Advertisement

- United States

- /

- Software

- /

- NYSE:U

Do Confident Analyst Upgrades on Unity (U) Outweigh Insider Selling and AI Competitive Uncertainty?

Reviewed by Sasha Jovanovic

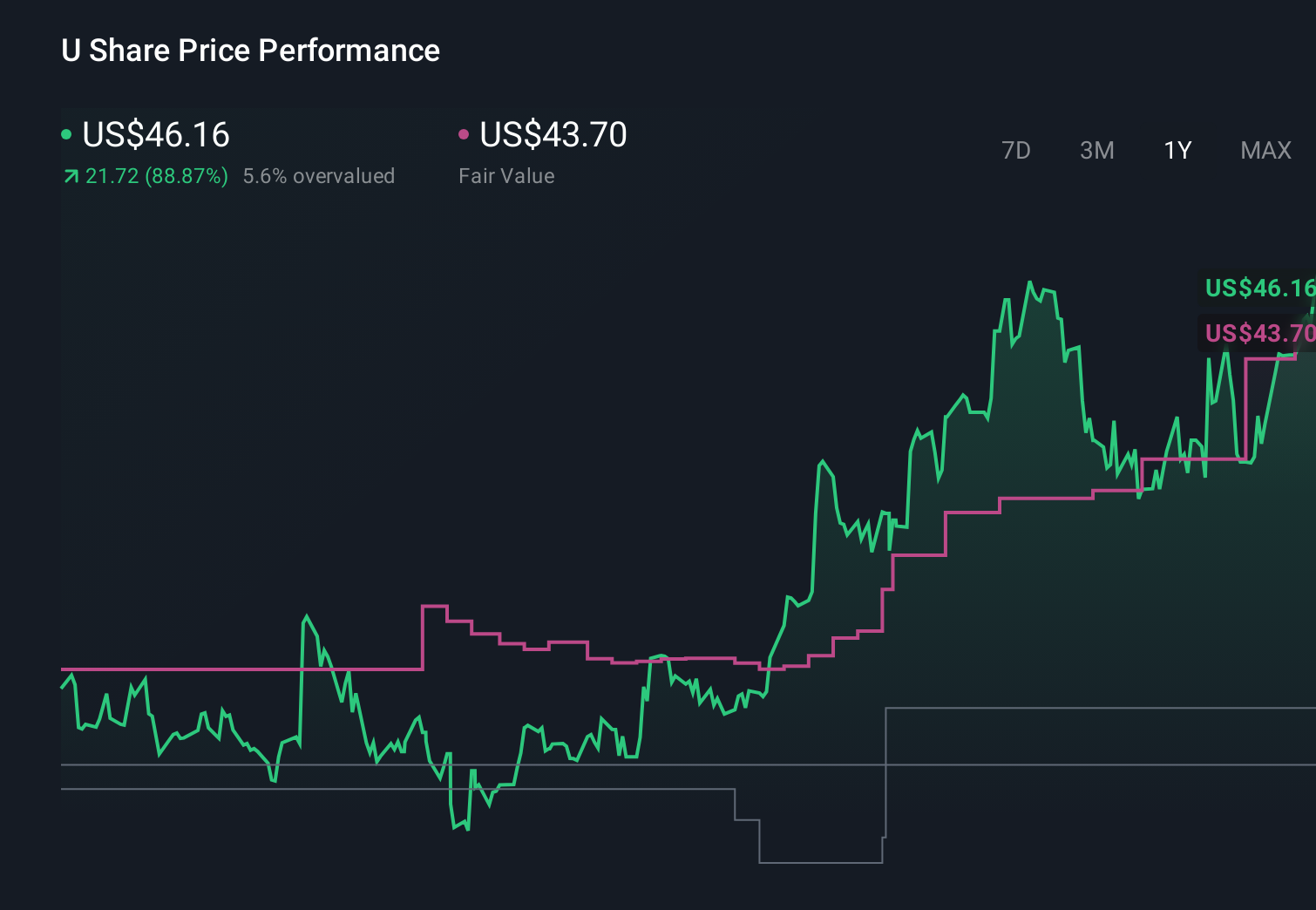

- In recent weeks, Unity Software has attracted renewed attention as multiple research firms reiterated or upgraded positive ratings and raised earnings forecasts, while options activity and analyst commentary underscored expectations for improving margins despite softer revenue growth and sector-wide concern about AI’s impact on software providers.

- At the same time, investors are weighing upbeat analyst sentiment and stronger earnings estimates against insider share sales and worries that AI and competitive pressures could challenge Unity’s longer-term positioning.

- We’ll now examine how this more optimistic earnings outlook, alongside reaffirmed positive analyst ratings, reshapes Unity Software’s investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Unity Software Investment Narrative Recap

To own Unity, you need to believe its real time 3D and AI tools can offset competitive and AI‑related pressures while improving profitability. The latest analyst upgrades and higher EPS estimates support the near term catalyst of margin improvement, but the sharp share pullback and insider selling keep execution risk and competitive threats front and center. Overall, the recent news reinforces the focus on earnings quality more than it changes Unity’s biggest risk profile.

Among the recent developments, Wedbush’s reiterated Outperform rating and the broader consensus “Outperform” stance stand out, especially as analysts raise EPS forecasts despite moderating revenue growth. This positive shift in earnings expectations directly connects to Unity’s margin expansion story and heightens attention on whether management can sustain cost discipline while investing in AI and new products such as Unity 6 and Unity Vector.

Yet against this more upbeat earnings narrative, investors should be aware that insider selling and AI driven competitive risks could still...

Read the full narrative on Unity Software (it's free!)

Unity Software's narrative projects $2.3 billion revenue and $313.8 million earnings by 2028. This requires 9.3% yearly revenue growth and a $747.7 million earnings increase from -$433.9 million today.

Uncover how Unity Software's forecasts yield a $47.47 fair value, a 140% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously modeling Unity to reach about US$2.5 billion in revenue and roughly US$312 million in earnings, which is far more bullish than consensus. When you compare that optimism with the current AI and competition worries highlighted by recent news, you can see how differently people can view Unity’s future and why it is worth exploring several alternative viewpoints before deciding where you stand.

Explore 9 other fair value estimates on Unity Software - why the stock might be worth just $24.17!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Unity Software research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Unity Software research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unity Software's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

140 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.3% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.3% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3651.4% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Nebius Group ·

Nebius Group NV (NBIS): The AI Infrastructure Pivot and the Meta Super-Contract

Fair Value:US$132.62.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Intel ·

Intel Corp (INTC): The 18A Node Pivot and the "Foundry First" Transformation

Fair Value:US$3338.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

Bigd on Volatus Aerospace ·

Strong buy

Fair Value:CA$1.0516.2% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.8% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.3% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.9% undervalued

1312 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0