Advertisement

- United States

- /

- Software

- /

- NYSE:U

How Unity’s Removal From Russell Growth Indexes Will Impact Unity Software (U) Investors

Reviewed by Sasha Jovanovic

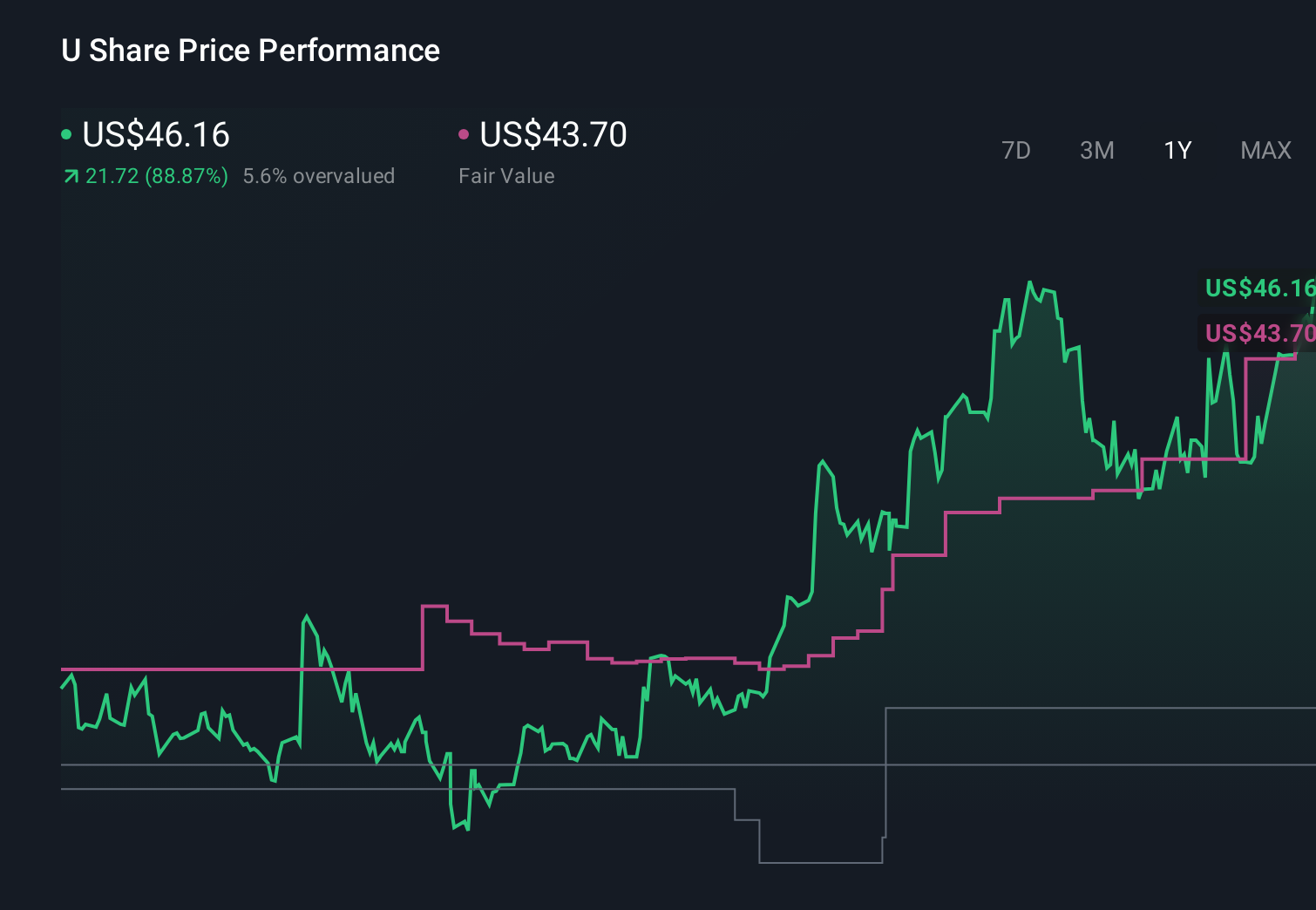

- In late June 2026, Unity Software Inc. (NYSE: U) was removed as a constituent from several major Russell growth indexes, including the Russell 1000 Growth and Russell Midcap Growth benchmarks.

- This broad index exclusion reshapes how Unity screens for growth-style funds, potentially altering its institutional investor mix without directly changing its underlying business trajectory.

- Next, we’ll examine how Unity’s removal from multiple Russell growth benchmarks may interact with its AI-focused growth narrative and analyst expectations.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Unity Software Investment Narrative Recap

To own Unity, you need to believe its engine and AI tools can turn heavy R&D and expansion outside gaming into durable, profitable growth. The near term focus remains on whether Unity can narrow substantial losses while growing revenue. Its broad removal from Russell growth indexes may affect trading flows and some institutional ownership, but it does not materially change the core earnings trajectory or the key risk that expenses stay high without clear progress toward profitability.

The most relevant recent development is Unity’s updated Q2 2026 revenue guidance of US$505 million to US$515 million, following Q1 2026 revenue of US$508.24 million alongside a US$347.61 million net loss and sizeable impairments. Against the backdrop of index removals, this guidance keeps attention squarely on whether Unity can convert its AI and non gaming initiatives into improving unit economics rather than just higher top line scale.

Yet beneath the AI promise, investors should be aware that Unity’s persistent losses and high R&D spend could...

Read the full narrative on Unity Software (it's free!)

Unity Software's narrative projects $3.0 billion revenue and $513.7 million earnings by 2029. This requires 16.0% yearly revenue growth and a $1,186.4 million earnings increase from -$672.7 million today.

Uncover how Unity Software's forecasts yield a $35.28 fair value, a 20% upside to its current price.

Exploring Other Perspectives

By contrast, the lowest analysts were already cautious, projecting about US$2.7 billion revenue and US$435.5 million earnings by 2029, so Unity’s index exit could further test those assumptions.

Explore 7 other fair value estimates on Unity Software - why the stock might be worth just $35.28!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Unity Software research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Unity Software research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unity Software's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.0% undervalued

88 followersusers have followed this narrative

0 commentsusers have commented on this narrative

22 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

56 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

29 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

MO

Momentum_Heron_abxu on Nintendo ·

Nintendo facing the Ram shortage situation

Fair Value:JP¥8k10.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lenny67 on Agnico Eagle Mines ·

Is This Micro-Cap the Secret Solution to Agnico Eagle’s Multi-Year Production Crisis? (CSE: RFR | NYSE: AEM)

Fair Value:US$123.91k99.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lenny67 on Renforth Resources ·

The Strategic Arbitrage at Parbec: Why Renforth Holds the Cards

Fair Value:CA$0.1586.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

83 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Trending Discussion

PR

ProjectKai on Iovance Biotherapeutics ·

Polip, this is Kai. When do you estimate IOVA could reach a $12–20 billion valuation, implying rough...

0

|0