- United States

- /

- Software

- /

- NYSE:FIG

Figma (FIG): Reassessing Valuation After a Recent Share Price Rebound and Tough Year-To-Date Decline

Reviewed by Simply Wall St

Figma (FIG) shares have quietly climbed about 10% over the past month, even after sliding roughly 31% in the past 3 months and more than 65% year to date.

See our latest analysis for Figma.

The 10.46% 1 month share price return suggests sentiment is stabilizing after a brutal year to date slide, as investors reassess both Figma's growth runway and perceived execution risks.

If this rebound has you rethinking your tech exposure, it could be worth exploring other potential opportunities across high growth tech and AI stocks to see how they compare on growth and momentum.

With shares still trading well below analyst targets despite double digit revenue growth and improving earnings trends, investors now face a key question: is Figma an overlooked rebound candidate, or is the market already pricing in its next leg of growth?

Most Popular Narrative Narrative: 39.9% Undervalued

Figma's narrative fair value of about $65.70 sits well above the $39.48 last close, framing a sharp gap between story driven forecasts and current pricing.

From that strong base, Figma has started adding more products that grow naturally from Design. There’s Buzz for creating marketing assets, Make for building prototypes with AI, Sites for publishing, and Slides for presentations. Each one of these products has its own space with strong competitors: Canva for marketing design, Google Slides for presentations, Squarespace and Webflow for websites, Wix for simple builds, Lovable for prototyping. But the difference is, when you use Figma, all of these are connected. You don’t feel like you’re jumping between tools that don’t talk to each other. Instead, it feels smooth, consistent, and like it was designed to be one system.

Want to see why, according to TickerTickle, this platform sized valuation might still have room to run? The narrative leans on compounding revenue expansion, ambitious profitability uplift, and a premium future multiple usually reserved for category defining software leaders. Curious which precise growth path and margin profile power that fair value gap? Dive in to uncover the exact assumptions behind this call.

Result: Fair Value of $65.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained growth could falter if rivals rapidly narrow Figma's AI and integration lead or if valuation expectations reset sharply amid weaker sentiment.

Find out about the key risks to this Figma narrative.

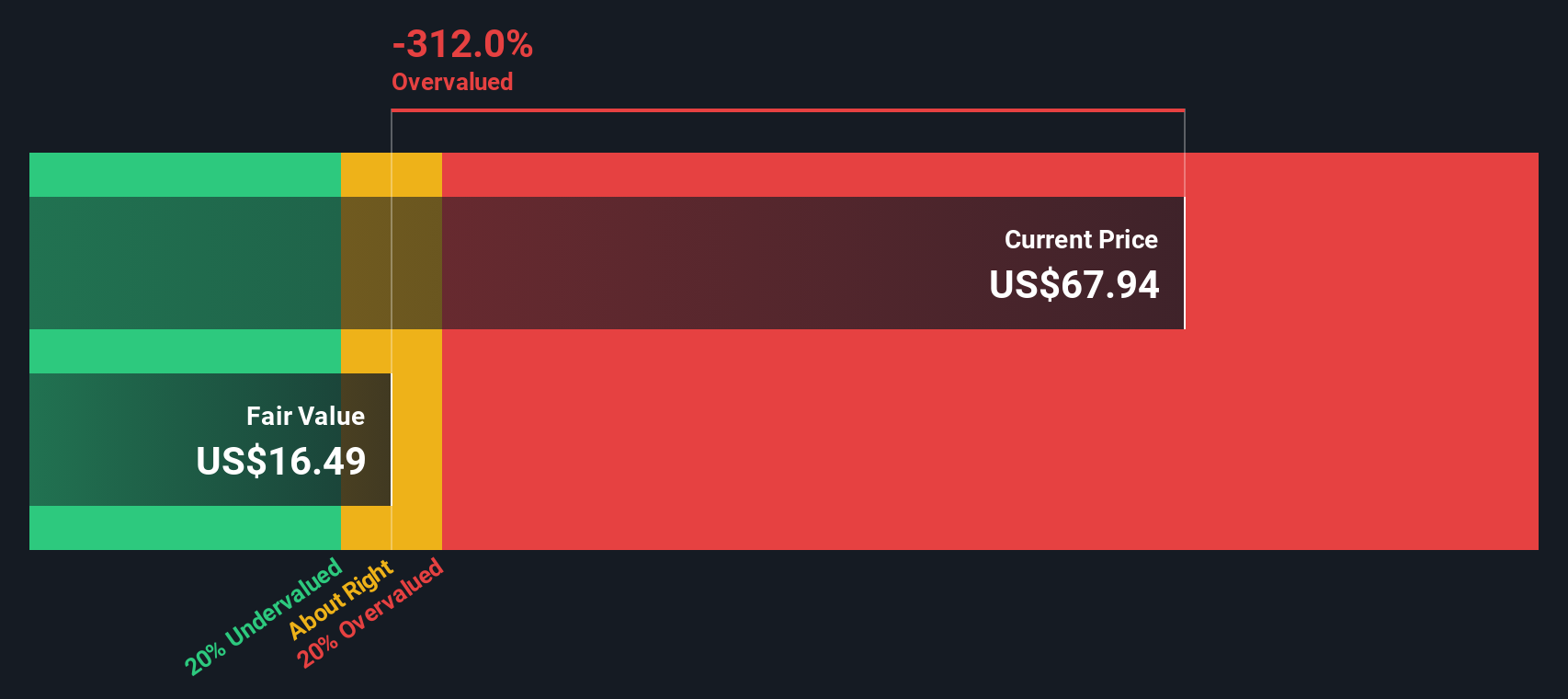

Another Lens on Value

While the narrative points to upside, our DCF model paints a tougher picture, with fair value near $19.62, implying Figma is overvalued at $39.48. Is this a case of the market looking too far ahead or the DCF not fully capturing platform optionality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Figma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Figma Narrative

If you want to stress test these assumptions or build a thesis from scratch, you can spin up a fresh narrative in under three minutes: Do it your way.

A great starting point for your Figma research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with one stock when smarter, high conviction opportunities are just a few clicks away. Put Simply Wall Street's powerful Screener to work for you today.

- Capture early stage momentum by reviewing these 3624 penny stocks with strong financials that pair tiny market caps with surprisingly resilient balance sheets and improving fundamentals.

- Tap into the next wave of automation by focusing on these 25 AI penny stocks positioned at the intersection of software, data, and scalable AI enabled business models.

- Identify dependable cash returns by screening these 13 dividend stocks with yields > 3% that balance attractive yields with sustainable payout ratios and ongoing earnings support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FIG

Figma

Develops a browser-based tool for designing user interfaces that helps design and development teams build various products.

Flawless balance sheet with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion