Advertisement

- United States

- /

- Software

- /

- NYSE:PCOR

Procore Technologies (PCOR): Reassessing Valuation After New AI Suite, AWS Deal and CEO Transition

Procore Technologies (PCOR) just lined up three meaningful catalysts at once: its new Groundbreak AI suite, an expanded AWS partnership, and an incoming CEO, all converging ahead of the next earnings stretch.

See our latest analysis for Procore Technologies.

Those moves are arriving just as momentum has quietly improved, with an 8.6 percent 1 month share price return and a solid 3 year total shareholder return of about 53 percent, despite a softer 1 year total shareholder return.

If Procore’s AI push has you thinking more broadly about digital transformation, it could be a good moment to explore other high growth tech and AI stocks that might be setting up for similar growth stories.

With revenue still growing double digits, but shares sitting roughly 9 percent below their 1 year level and about 12 percent under analyst targets, is this setting up a fresh entry point, or is the market already banking on future growth?

Most Popular Narrative Narrative: 11.2% Undervalued

With Procore Technologies last closing at $76.79 against a narrative fair value of $86.44, the valuation case hinges on aggressive long term assumptions.

The demonstrated operating leverage from recent go to market changes and increased sales efficiency is already delivering improved operating margins; management's commitment to further expand margins (targeting 25% 40% FCF margins long term) suggests future earnings and cash flow growth may be underestimated in current valuations.

Curious how a still unprofitable construction software platform earns such a rich future multiple? The narrative leans on bold margin expansion and compounding revenue. Want to see which specific growth and profitability paths are baked into that fair value?

Result: Fair Value of $86.44 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside depends on continued construction spending and successful global expansion, both of which could stall if macro conditions worsen or if competitive pressure intensifies.

Find out about the key risks to this Procore Technologies narrative.

Another View Using Market Ratios

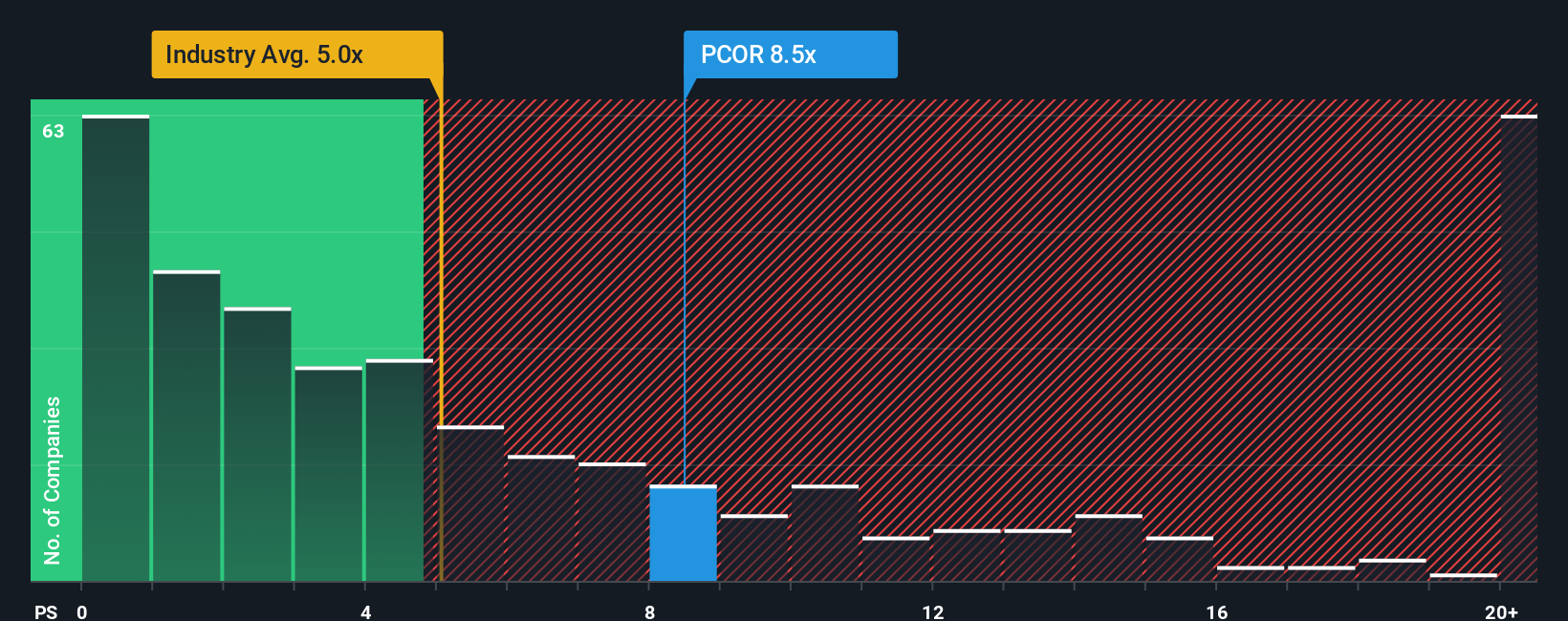

While the narrative fair value suggests upside, the market’s own yardsticks tell a cooler story. On a price to sales of 9.4 times versus a fair ratio of 7.4 times, and 4.9 times for the wider US software space and 8 times for peers, Procore looks richly priced, leaving less margin for error if growth or margins disappoint.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Procore Technologies Narrative

If this perspective does not match your own, or you would rather dig into the numbers yourself, you can build a custom view in just minutes, Do it your way.

A great starting point for your Procore Technologies research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Use the Simply Wall St Screener now to uncover focused, data driven opportunities that others are missing, before the next wave of market interest hits.

- Find potential growth at lower prices by targeting companies that look overlooked on cash flows with these 908 undervalued stocks based on cash flows.

- Explore innovation in automation, data, and software by reviewing these 26 AI penny stocks.

- Identify income opportunities while rates shift by scanning these 15 dividend stocks with yields > 3% for dividend-paying companies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PCOR

Procore Technologies

Provides a cloud-based construction management platform and related products and services in the United States and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5360.5% undervalued

135 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.1% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

12 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.315.7% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2454.2% undervalued

30 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥2.28k36.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Unicycive Therapeutics ·

Unicycive Therapeutics is a late-stage clinical biotech transitioning toward commercialization

Fair Value:US$9.177.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Guming Holdings ·

A scaled, high-growth, franchise-driven beverage leader with strong penetration in China

Fair Value:HK$47.5650.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

108 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.226.0% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74016.7% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative