Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:CSCO

Is Cisco Systems (CSCO) Still Attractive After Recent 9% Share Price Decline?

Reviewed by Bailey Pemberton

- If you are wondering whether Cisco Systems at around US$76.85 is still a sensible entry point or more of a hold, the key question is how its current price compares with its underlying value.

- The share price has seen a 9.4% decline over the last 7 days, while returns sit at 3.3% over 30 days, 1.1% year to date, 21.3% over 1 year, 64.8% over 3 years and 94.4% over 5 years. This gives you a wide range of recent outcomes to think about.

- Recent headlines around Cisco Systems have focused on its position in networking and security, including ongoing attention on how it fits into long term infrastructure and connectivity trends. This background helps explain why the share price can respond quickly when investors reassess the company’s role in these markets.

- Cisco Systems currently has a valuation score of 4 out of 6, reflecting where it screens as undervalued on several checks. Next we will look at the main valuation methods behind that score, then finish with a way to think about value that goes beyond standard models.

Find out why Cisco Systems's 21.3% return over the last year is lagging behind its peers.

Approach 1: Cisco Systems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today’s value to estimate what the business might be worth right now.

For Cisco Systems, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about $12.4b. Analysts provide explicit forecasts for several years, and Simply Wall St then extrapolates further, with projected free cash flow of about $19.8b in 2030 and a full set of annual estimates out to 2035.

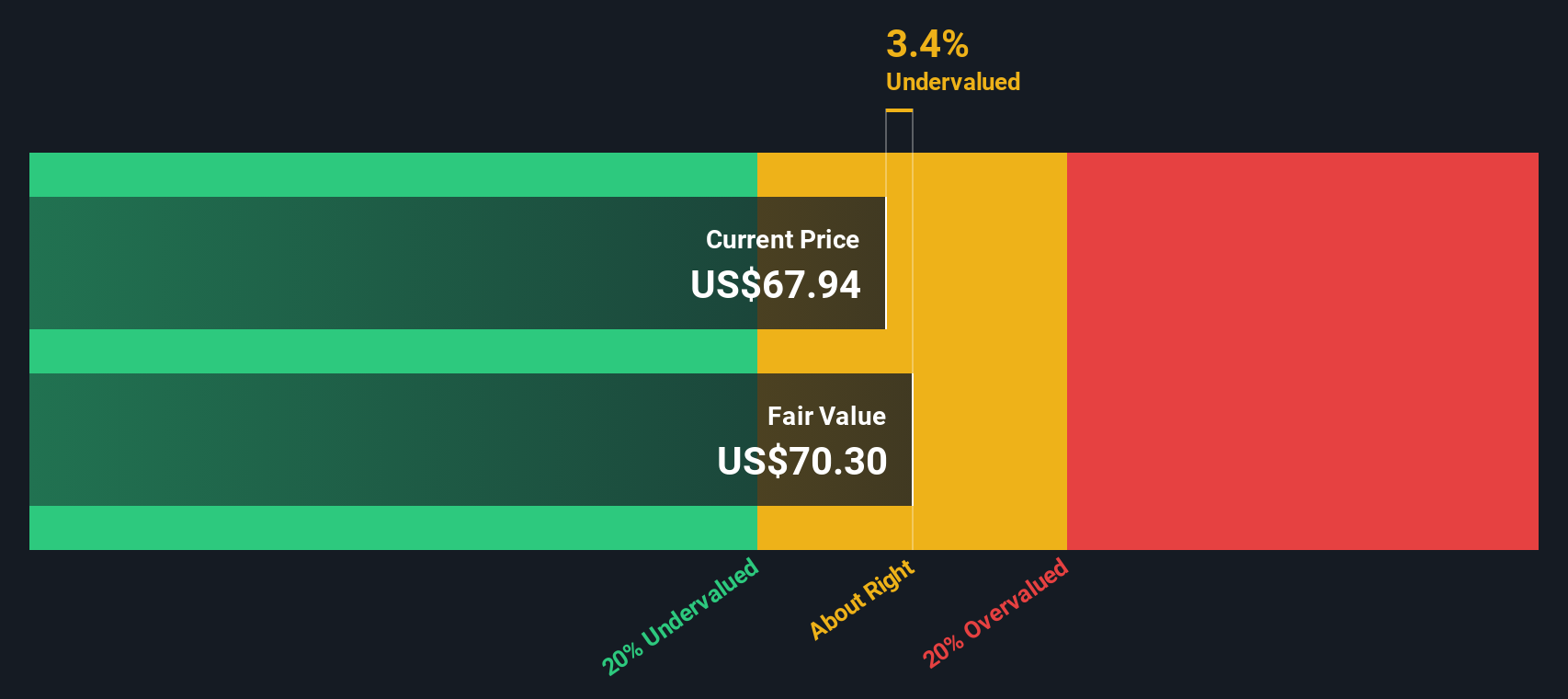

Combining these projections and discounting them back, the model suggests an intrinsic value of about $85.88 per share. Compared with the recent share price around $76.85, this indicates the stock screens as roughly 10.5% undervalued under this method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cisco Systems is undervalued by 10.5%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

