Advertisement

- United States

- /

- Software

- /

- NYSE:PCOR

Pinning Down Procore Technologies, Inc.'s (NYSE:PCOR) P/S Is Difficult Right Now

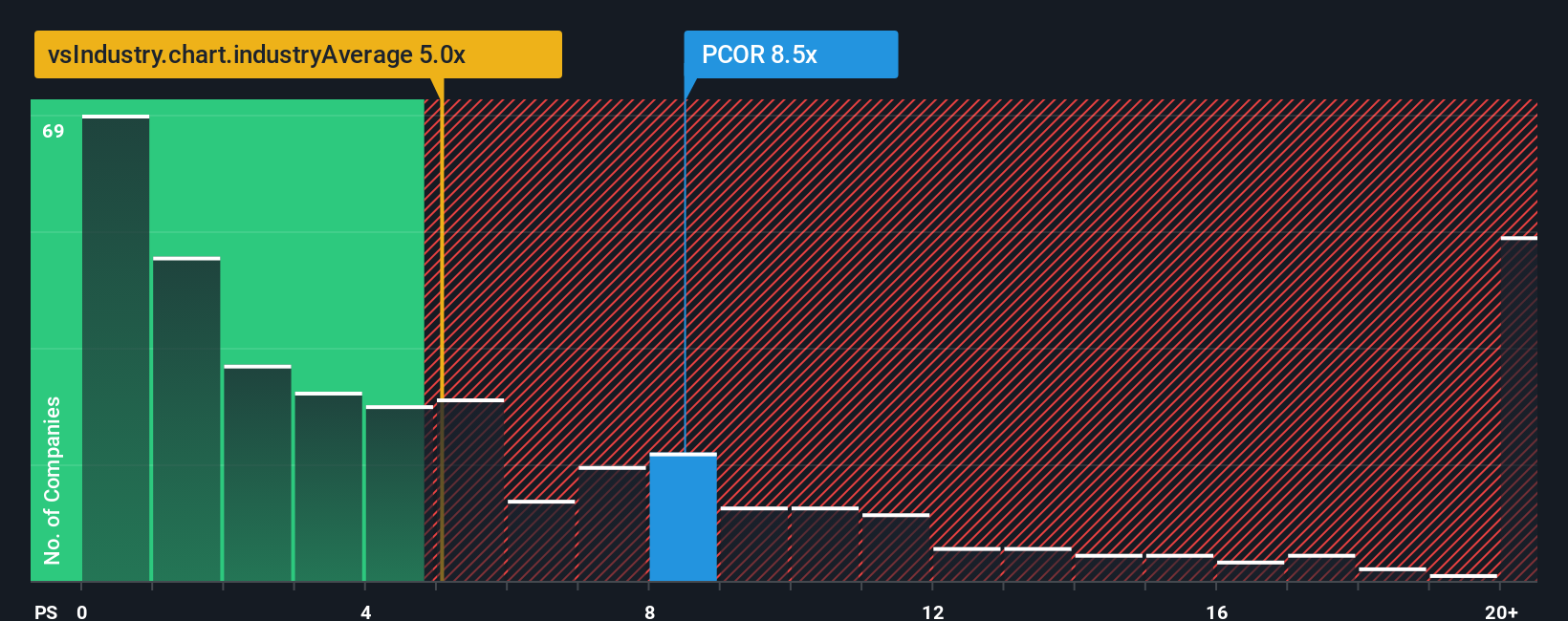

You may think that with a price-to-sales (or "P/S") ratio of 8.5x Procore Technologies, Inc. (NYSE:PCOR) is a stock to avoid completely, seeing as almost half of all the Software companies in the United States have P/S ratios under 5x and even P/S lower than 1.9x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Procore Technologies

How Procore Technologies Has Been Performing

Recent times have been advantageous for Procore Technologies as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Procore Technologies.Is There Enough Revenue Growth Forecasted For Procore Technologies?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Procore Technologies' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 19% gain to the company's top line. The latest three year period has also seen an excellent 113% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 14% per year during the coming three years according to the analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 16% per annum, which is not materially different.

In light of this, it's curious that Procore Technologies' P/S sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Given Procore Technologies' future revenue forecasts are in line with the wider industry, the fact that it trades at an elevated P/S is somewhat surprising. Right now we are uncomfortable with the relatively high share price as the predicted future revenues aren't likely to support such positive sentiment for long. Unless the company can jump ahead of the rest of the industry in the short-term, it'll be a challenge to maintain the share price at current levels.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Procore Technologies that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PCOR

Procore Technologies

Provides a cloud-based construction management platform and related products and services in the United States and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.7% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.9% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38027.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.7% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

CE

CE on Oklo ·

High risk, unproven, but with big potential.

Fair Value:US$5518.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DO

DownUnder on Broadcom ·

Broadcom will keep strong with a 30% Revenue Growth Driven by AI Demand

Fair Value:US$456.568.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AshleighG on SharkNinja ·

Everyone Owns a Ninja. That Doesn't Make It Cheap.

Fair Value:US$110.7311.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.8% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.7% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.0% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

FR

FrontierTom on United States Antimony ·

Great Long term play that needs great tolerance for price swings along the way.

0

|0