Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:CSCO

Is Cisco’s (CSCO) New SAFE Integration the Next Step Toward Defining Its AI Security Advantage?

- SAFE recently announced a new integration with Cisco, combining Cisco AI Defense telemetry with SAFE's cyber risk platform to offer enterprises real-time, actionable insights for AI security governance.

- This partnership marks a significant advance in enabling organizations to manage AI-specific risks and accelerate secure AI adoption across distributed cloud environments.

- We'll explore how this move to integrate Cisco's AI Defense solution with SAFE's risk management platform could influence Cisco's broader AI-driven investment narrative.

The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Cisco Systems Investment Narrative Recap

To own Cisco Systems today, investors need to believe in the company's ability to grow through AI-centric products, subscription revenue, and robust shareholder returns, while effectively managing integration and competitive risks. The recent SAFE partnership with Cisco, uniting AI Defense telemetry with a leading cyber risk platform, directly supports Cisco’s AI growth catalyst but does not materially shift the short-term risks around major integration efforts or competitive market pressures.

Among recent announcements, Cisco’s unveiling of AI-centric infrastructure innovations, with over US$1 billion in AI infrastructure orders, is most relevant, illustrating how the company is scaling its AI portfolio to address rising enterprise demand. This aligns closely with the SAFE integration, bolstering Cisco’s ambition to remain a leader in secure, AI-driven solutions while reinforcing recurring revenue streams as a vital growth driver.

However, investors should also keep in mind the challenges Cisco faces in realizing complex synergies from recent acquisitions and integrations, as...

Read the full narrative on Cisco Systems (it's free!)

Cisco Systems' outlook anticipates $64.8 billion in revenue and $13.4 billion in earnings by 2028. This implies a 5.2% annual revenue growth rate and an $3.6 billion increase in earnings from the current $9.8 billion.

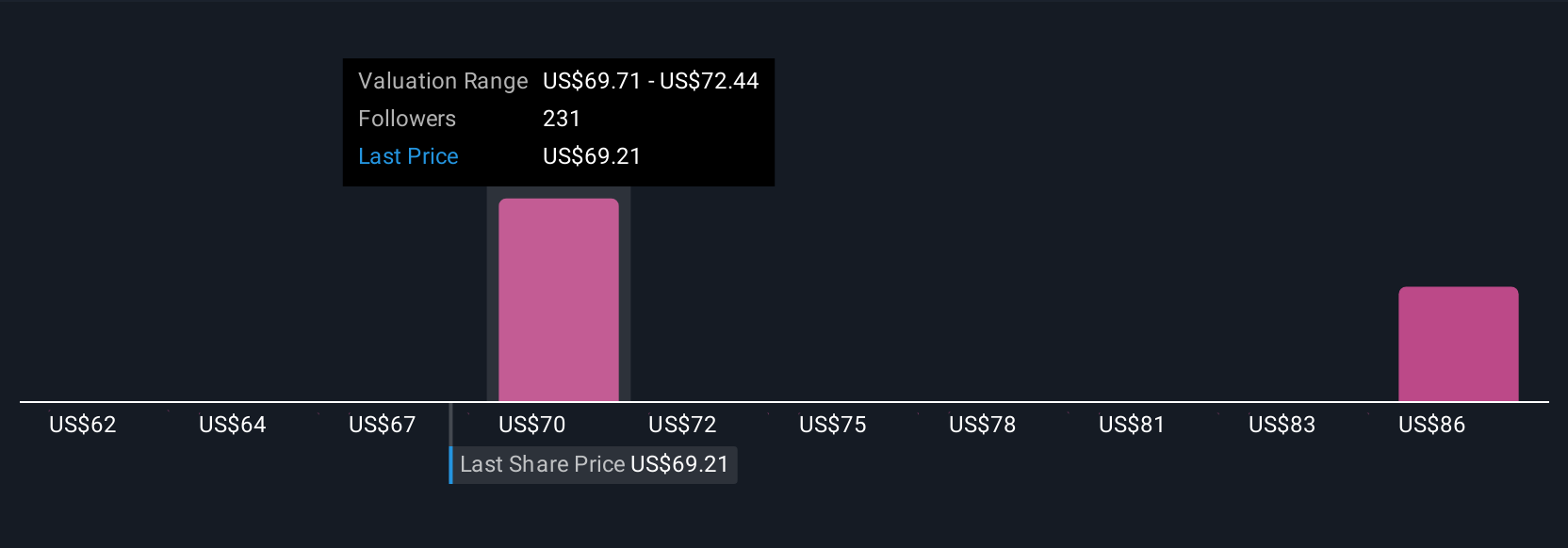

Uncover how Cisco Systems' forecasts yield a $72.29 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members provided nine fair value estimates for Cisco Systems, ranging from US$61.52 to US$88.28 per share. With competitive pressures from white-box and ODM vendors influencing the company’s revenue and margins, reader viewpoints span a broad set of scenarios for Cisco’s future performance.

Explore 9 other fair value estimates on Cisco Systems - why the stock might be worth 14% less than the current price!

Build Your Own Cisco Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cisco Systems research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Cisco Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cisco Systems' overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

25 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative