Advertisement

- United States

- /

- Software

- /

- NYSE:BMNR

Bitmine Immersion Technologies (BMNR): Evaluating Valuation After Recent 8% Share Price Jump

Bitmine Immersion Technologies (BMNR) has drawn attention this week following a nearly 8% gain in its stock price. The stock is bouncing back from recent declines, and investors are now considering whether this shift signals a potential turnaround for the company.

See our latest analysis for Bitmine Immersion Technologies.

Bitmine Immersion Technologies’ recent jump comes after a tough month that saw a 23% drop in share price, part of a broader 32% decline over the past 90 days. Still, with a year-to-date share price return of nearly 475% and an outstanding 570% total shareholder return for the past year, momentum remains impressive even as the pace of gains appears to be cooling from earlier highs.

If shifting trends in fast-moving stocks like BMNR interest you, now is an ideal moment to broaden your search and see what you find in the fast growing stocks with high insider ownership.

The company’s volatile swings raise a crucial question for investors: Is Bitmine Immersion Technologies now undervalued given its recent pullback, or is the market already anticipating strong future growth, leaving little room for upside?

Price-to-Book Ratio of 3980.4x: Is it justified?

Bitmine Immersion Technologies carries a sky-high price-to-book ratio of 3980.4x compared to a last close price of $40.23, suggesting significant overvaluation relative to both industry peers and its own fundamentals.

The price-to-book ratio compares a company’s market capitalization to its net assets on the balance sheet. This metric offers a quick snapshot of how much investors are paying for each dollar of book value. For software companies, elevated ratios can sometimes be explained by strong growth prospects or intangible assets, but such an extreme figure demands extra scrutiny.

Bitmine’s price-to-book valuation is much higher than the US software industry average of just 3.7x, as well as the peer average of 16.6x. This disparity highlights an aggressive premium being placed on the stock, which may be difficult to justify given its current unprofitability and lack of near-term forecasts for profit growth. There is no data available for what its fair ratio should be, so the premium may be exposed to a sharp correction if the market reassesses company prospects.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book Ratio of 3980.4x (OVERVALUED)

However, rapid revenue growth may not offset Bitmine’s ongoing losses or justify such a high premium if profitability remains elusive in the near term.

Find out about the key risks to this Bitmine Immersion Technologies narrative.

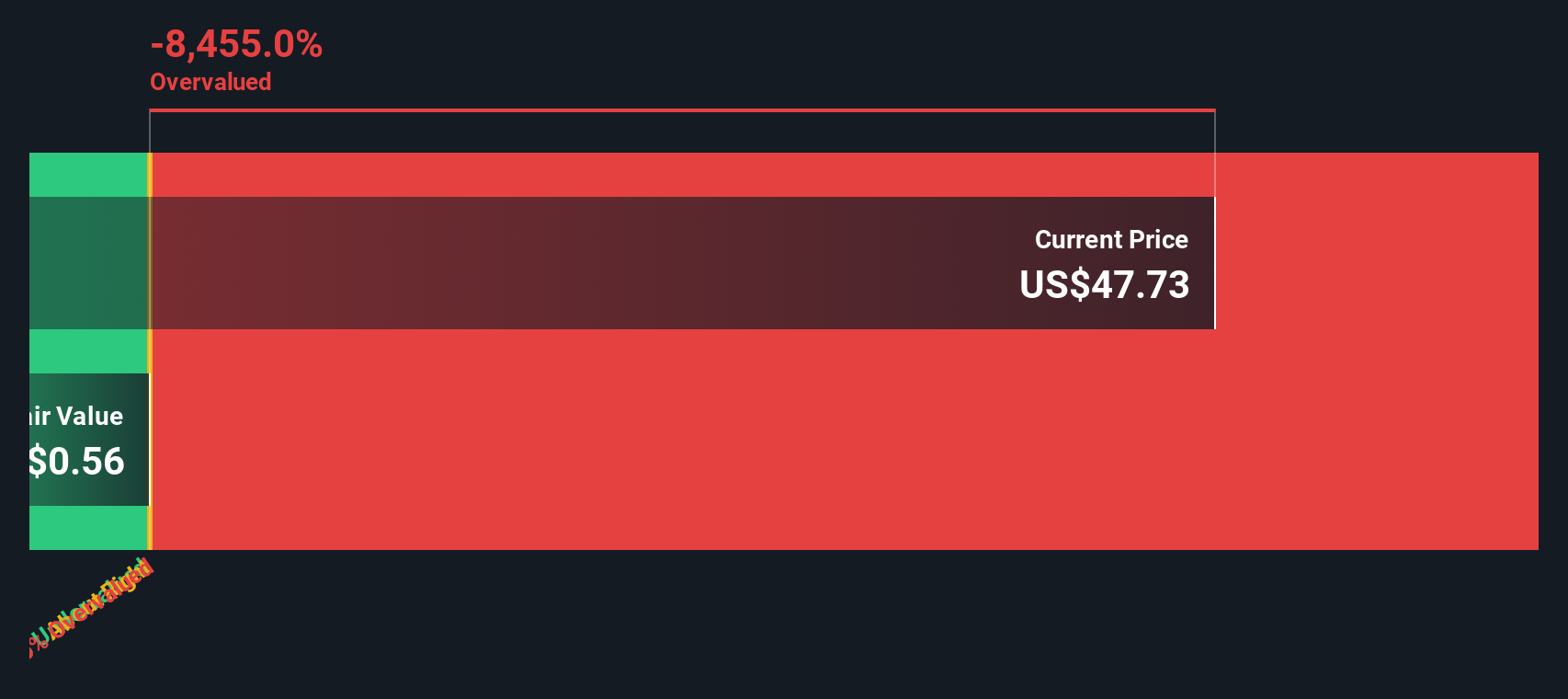

Another View: Discounted Cash Flow Model Poses Further Questions

Taking a different angle, our SWS DCF model suggests Bitmine Immersion Technologies is trading far above its estimated fair value. Shares are at $40.23, while the DCF fair value stands at just $0.35. This significant difference raises fresh doubts about whether the company’s rapid growth alone is sufficient to support its lofty valuation.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bitmine Immersion Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bitmine Immersion Technologies Narrative

If you see the story differently or want to explore the details yourself, you can build your own view from the ground up in just a few minutes. Why not Do it your way.

A great starting point for your Bitmine Immersion Technologies research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Why stop here when you can give your portfolio an edge? Take a few minutes today and seize unique opportunities that could shape your financial future.

- Benefit from rapid tech advancements by tapping into these 25 AI penny stocks, which are making their mark on artificial intelligence and automation.

- Strengthen your income strategy with these 16 dividend stocks with yields > 3%, offering solid yields for consistent cash flow and potential long-term growth.

- Uncover tomorrow’s industry leaders by checking out these 28 quantum computing stocks, which are pushing boundaries in computing innovation and next-level processing power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bitmine Immersion Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BMNR

Bitmine Immersion Technologies

Operates as a blockchain technology company primarily in the United States.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

44 followersusers have followed this narrative

8 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

90 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AL

Alice3D on ServiceNow ·

NOW is an established SAAS positioned for accelerated growth over the next 5 years.

Fair Value:US$15534.1% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Unilever Indonesia ·

Nilai Wajar di Tengah Pemulihan Kinerja

Fair Value:Rp931.1178.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

QU

QuanD on Space Exploration Technologies ·

Making sense of 1.75 trillion IPO

Fair Value:US$13519.2% overvalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative