Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:STX

Seagate Technology Holdings (STX) Following Its Pullback Is The AI Storage Story Fully Valued

Seagate Technology Holdings (STX) is back in focus after its stock fell 12.2% during a wider tech pullback, a sharp move that stands out against its strong year-to-date performance and its AI-fueled storage story.

See our latest analysis for Seagate Technology Holdings.

In the short term, Seagate Technology Holdings has seen some heat come out of the trade, with the share price down 5.16% over one day and 7.86% over seven days. This sits against a backdrop of a 113.15% 90 day share price return and a 1 year total shareholder return that is more than 5x.

If Seagate’s AI storage surge has caught your attention, it can be useful to see what else is moving in related areas by checking out 53 AI infrastructure stocks.

With Seagate Technology Holdings now trading after a huge 1 year total shareholder return and only a modest 3.6% discount to the average analyst price target, the key question is simple: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 8% Overvalued

On the latest numbers, Seagate Technology Holdings closed at $915.19 against a most followed narrative fair value of $847.68, setting up a clear valuation gap for investors to test.

The analysts have a consensus price target of $847.68 for Seagate Technology Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $1150.0, and the most bearish reporting a price target of just $545.0.

Want to see what powers this Seagate narrative beyond the headline fair value? The earnings ramp, margin profile and future multiple assumptions are where the story really lives.

Result: Fair Value of $847.68 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Seagate Technology Holdings still faces clear pressure points, including potential impacts from trade policy changes and intense competition from SSD and QLC NAND that could challenge the current AI storage narrative.

Find out about the key risks to this Seagate Technology Holdings narrative.

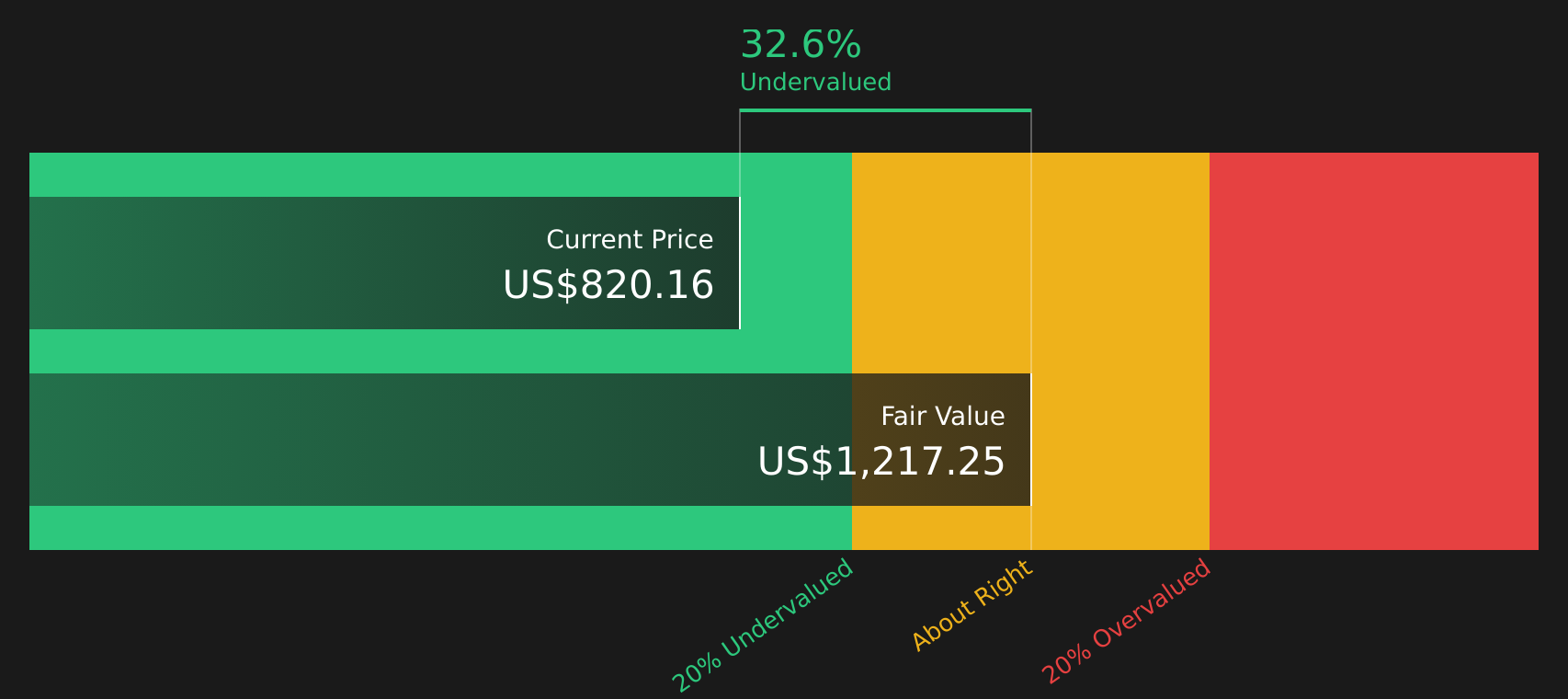

Another View: Seagate Technology Holdings Through a Cash Flow Lens

While the most followed Seagate Technology Holdings narrative points to an 8% premium to its $847.68 fair value estimate, a different approach tells another story. Our DCF model, which discounts future cash flows back to today, suggests a fair value of $1,212.54, implying the stock trades at a 24.5% discount.

This creates a clear tension for investors, with one lens flagging Seagate as expensive on earnings multiples and another implying underpricing based on future cash generation. Which story do you think makes more sense for your own thesis on STX?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Seagate Technology Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing Seagate Technology Holdings pulled in different directions on valuation and expectations, it makes sense to move fast and test the numbers for yourself. To balance the concerns and the upside, take a closer look at the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Seagate Technology Holdings?

If Seagate has sharpened your focus, do not stop here; broaden your watchlist with fresh stock ideas built from consistent rules and clear financial data.

- Spot potential value opportunities early by checking companies highlighted in the 41 high quality undervalued stocks before others catch on.

- Strengthen your income game by reviewing reliable payers through the 8 dividend fortresses to see which yields might fit your goals.

- Prioritize resilience and peace of mind by scanning financially robust companies using the solid balance sheet and fundamentals stocks screener (47 results) built to handle tougher conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:STX

Seagate Technology Holdings

Engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

IN

inimosini on Lucky Cement ·

Discounted Cash Flow Valuation of Lucky Cement Limited (LUCK)

Fair Value:PK₨511.86.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative