Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqCM:LPTH

We Think The Compensation For LightPath Technologies, Inc.'s (NASDAQ:LPTH) CEO Looks About Right

The share price of LightPath Technologies, Inc. (NASDAQ:LPTH) has increased significantly over the past few years. However, the earnings growth has not kept up with the share price momentum, suggesting that some other factors may be driving the price direction. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 17 November 2022. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From what we gathered, we think shareholders should be wary of raising CEO compensation until the company shows some marked improvement.

Check out the opportunities and risks within the US Electronic industry.

Comparing LightPath Technologies, Inc.'s CEO Compensation With The Industry

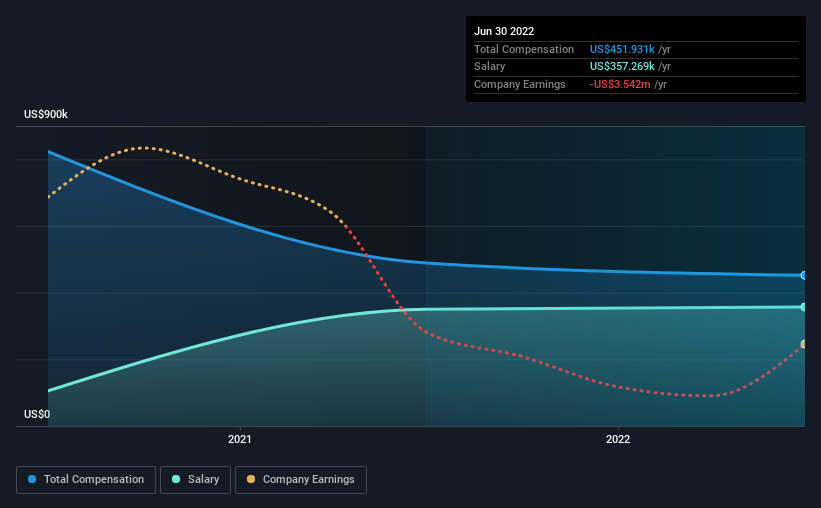

At the time of writing, our data shows that LightPath Technologies, Inc. has a market capitalization of US$28m, and reported total annual CEO compensation of US$452k for the year to June 2022. That's a slight decrease of 7.6% on the prior year. Notably, the salary which is US$357.3k, represents most of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under US$200m, the reported median total CEO compensation was US$408k. So it looks like LightPath Technologies compensates Sam Rubin in line with the median for the industry.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | US$357k | US$350k | 79% |

| Other | US$95k | US$139k | 21% |

| Total Compensation | US$452k | US$489k | 100% |

On an industry level, around 30% of total compensation represents salary and 70% is other remuneration. According to our research, LightPath Technologies has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at LightPath Technologies, Inc.'s Growth Numbers

Over the last three years, LightPath Technologies, Inc. has shrunk its earnings per share by 29% per year. In the last year, its revenue is down 7.6%.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has LightPath Technologies, Inc. Been A Good Investment?

Boasting a total shareholder return of 66% over three years, LightPath Technologies, Inc. has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean returns may be hard to keep up. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for LightPath Technologies that investors should be aware of in a dynamic business environment.

Important note: LightPath Technologies is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LPTH

LightPath Technologies

Designs, develops, manufactures, and distributes optical systems and assemblies in the United States.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25380.9% overvalued

68 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

69 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.4% overvalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

YI

yiannisz on Etsy ·

Etsy Stock: Defending Differentiation in a World of Infinite Marketplaces

Fair Value:US$64.459.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Align Technology ·

Align Technology Stock: Premium Orthodontics in a Cost-Sensitive World

Fair Value:US$154.623.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BO

BonSquid88 on Micron Technology ·

Micron Technology will experience a robust 16.5% revenue growth

Fair Value:US$40022.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

69 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25380.9% overvalued

68 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0225.6% undervalued

1019 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative

Trending Discussion

ST

StevenM on Excellon Resources ·

Interesting analysis, but the price trajectory assumed for the baseline metals is problematic. These assumptions form the foundation for the entire case, and when compared against historical pricing, don’t appear to be grounded in any reasonable precedent. Even accounting for past commodity super-cycles, inflationary periods, or supply constraints, the forecasted pricing for gold, silver, zinc, and lead are well outside what history would suggest is plausible over comparable timeframes. That creates a fragile premise as the conclusions are driven by aggressive inputs rather than underlying market behavior that is realistic. The analysis would be materially stronger if the price assumptions were anchored to historical ranges and prior cycle peaks, with explicit rationale where the model intentionally departs from those patterns. As it stands, the trajectory feels more aspirational than analytical.

1

|1