- United States

- /

- Communications

- /

- NasdaqCM:LTRX

Shareholders Will Most Likely Find Lantronix, Inc.'s (NASDAQ:LTRX) CEO Compensation Acceptable

Under the guidance of CEO Paul Pickle, Lantronix, Inc. (NASDAQ:LTRX) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 09 November 2021. We present our case of why we think CEO compensation looks fair.

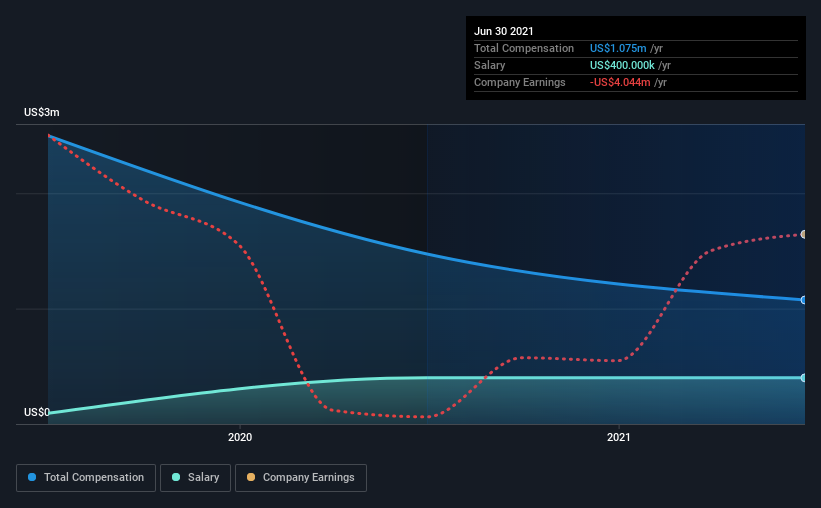

See our latest analysis for Lantronix

How Does Total Compensation For Paul Pickle Compare With Other Companies In The Industry?

According to our data, Lantronix, Inc. has a market capitalization of US$287m, and paid its CEO total annual compensation worth US$1.1m over the year to June 2021. Notably, that's a decrease of 27% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$400k.

For comparison, other companies in the same industry with market capitalizations ranging between US$100m and US$400m had a median total CEO compensation of US$1.1m. This suggests that Lantronix remunerates its CEO largely in line with the industry average. Furthermore, Paul Pickle directly owns US$4.0m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | US$400k | US$400k | 37% |

| Other | US$675k | US$1.1m | 63% |

| Total Compensation | US$1.1m | US$1.5m | 100% |

Talking in terms of the industry, salary represented approximately 21% of total compensation out of all the companies we analyzed, while other remuneration made up 79% of the pie. It's interesting to note that Lantronix pays out a greater portion of remuneration through salary, compared to the industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Lantronix, Inc.'s Growth

Over the last three years, Lantronix, Inc. has shrunk its earnings per share by 73% per year. Its revenue is up 19% over the last year.

Investors would be a bit wary of companies that have lower EPS But on the other hand, revenue growth is strong, suggesting a brighter future. It's hard to reach a conclusion about business performance right now. This may be one to watch. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Lantronix, Inc. Been A Good Investment?

Most shareholders would probably be pleased with Lantronix, Inc. for providing a total return of 151% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Some shareholders will be pleased by the relatively good results, however, the results could still be improved. Still, we think that until shareholders see an improvement in EPS growth, they may find it hard to justify a pay rise for the CEO.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 2 warning signs for Lantronix that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking to trade Lantronix, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:LTRX

Lantronix

Develops, markets, and sells industrial and enterprise internet of things (IoT) products and services in the Americas, Europe, the Middle East, Africa, and the Asia Pacific Japan.

Excellent balance sheet and fair value.

Market Insights

Community Narratives