F5 (FFIV) just made waves by raising its full-year revenue guidance on the back of an impressive third quarter, which saw the company post 12% year-over-year growth and a 26% jump in product revenue. Management did not shy away from spotlighting rising demand in both content delivery and cloud segments, which outpaced similar moves from other tech peers. For investors, these headlines probably spark the question: is F5 pulling ahead of the pack in an increasingly AI-driven landscape, or is this simply what a rebound looks like for legacy players adapting to new trends?

Stepping back, the last year has been no less intriguing for F5’s stock. Shares are up 61% over the past twelve months, with momentum picking up. The stock has shown a 30% year-to-date gain and a notable 12% climb in the past three months alone. Recent updates have focused on F5’s position as a go-to for secure and scalable app delivery in hybrid and cloud environments, themes that have clearly resonated as investors reward the company’s growth story.

But with shares on the rise and management now raising the bar for future results, is this the moment to consider F5 undervalued, or has the market already priced in its renewed growth outlook?

Advertisement

Most Popular Narrative: Fairly Valued

The most widely followed narrative views F5 as fairly valued at current levels, with the consensus price target only marginally above the recent share price. This outlook is based on expectations of sustained revenue and profit growth, but also recognizes the need for further evidence to justify a higher valuation.

Accelerated enterprise adoption of hybrid multi-cloud architectures and data center modernization is fueling durable demand for F5's application delivery and security solutions. This trend is positioning the company for sustained product and software revenue growth over the next several years.

Want to know what could push F5’s value even higher? The secret lies in aggressive growth forecasts for earnings and margins, plus a discounted cash flow benchmark that sets the bar for fair value. Are bold profit projections and future multiples the backbone of this narrative? Find out what specific financial expectations drive the consensus judgment on valuation.

However, heightened competition and slower adoption of F5’s software offerings could quickly change the story, which may put both future revenue and margin growth at risk.

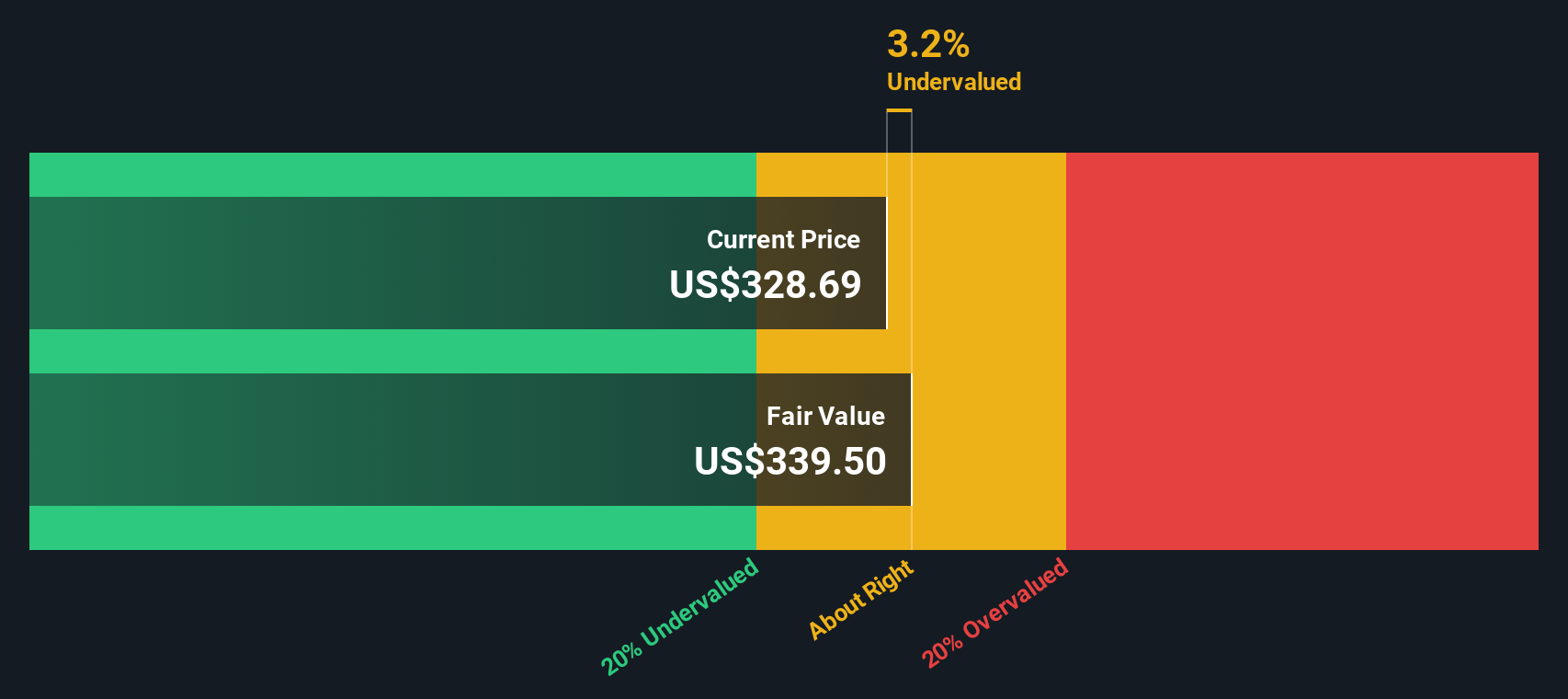

While consensus sees F5 as fairly valued, a look through the lens of our SWS DCF model offers a different perspective. This model suggests the shares might actually be trading below their intrinsic worth. Could the market be missing the longer-term upside?

If you have a different outlook or want to dive into the details yourself, you can build your own perspective in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding F5.

Looking for More Investment Ideas?

Serious investors know that opportunities are not just limited to one standout stock. Do not let new possibilities slip by; use the right tools to seize your next big move right now.

Uncover value by checking out companies flying under the radar with remarkable financial strength in our collection of penny stocks with strong financials.

Tap into breakthroughs reshaping tomorrow’s healthcare by searching for leaders in artificial intelligence advancements across medical tech with healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies