Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:XYZ

Buy Now, Pay Later. Evaluating Square's (NYSE:SQ) Acquisition of Afterpay

Square, Inc. ( NYSE:SQ ) just announced plans to acquire Afterpay ( ASX:APT ) in an all shares transaction worth US$26 billion. The transaction is expected to close in the first quarter of calendar year 2022.

What is Afterpay, and will the transaction create or destroy value?

Afterpay enables merchants to offer their clients the option to buy now and pay later in multiple installments. Square plans to integrate Afterpay into their CashApp and Seller ecosystems. This is arguably a very good thing for consumers and a right direction in building a trusted brand.

As of June 30, 2021, Afterpay serves more than 16 million consumers and nearly 100,000 merchants globally, including major retailers across key verticals such as fashion, homewares, beauty, sporting goods etc. So it is clear that Square expects the addition to bolster growth by allowing affordable purchasing options for consumers.

As a reflection on the strategic implications of the feature, it seems to be a very smart move. Low income consumers, especially in developing economies, are all too familiar with the concept of paying in installments, and this kind of behavior is even further expressed in economic stagnation.

Now that we know what Square is buying, and that is makes sense, let's go over the costs and what that means for shareholders in the long run.

First, we should note that the transaction is all equity, based on the closing price of Square common stock on July 30, 2021, at which point the stock was trading at US$247 per share. This means that Square will have to issue new shares and dilute current shareholders, but paying for a transaction with their strongest asset might just be worth it.

Acquisitions are complex and very hard to get right. Companies have 2 options to use in acquisitions, 1 is to pay with cash or debt, and the second is to pay with equity/issuing shares. Sometimes they can find a mix between the two. It is important for companies to use their strongest asset and not overpay for an acquisition.

In the case of Square, we will take a look at their share price and see if the choice to use stock was the smart move.

Looking at the big picture, Square's share price is 2,118% higher than it was five years ago. That means investors were quite enthusiastic about the future of this company and may have given them excess capacity to pull off moves just like this one.

It seems that Square has indeed chosen its strongest asset to pay for the acquisition. On the other hand, shareholders are left with the bill and might not appreciate overpaying for a company, as this kind of behavior can actually destroy value.

Lastly, we will take a look at the growth prospects for Square before the announcement and note that should the deal go through, Square will need to deliver even more growth than previously estimated.

Check out our latest analysis for Square

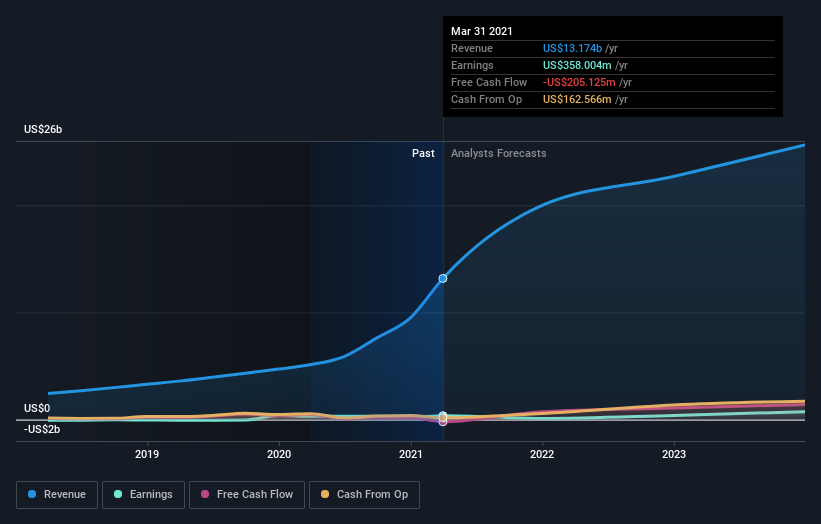

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

While Square made a small profit, in the last year, we think that the market is probably more focussed on the top line growth at the moment. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

In the last 5 years Square saw its revenue grow at 42% per year. Even measured against other revenue-focussed companies, that's a good result. Arguably, this is well and truly reflected in the strong share price gain of 86% (per year) over the same period.

Conclusion

Acquisitions have two sides, a great company and appropriate payment. We can envision how Afterpay is a great addition to Square as a feature and a growth opportunity.

However, investors should be mindful of the price - US$29b is quite the sum, and a very hard number to outgrow in the short term. This may lead to a short to medium downfall of the stock. We hope that Square smoothly integrates the features in order to start seeing results as soon as possible.

Consider for instance, the ever-present specter of investment risk. We've identified 4 warning signs with Square (at least 2 which shouldn't be ignored) , and understanding them should be part of your investment process.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Block might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:XYZ

Block

Block, Inc., together with its subsidiaries, builds ecosystems focused on commerce and financial products and services in the United States and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor