Advertisement

- United States

- /

- Software

- /

- NYSE:TYL

Tyler Technologies (TYL): Evaluating Valuation After a Notable Three-Month Share Decline

Tyler Technologies (TYL) shares have been on a downward trend over the past three months, declining roughly 18%. This follows a period of outsized growth in prior years, and now the software company faces a more challenging environment.

See our latest analysis for Tyler Technologies.

Over the past year, Tyler Technologies’ share price has steadily lost ground alongside several high-profile software firms, with a 1-year total shareholder return of -21%. That pullback comes despite a solid multi-year run; its 3-year total return still sits at an impressive 65%. Momentum is clearly fading now as the latest quarter’s dip adds to investor caution around the stock’s valuation and growth pace.

If volatility in software stocks has you rethinking your strategy, now’s a great moment to broaden your search and discover fast growing stocks with high insider ownership

With shares still well below analyst price targets and healthy financial growth, investors now face the big question: is Tyler Technologies being overlooked, or is the recent weakness simply a sign that all the future upside is already priced in?

Most Popular Narrative: 28.3% Undervalued

With Tyler Technologies trading at $476.26, the most widely followed narrative places fair value sharply higher, highlighting a compelling gap to the market price. This setup suggests investors are significantly discounting the company’s prospective growth and profitability.

Ongoing investment in AI-powered tools and automation, evident in product launches like the AI-driven Resident Assistant and enhanced budgeting solutions, caters to public sector labor challenges and the need for data-driven decision-making. This enables premium pricing, reduces customer churn, and unlocks scalable margin improvements over time.

Curious why high-margin expansion and bold tech bets have analysts so bullish? The real surprise comes from the projected leaps in both top-line growth and profit margins. See exactly which aggressive assumptions fuel this upside view—key financial levers may catch investors off guard.

Result: Fair Value of $664.06 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent reliance on government budgets and unpredictable deal cycles may limit Tyler Technologies’ long-term earnings visibility and growth momentum.

Find out about the key risks to this Tyler Technologies narrative.

Another View: Multiples Tell a Cautionary Tale

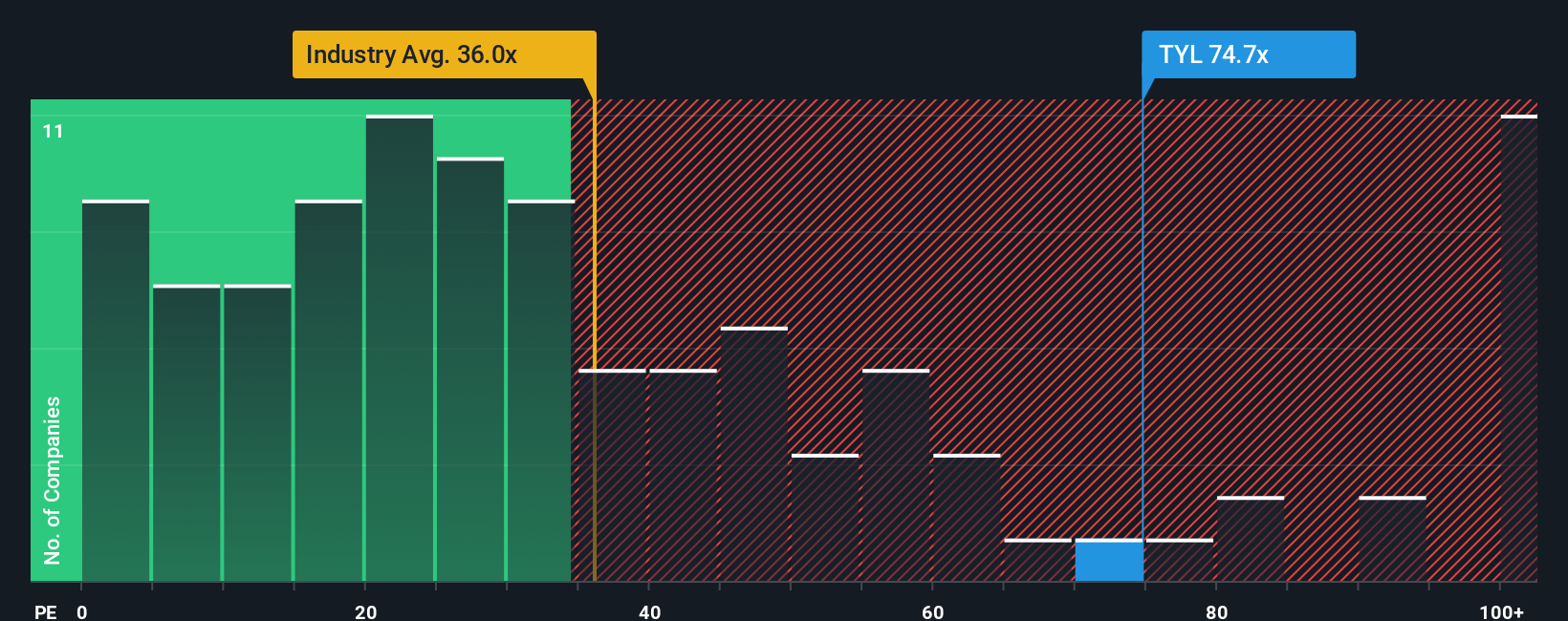

While some see Tyler Technologies as undervalued based on projected growth, the market’s go-to gauge tells a different story. Its price-to-earnings ratio stands at 65x, far above both the US Software industry average of 34.1x and the fair ratio of 35.1x. This premium could mean that the market is already pricing in a lot of future growth. What happens if reality falls short?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Tyler Technologies Narrative

If you see things differently or want to dig into the numbers firsthand, you can build your own analysis and perspective in just minutes using the tools available. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Tyler Technologies.

Looking for More Investment Ideas?

Don’t settle for just one opportunity. Explore handpicked investment themes that could shape your portfolio and help set you ahead of the crowd.

- Unlock steady income potential by reviewing these 22 dividend stocks with yields > 3% offering standout yields and long-term stability. This is ideal for investors seeking reliable returns.

- Spot emerging trends and increase your exposure to artificial intelligence breakthroughs with these 26 AI penny stocks set to transform tomorrow’s industries.

- Capture unique growth prospects in the rapidly evolving digital asset space through these 81 cryptocurrency and blockchain stocks, where innovation meets opportunity for forward-looking investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tyler Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TYL

Tyler Technologies

Provides integrated software and technology management solutions for the public sector in the United States.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5370.8% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HegelBayeBagel on PlaySide Studios ·

PlaySide Studios: Market Is Sleeping on a Potential 10M+ Unit Breakout Year, FY26 Could Be the Rerate of the Decade

Fair Value:AU$0.8460.7% undervalued

12 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.278.3% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TH

TheValueDetector on Cognyte Software ·

This isn’t speculation — this is confirmation.A Schedule 13G was filed, not a 13D, meaning this is passive institutional capital, not acti

Fair Value:US$95.6792.9% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.220.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

Bradleywang on Marriott International ·

Asset-Light but Valuation-Heavy: A Fundamental Breakdown of Marriott ($MAR)

Fair Value:US$313.9410.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CT

ctmlin910 on Novo Nordisk ·

Why did Novo Nordisk flop?

Fair Value:DKK 2874.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.9% undervalued

61 followersusers have followed this narrative

5 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.4% undervalued

1295 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3638.1% undervalued

48 followersusers have followed this narrative

19 commentsusers have commented on this narrative

22 likesusers have liked this narrative