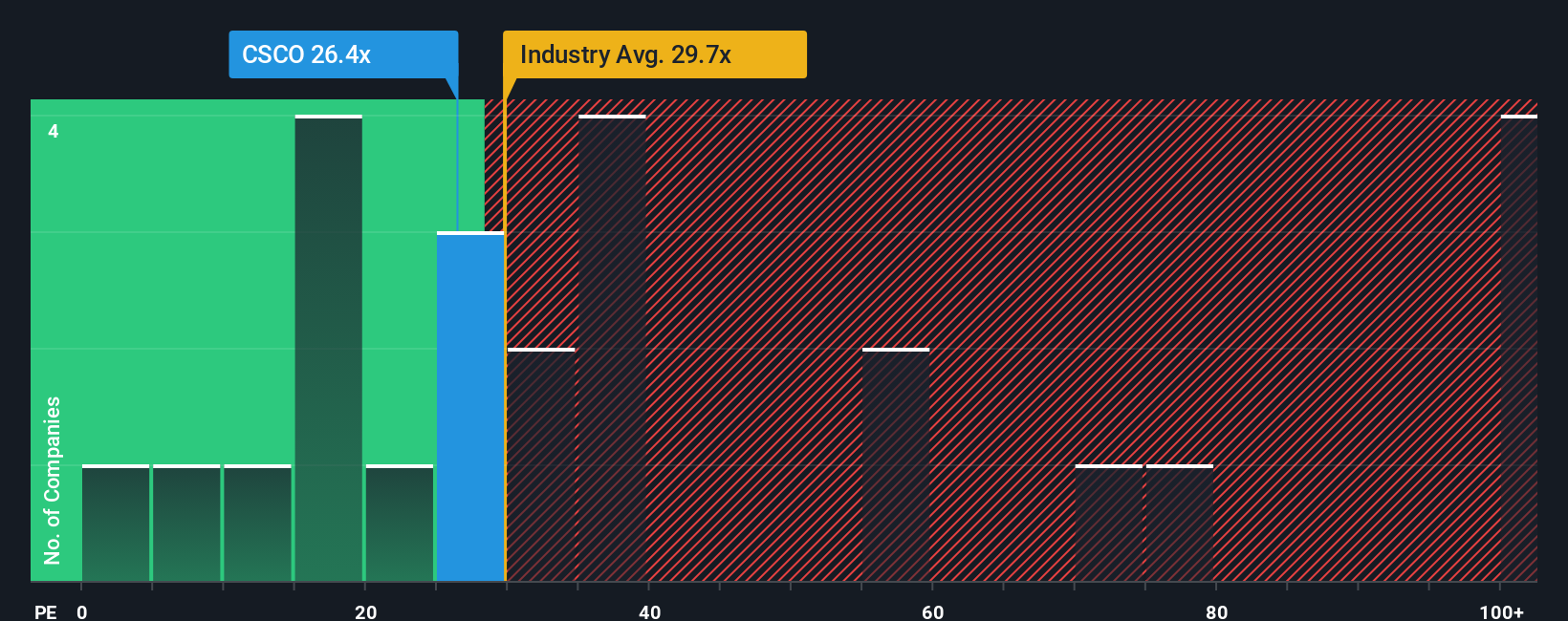

Approach 2: Cisco Systems Price vs Earnings

For a profitable business like Cisco Systems, the P/E ratio is a practical way to think about value because it links what you pay today to the earnings the company is already producing. Investors typically expect higher growth or lower risk to justify a higher P/E, while slower growth or higher risk usually call for a lower, more cautious P/E.

Cisco Systems currently trades on a P/E of 27.41x, compared with the Communications industry average of about 31.56x and a peer average of 73.80x. Simply Wall St also calculates a Fair Ratio of 31.43x for Cisco Systems, which is the P/E level it might trade on given its earnings profile, industry, profit margins, market cap and risk factors.

This Fair Ratio is more tailored than a straight comparison with peers or the broad industry, because it adjusts for Cisco Systems specific characteristics rather than assuming all companies deserve the same multiple. With the current P/E of 27.41x sitting below the Fair Ratio of 31.43x, Cisco Systems appears undervalued using this approach.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Cisco Systems Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St help you turn your view of Cisco Systems into a clear story that links what you think about its AI networking strength, subscription shift, security risks and acquisitions to concrete forecasts for revenue, earnings, margins and a fair value. It then compares that fair value with the current price so you can judge whether Cisco Systems looks closer to the more optimistic narrative with a fair value around US$87 or the more cautious view nearer US$61, all within an easy Community page tool that updates as fresh news or earnings arrive.

Do you think there's more to the story for Cisco Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

70 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

51 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on Palfinger ·

Palfinger’s Valuation Depends On Whether Free Cash Flow Can Hold

Fair Value:€4326.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

Polip on Iovance Biotherapeutics ·

Why I think Iovance is undervalued

Fair Value:US$1876.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

Polip on ABIVAX Société Anonyme ·

OBE is best in disease

Fair Value:€22041.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative