Advertisement

- United States

- /

- IT

- /

- NYSE:NET

Assessing Cloudflare (NET) After Recent Security Headlines And A 3-Year Price Surge

Reviewed by Bailey Pemberton

- If you are wondering whether Cloudflare's share price still lines up with its underlying worth, you are not alone. This article will walk through what that value picture looks like.

- Cloudflare closed at US$179.98, with returns of 5.7% over the last 7 days, a 1.5% decline over 30 days, an 8.2% decline year to date and 4.3% over the past year, while the 3 year return is very large and the 5 year return sits at 119.3%.

- Recent headlines have focused on Cloudflare's role in internet security and content delivery, as investors weigh how its services fit into long term digital infrastructure trends. That backdrop helps explain why the share price has seen both pullbacks and rebounds as the story continues to develop.

- Right now, Cloudflare scores 0 out of 6 on our valuation checks. Next we will look at what different valuation methods say about the stock today and then finish with a more complete way of thinking about value beyond a single score.

Cloudflare scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Cloudflare Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today to arrive at an estimate of what the business might be worth now.

For Cloudflare, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $269.4 million. Analyst estimates and Simply Wall St extrapolations point to projected free cash flow of $1.469b by 2030, with a detailed path of annual projections between 2026 and 2035 that are then discounted back to today in US dollars.

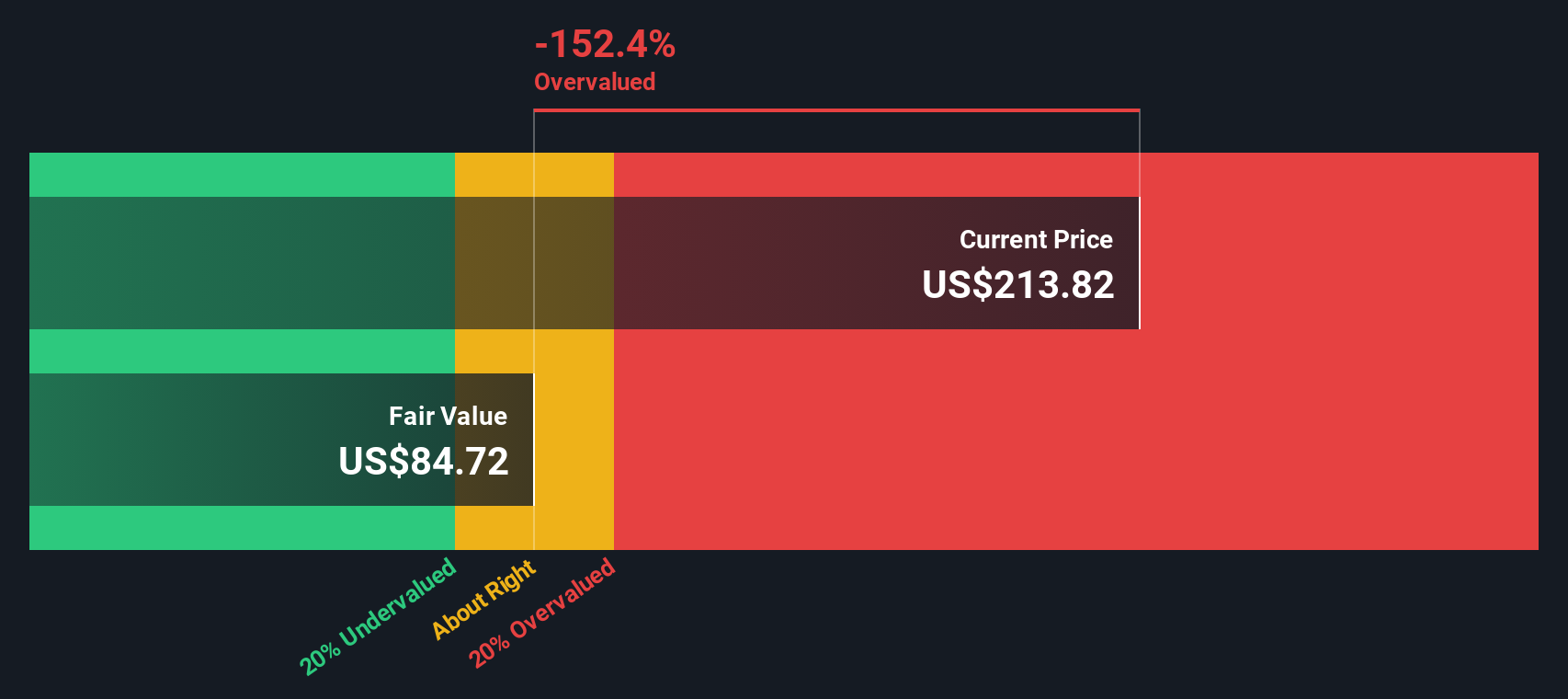

When all those discounted cash flows are added up, the DCF model suggests an estimated intrinsic value of about $85.42 per share. Compared with the recent share price of US$179.98, this implies the stock is around 110.7% overvalued according to this method.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cloudflare may be overvalued by 110.7%. Discover 51 high quality undervalued stocks or create your own screener to find better value opportunities.

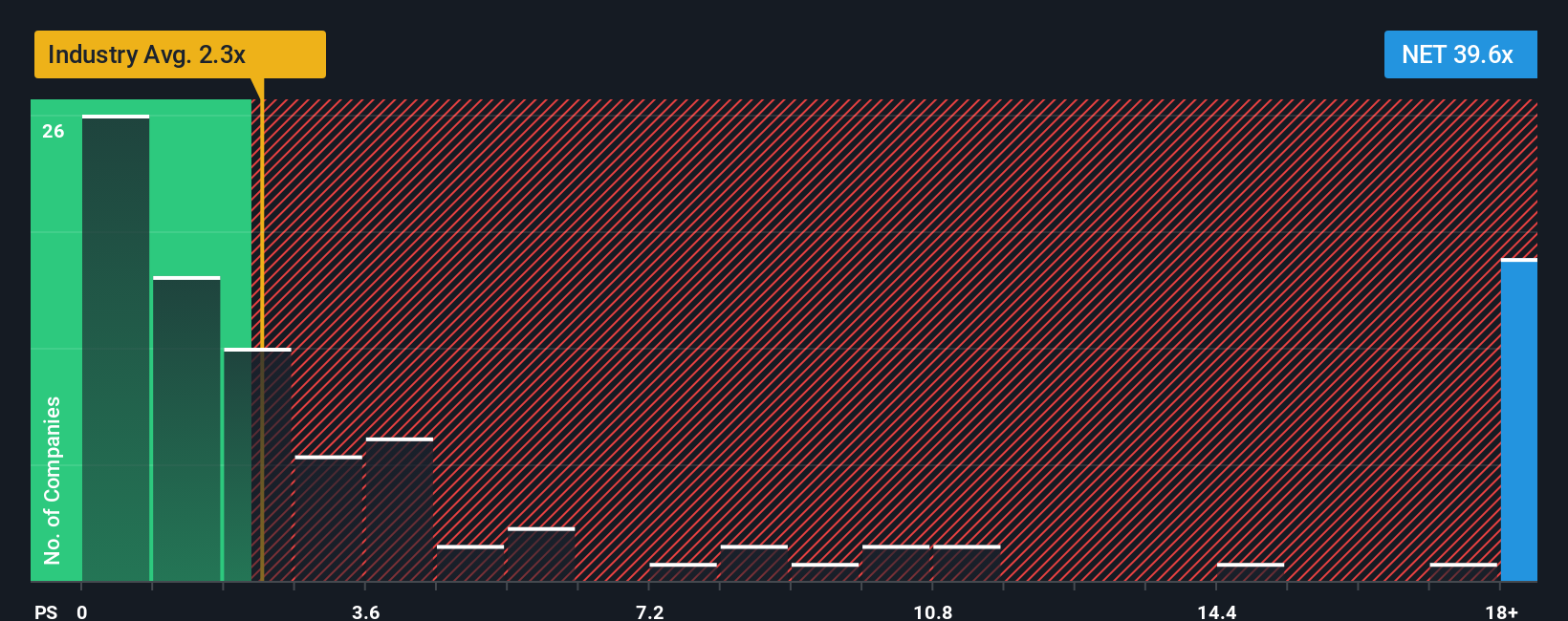

Approach 2: Cloudflare Price vs Sales

For a business like Cloudflare, where investors place a lot of weight on revenue traction, the P/S ratio is a useful way to think about valuation because it compares the share price directly with the sales the company is generating.

In general, the higher the growth expectations and the lower the perceived risk, the more investors are willing to pay for each dollar of sales, which usually shows up as a higher P/S multiple. If growth expectations are more modest or risk is seen as higher, a lower multiple is often viewed as more typical.

Cloudflare currently trades on a P/S ratio of 31.31x. That sits well above the IT industry average P/S of 2.05x and also above the peer average of 13.79x. Simply Wall St’s Fair Ratio for Cloudflare is 13.37x. This is a proprietary estimate of what the P/S multiple might be, given factors such as earnings growth, industry, profit margins, market cap and key risks. This Fair Ratio can be more informative than a straight peer or industry comparison because it attempts to adjust for the company’s specific characteristics rather than using broad group averages. Comparing the current 31.31x to the Fair Ratio of 13.37x suggests the stock is trading at a richer level than that benchmark.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Cloudflare Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives. Narratives let you connect your view of Cloudflare’s story to specific forecasts for revenue, earnings and margins, then to a fair value that you can compare with today’s price.

On Simply Wall St’s Community page, Narratives are an easy tool where you can set or adopt a fair value, link it to concrete expectations, and then see at a glance whether that view suggests Cloudflare is above or below the price you see on screen. This can help you decide whether it appears more like a buy, a hold or a sell for your portfolio.

Narratives update automatically when new earnings, news or analyst targets are added, so they stay current. You can see how different investors can look at the same company and reach very different conclusions. For example, one Cloudflare Narrative anchors on a fair value around US$132.68, another uses about US$232.78, and a more optimistic one sits at US$318, each reflecting a different story about future AI, security and margin outcomes.

For Cloudflare, however, we will make it really easy for you with previews of two leading Cloudflare narratives:

Fair value in this bullish narrative: about US$232.78 per share

At the last close of US$179.98, this narrative implies Cloudflare is roughly 22.7% below its fair value estimate.

Revenue growth assumption used: 27.62% a year

- Backers of this view focus on strong demand for cloud native security, zero trust and resilient infrastructure, along with expanding partnerships such as JD Cloud, as support for long term revenue growth and customer retention.

- They highlight improving profitability potential through operational efficiencies, cross selling and platform scale, with an updated fair value of about US$232.78 that sits close to but above the current share price and slightly below the consensus price target of US$209.01 cited in the narrative text.

- Key watchpoints include customer concentration, regulatory change, competition from hyperscalers and uncertainty around how new AI and Act 4 initiatives are monetized, which could all affect margins and the ability to support high future P/E multiples.

Fair value in this bearish narrative: about US$133.00 per share

At the last close of US$179.98, this narrative implies Cloudflare is roughly 35.3% above its fair value estimate.

Revenue growth assumption used: 26.36% a year

- This more cautious view leans on the lower end of analyst targets, with a fair value of about US$133 based on assumptions that regulatory pressure, geopolitics and higher operating costs could limit Cloudflare’s effective market size and weigh on margins over time.

- It points to competition from hyperscalers, open source tools and pricing pressure in CDN and security as risks for product differentiation and long term gross margins, even though the business is still modeled with solid top line growth.

- Supporters of this narrative see the current share price as rich relative to their assumed fair value and future P/E of 86.12x, and view any setbacks on AI workloads, security deal timing or outages as potential pressure points for the stock.

Do you think there's more to the story for Cloudflare? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NET

Cloudflare

Operates as a cloud services provider that delivers a range of services to businesses worldwide.

Exceptional growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’sMost Mispriced AI Story

Fair Value:US$7.551.2% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.9% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.9% undervalued

45 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2782.0% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

AN

AnimalDoctorKwon on Mustang Bio ·

A CAR-T Therapy Pipeline with Complete Remission (CR) Data Priced as a Negative Asset???

Fair Value:US$1.861.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GavrielH on oOh!media ·

oOh! Media Limited: Contested Takeover Creates an Asymmetric Upside

Fair Value:AU$1.923.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0336.2% undervalued

3 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.6% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.3% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17057.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative