Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:NSSC

Napco Security Technologies (NSSC): Valuation in Focus After Launching Next-Gen Security Solutions and Expanding StarLink Platform

Napco Security Technologies (NSSC) has caught attention after revealing a lineup of new integrated security solutions at ISC East 2025 in New York City. The company is highlighting innovations designed to enhance its MVP Cloud platform and modernize its StarLink line.

See our latest analysis for Napco Security Technologies.

Following this showcase of new solutions, Napco Security Technologies has continued to ride strong momentum, with a 30.3% share price return over the last 90 days and a total shareholder return of 8.96% for the past year. Strong demand for integrated security products and healthy expansion in recurring revenues have helped keep attention on the stock, and its long-term total return stands at an impressive 180.8% over five years. This reflects consistent growth and evolving market leadership.

If you've got an eye on high-growth opportunities with strong management ownership, now's a smart time to explore fast growing stocks with high insider ownership

With Napco’s shares recently up over 30% in three months and robust growth fueling optimism, the key question is whether the current price still offers value for investors, or if future gains are already reflected in the price.

Most Popular Narrative: 16.9% Undervalued

Compared to the most recent closing price of $39.59, the narrative fair value of $47.67 signals a significant upside that stands out in today’s market. The calculation hinges on bold assumptions about future margins, profit growth, and a premium earnings multiple that investors may find compelling.

Ongoing digital innovation and pricing actions, backed by a strong balance sheet, drive product innovation, gross margin recovery, and long-term growth. Operational discipline, strong cash generation, and a debt-free balance sheet enable Napco to reinvest in innovation, pursue strategic acquisitions, and flexibly return capital to shareholders. This supports long-term earnings growth and valuation recovery.

Want to know what projections power such a high fair value? The expected margin expansion, ambitious growth targets, and a future earnings multiple not seen in many competitors all factor in. Unpack the precise financial bets this narrative is making. See which assumptions could send the valuation even higher or unravel the upside story.

Result: Fair Value of $47.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued softness in hardware demand or increased reliance on StarLink recurring revenue could challenge Napco’s momentum if broader markets weaken.

Find out about the key risks to this Napco Security Technologies narrative.

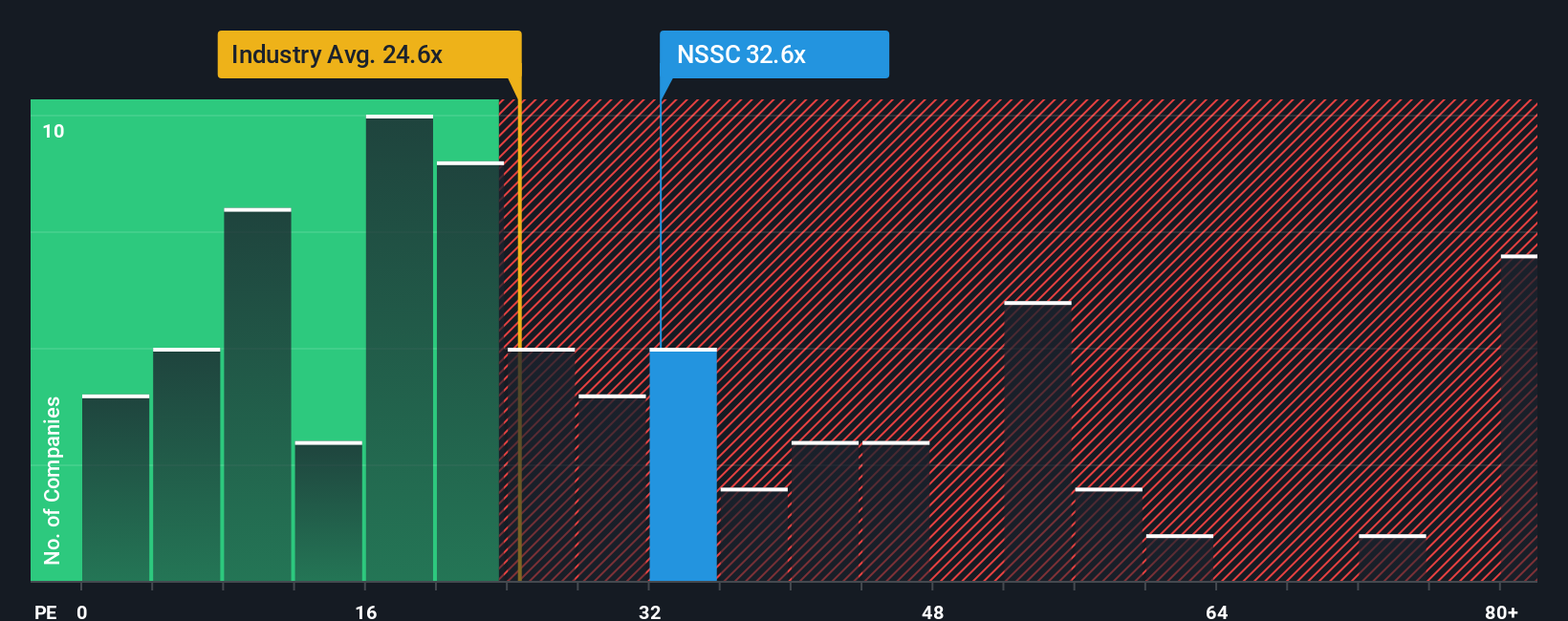

Another View: What Do Earnings Multiples Suggest?

Take a look at the market's most-used benchmark: the price-to-earnings ratio. Napco’s PE stands at 31.8x, noticeably higher than both the US Electronic industry average of 22.8x and the fair ratio of 24.8x. However, it remains below peers trading at 45.4x. This means investors are paying a premium for Napco, banking on faster growth or resilience than much of the sector. Does this premium signal confidence or indicate valuation risk as competition intensifies?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Napco Security Technologies Narrative

If these views aren't quite your own or you’d rather dive into the numbers yourself, building your customized narrative takes less than three minutes with our tools. Do it your way

A great starting point for your Napco Security Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more ways to boost your portfolio?

Don't let standout opportunities pass you by when there are smart investment ideas right within reach. Delve into stocks making waves in technology, healthcare, and crypto that could reshape your financial outlook.

- Spot up-and-coming healthcare innovators by checking out these 30 healthcare AI stocks. This screener highlights the next advancements in medical technology and AI-driven solutions.

- Capitalize on shifts in digital finance and blockchain by moving toward these 81 cryptocurrency and blockchain stocks. Here you will find companies redefining the financial world with breakthrough payment systems.

- Uncover attractive value prospects by targeting these 898 undervalued stocks based on cash flows to pinpoint stocks with strong potential trading below their intrinsic worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Napco Security Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NSSC

Napco Security Technologies

Engages in the development, manufacturing, and sale of electronic security systems for commercial, residential, institutional, industrial, and governmental applications in the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

10 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative