Super Micro Computer (SMCI) shares dipped slightly this week, moving down about 1% over the past day and nearly 25% in the past month. Investors are weighing recent market activity as they evaluate the stock's current valuation.

While short-term momentum has faded for Super Micro Computer, with a sharp pullback over the past month, the bigger picture is still striking: the company’s total shareholder return over the past year stands at an impressive 62.15%, and its five-year total return exceeds 1,200%. This long-term performance highlights how quickly market sentiment can shift for high-growth tech names, sometimes on changing risk perceptions and sometimes on evolving views of future potential, reminding investors to keep the full context in mind.

If you're tracking tech sector shifts or looking for fresh opportunities, it's worth checking out See the full list for free..

With shares now trading well below recent highs, the key question is whether Super Micro Computer’s current price reflects a temporary dip or if future growth is already fully accounted for, leaving little room for upside.

Advertisement

Most Popular Narrative: 21.9% Undervalued

Compared to the last close price, the most widely followed narrative suggests Super Micro Computer could have notable upside, with its fair value well above the current market level. The narrative view is built around major growth catalysts and shifting industry trends, setting the stage for a closer look at the drivers analysts are focusing on.

The accelerating global adoption of AI and analytics continues to drive demand for high-performance, scalable server and data center solutions. This positions Super Micro for strong multi-year revenue growth as enterprises and nations build out AI infrastructure, directly supporting projected revenue outperformance. The company's launch and rapid expansion of its Data Center Building Block Solution (DCBBS) enables customers to deploy turnkey, energy-efficient, and customized AI data centers faster than traditional solutions. This supports a higher-margin product mix and improves gross and operating margins over time.

Want to know what’s fueling this potential surge? This narrative hinges on future growth rates and a profit outlook some view as bold. See exactly which metrics and assumptions power this surprising fair value.

However, persistent supply chain scrutiny and mounting margin pressures remain key risks. These factors could potentially challenge the optimistic growth outlook for Super Micro Computer.

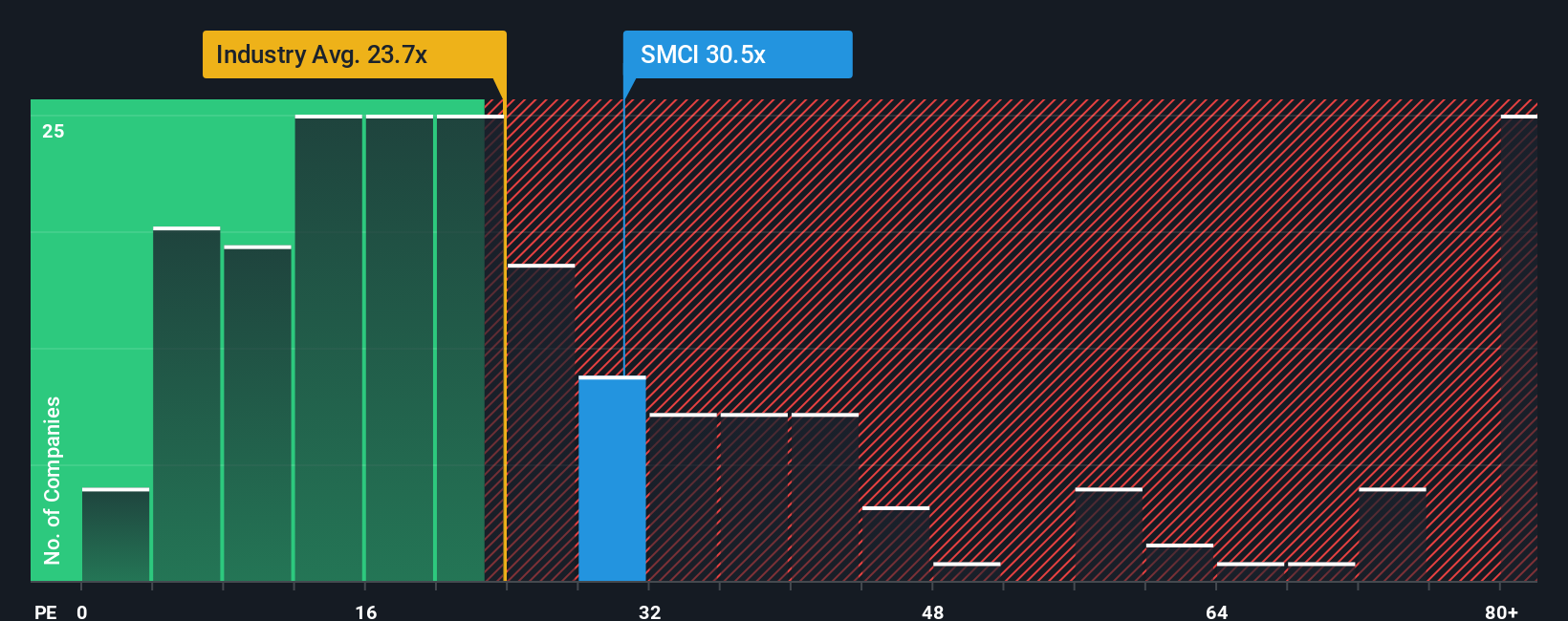

Looking at valuation through the lens of earnings multiples, Super Micro Computer trades at a ratio of 29.9 times earnings, which is notably higher than both the peer average (22.7x) and the global tech industry average (22.6x). While this premium can reflect positive growth expectations, it also highlights greater valuation risk if those high expectations are not met. The fair ratio, where the share price could gravitate over time, is estimated at 92.5x, suggesting both challenge and potential depending on how market sentiment evolves.

If you see things differently or want a deeper, personal dive into the data, you can shape your own take in just minutes. Do it your way.

A great starting point for your Super Micro Computer research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don't let your next big opportunity slip away when so many unique stock ideas are at your fingertips on Simply Wall Street's free Screener. Researching beyond the obvious could be your smartest move this year.

Unlock opportunities in emerging artificial intelligence trends by browsing these 25 AI penny stocks and see which innovators are poised to shape tomorrow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.