holdings, we will make it really easy for you with previews of two leading Seagate Technology Holdings Narratives:

Each Narrative links explicit assumptions about future revenue, margins and valuation to a Fair Value, so you can quickly see which story, if any, is closer to your own view of the stock.

🐂 Seagate Technology Holdings Bull Case

Fair Value: US$1,096.35

Implied discount to Fair Value vs last close: about 6.5% undervalued

Assumed revenue growth rate: 37.51%

- Assumes Seagate Technology Holdings benefits from strong AI related data growth, regulatory data retention trends and faster adoption of high capacity HAMR based drives.

- Bullish analysts model revenue reaching about US$28.6b and earnings of US$16.0b by 2029, with profit margins rising to 55.8% and the stock trading on a lower P/E of 22.9x at that point.

- Key risks include a faster shift to flash storage, pricing pressure from large cloud customers, potential regulatory and sustainability costs, and the possibility that HAMR rollout or customer spending plans fall short of expectations.

🐻 Seagate Technology Holdings Bear Case

Fair Value: US$847.68

Implied premium to Fair Value vs last close: about 21.0% overvalued

Assumed revenue growth rate: 30.37%

- Builds on strong demand for mass capacity storage and HAMR technology, with Seagate Technology Holdings benefiting from cloud and AI data center spending, pricing discipline and build to order contracts.

- Analysts in this camp assume revenue of about US$24.4b and earnings of US$10.9b by 2029, with margins at 44.7% and a future P/E of 25.9x, which leads to a consensus Fair Value close to the current share price.

- Flags risks around trade policy, supply constraints, leverage, competition from SSDs and QLC NAND, and potential tax changes that could lift the effective tax rate from fiscal 2026.

Together, these Seagate Technology Holdings Narratives frame a useful range for what the stock might be worth under different assumptions about AI storage demand, margins and balance sheet risk, so you can decide which story, if either, feels closer to your own expectations for the company.

To see how other investors are building out these stories in detail, including their full earnings paths and risk lists, See what the community is saying about Seagate Technology Holdings.

Do you think there's more to the story for Seagate Technology Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:STX

Seagate Technology Holdings

Engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5297.0% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3076.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative