Advertisement

- United States

- /

- IT

- /

- NYSE:IT

Is Gartner (IT) Attractive After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- If you are wondering whether Gartner's current share price still reflects the quality of the business, you are not alone. A closer look at its valuation can help frame that question more clearly.

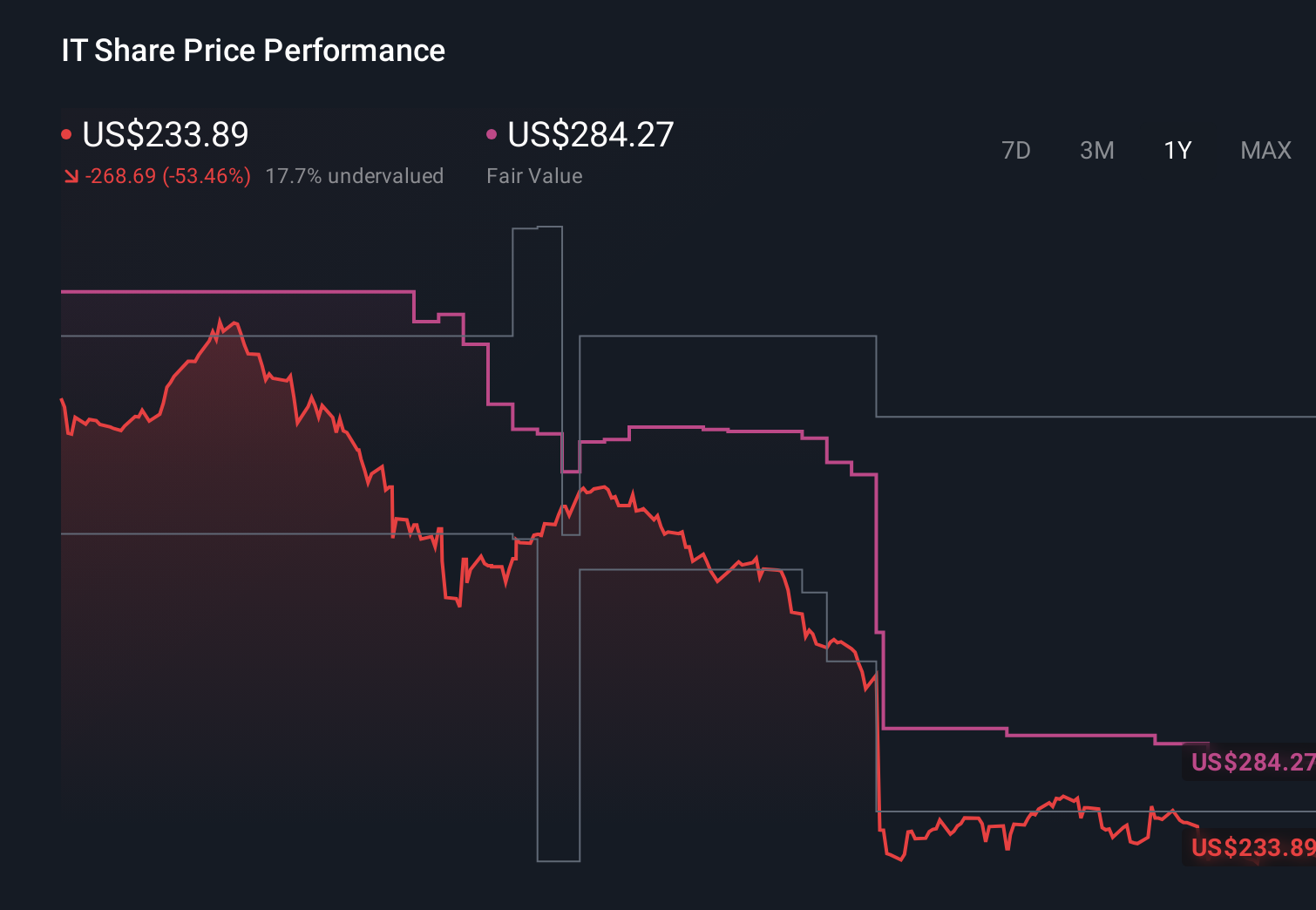

- The stock last closed at US$232.44, with returns of a 2.7% decline over 7 days, 7.2% decline over 30 days, 1.9% decline year to date, 55.7% decline over 1 year and 29.3% decline over 3 years, while the 5 year return sits at 53.3%.

- Recent coverage of Gartner has focused on its role as a key research and advisory provider for technology decision makers. This helps explain why investors keep a close eye on how the market is pricing its shares. This context is important when thinking about whether recent share price weakness reflects changing sentiment around the business or simply a reset in expectations.

- On Simply Wall St's 6 point valuation checklist, Gartner scores 4 out of 6, suggesting several checks flag the stock as potentially undervalued. Next, we will look at what different valuation methods say about that score before finishing with a way to gauge value that goes beyond the usual numbers.

Find out why Gartner's -55.7% return over the last year is lagging behind its peers.

Approach 1: Gartner Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth today by projecting its future cash flows and then discounting those back to a present value.

For Gartner, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $1.21b. Analyst estimates and Simply Wall St extrapolations project free cash flow out to 2035, with 2035 FCF forecast at about $1.71b.

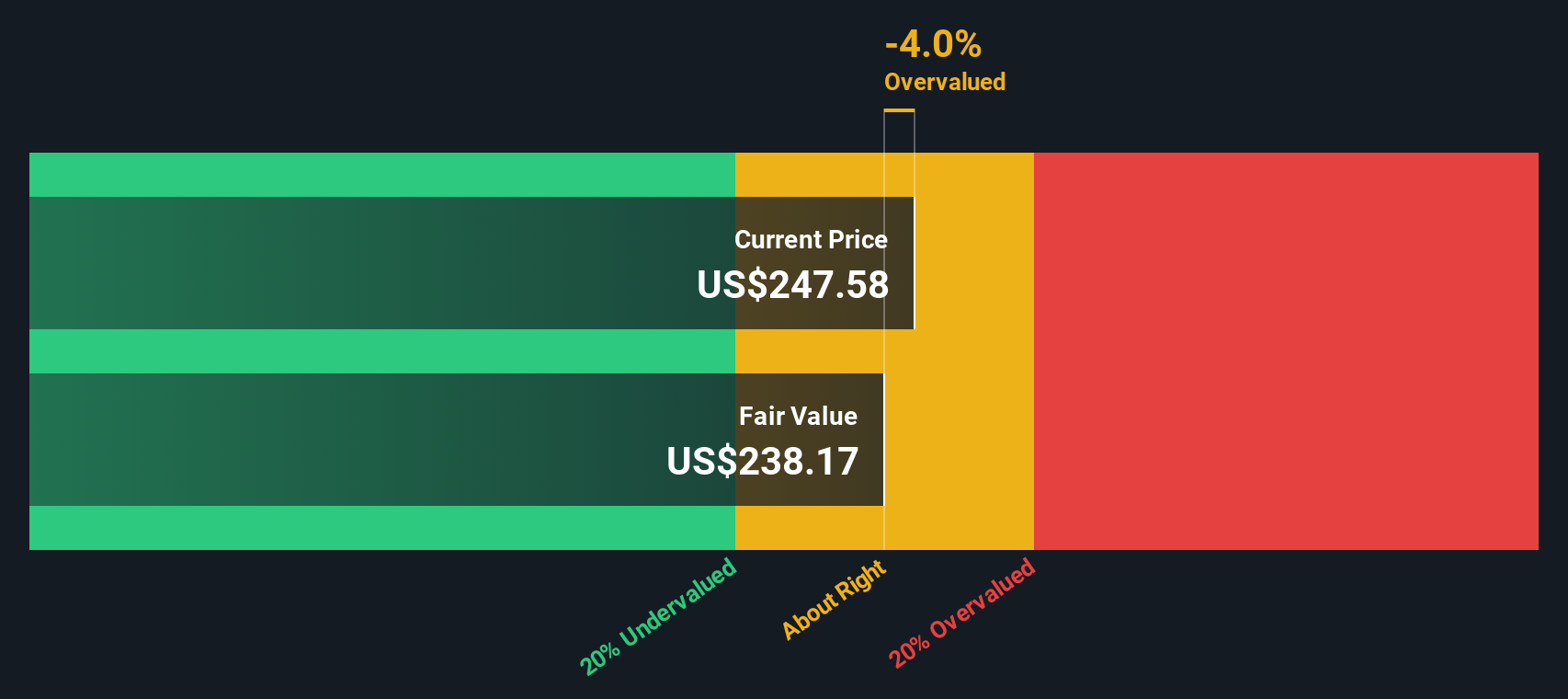

When these cash flows are discounted back to today, the model arrives at an intrinsic value of about $284.52 per share. Compared with the recent share price of $232.44, the DCF output suggests the shares trade at an 18.3% discount, which indicates the stock may be undervalued on this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Gartner is undervalued by 18.3%. Track this in your watchlist or portfolio, or discover 878 more undervalued stocks based on cash flows.

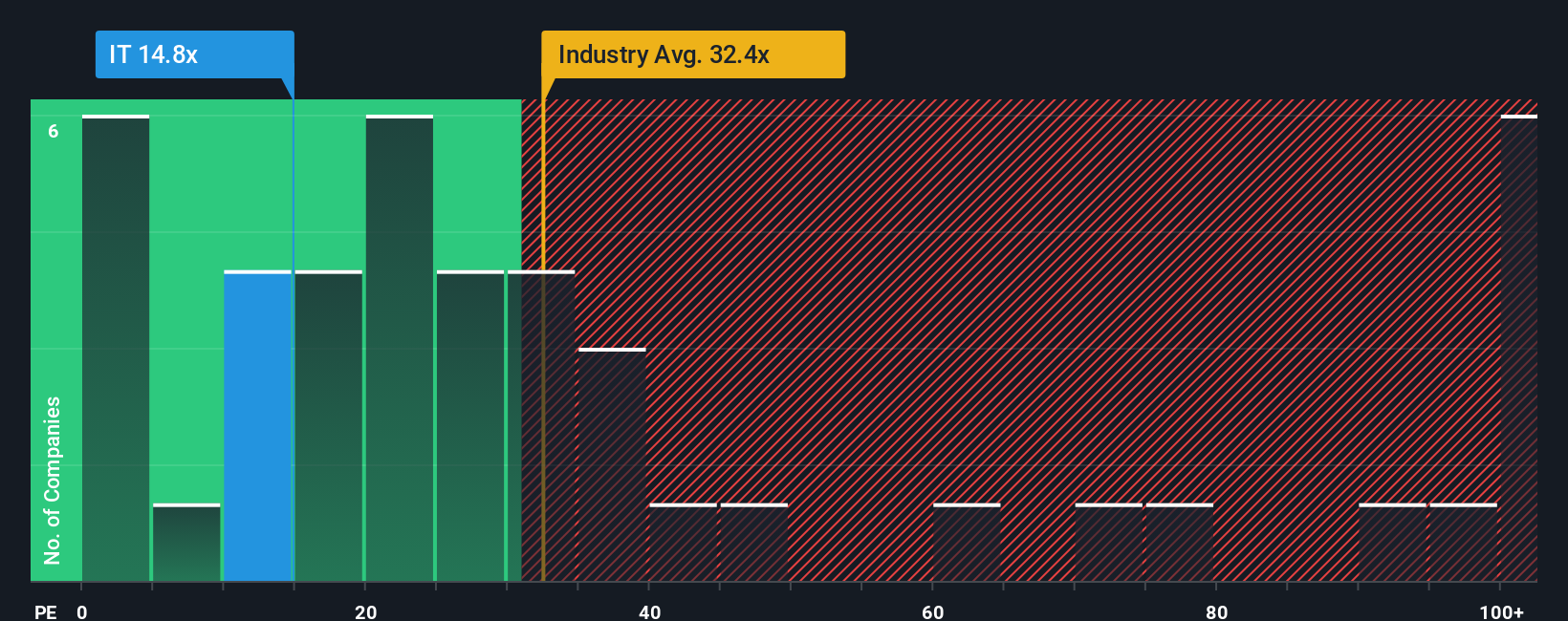

Approach 2: Gartner Price vs Earnings

For a profitable company like Gartner, the P/E ratio is a straightforward way to think about what you are paying for each dollar of earnings. Higher growth expectations and lower perceived risk usually justify a higher P/E, while slower growth or higher risk tend to point to a lower, more conservative P/E.

Gartner currently trades on a P/E of 18.92x. That sits below the broader IT industry average of 27.60x and also below the peer group average of 20.08x, which suggests the market is valuing Gartner's earnings at a lower level than many comparable names.

Simply Wall St's Fair Ratio for Gartner is 30.08x. This is a proprietary estimate of what Gartner's P/E might be given its earnings growth profile, industry, profit margins, market cap and risk characteristics. Because it blends these company specific factors, the Fair Ratio can be more tailored than a simple comparison against peers or the industry average, which do not fully reflect Gartner's own strengths and risks. Comparing Gartner's current P/E of 18.92x with the Fair Ratio of 30.08x points to the shares appearing undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Gartner Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which let you attach a clear story, along with your assumptions about Gartner's future revenue, earnings, margins and fair value, to the numbers you see on screen.

A Narrative connects three pieces you already think about: what you believe is happening at the company, how that might flow through to future financials, and what a fair value could be based on those forecasts.

On Simply Wall St's Community page, used by millions of investors, Narratives are a simple tool that helps you compare your own fair value for Gartner with the current share price, so you can decide for yourself whether it looks closer to a buy, a hold, or a potential sell.

Because Narratives are updated when new information such as news or earnings is added to the platform, your view of Gartner can adjust quickly as the facts change, and you can see at a glance how different investors, from the most optimistic to the most cautious, arrive at very different fair values for the same stock.

Do you think there's more to the story for Gartner? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IT

Gartner

Provides business and technology insights for decisions and performance on an organization’s mission-critical priorities in the United States, Canada, Europe, the Middle East, Africa, and internationally.

Good value with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

72 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

22 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on PSP Energy Berhad ·

PSP Energy Bhd Posts Strong Q3 Growth on Higher Fuel Orders

Fair Value:RM 0.237.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56031.4% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on OCI ·

OCI is not being priced on asset value. That is the opportunity.

Fair Value:€6.5643.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1188 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative