Snowflake (SNOW) shares have seen some ups and downs lately, leaving investors curious about what could drive its next move. As valuation debates continue, the stock’s year-to-date return stands out in comparison to software peers.

Despite a recent pullback, as Snowflake’s share price is down 6.24% over the past week, the stock has built significant momentum this year. It has delivered a year-to-date share price return of over 60% and an impressive total shareholder return of nearly 96% over the past twelve months. That kind of performance has investors weighing whether the growth story can continue at this pace, especially after such a sharp move.

If Snowflake’s latest run has you wondering what else is gaining steam, it could be the perfect time to explore See the full list for free.

With impressive gains on the board, investors are left to wonder whether Snowflake is trading below its true value or if rapid growth expectations are already built into the current price. Is there still a buying opportunity here, or is the market simply pricing in years of future growth?

Advertisement

Most Popular Narrative: 5.1% Undervalued

The current fair value narrative suggests Snowflake’s shares may have a modest upside from the last close of $252.98. This sets the stage for an intriguing debate around its next move.

Rapid product innovation, including the launch of approximately 250 new features and expanded offerings such as Snowflake Intelligence, Cortex AI SQL, and Postgres support, is increasing average revenue per user and deepening customer stickiness, which should drive recurring revenue and long-term topline growth.

Curious what bold revenue projections and margin ambitions fuel this premium? The underlying model weaves together explosive expansion, sticky customer growth, and a leap of faith on future profitability. Find out which levers drive valuation and learn what makes this narrative both exciting and controversial.

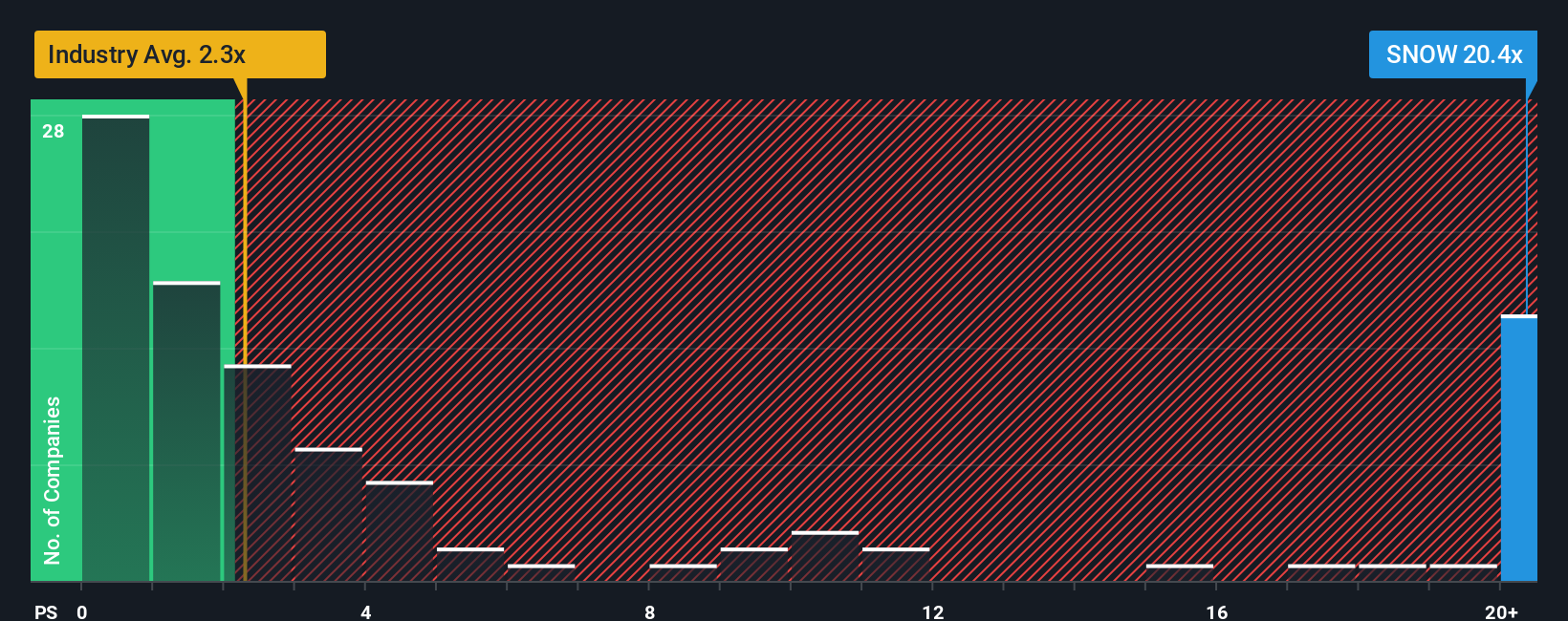

Snowflake’s valuation stands out when judged by its price-to-sales ratio of 20.8x. This is far above both the US IT industry average (2.4x) and its peer group (19.6x). Even compared to a fair ratio of 15.9x, the current premium is striking and raises questions about valuation risk if market trends change.

Why limit your growth to just one stock? Act now and unlock new opportunities by using the Simply Wall Street Screener to uncover leading-edge companies that match your strategy.

Grab income potential with stable, high-yield investments. Check out these 15 dividend stocks with yields > 3% for stocks delivering market-beating dividends above 3%.

Seize the promise of the digital frontier by reviewing these 81 cryptocurrency and blockchain stocks for cutting-edge businesses innovating in cryptocurrency and blockchain technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks