- United States

- /

- Software

- /

- NYSE:ESTC

Elastic (ESTC): Revisiting Valuation After Earnings Beat, Upbeat Guidance, and Positive AI Momentum

Reviewed by Simply Wall St

If you’re watching Elastic (ESTC) these days, you know the latest quarterly update has made waves with investors. The company posted stronger revenue and narrower net losses compared to last year, topping consensus expectations and signaling more than just a one-off win. Management’s upbeat guidance for both the next quarter and the full fiscal year points to double-digit growth ahead. The core message remains clear: Elastic is leaning hard into AI and data observability. As market excitement bubbled over, shares climbed in anticipation, and the upbeat sentiment increased further after a key competitor delivered impressive results of their own.

Putting this move into context, Elastic’s share price has seen its fair share of turbulence this year. The stock is still down 15% over the past year and off 11% year-to-date. Momentum, though, has shifted more recently. Shares rose nearly 7% in the lead-up to earnings and are up 9% over the past three months. These swings reflect both ongoing questions about competitive pressures and optimism that Elastic’s AI and cybersecurity push could be gaining traction with large enterprise customers.

With expectations reset and management’s outlook sounding more confident, investors may be considering whether this is a window to pick up shares at a discount, or if the market is already factoring in all the potential upside from future growth.

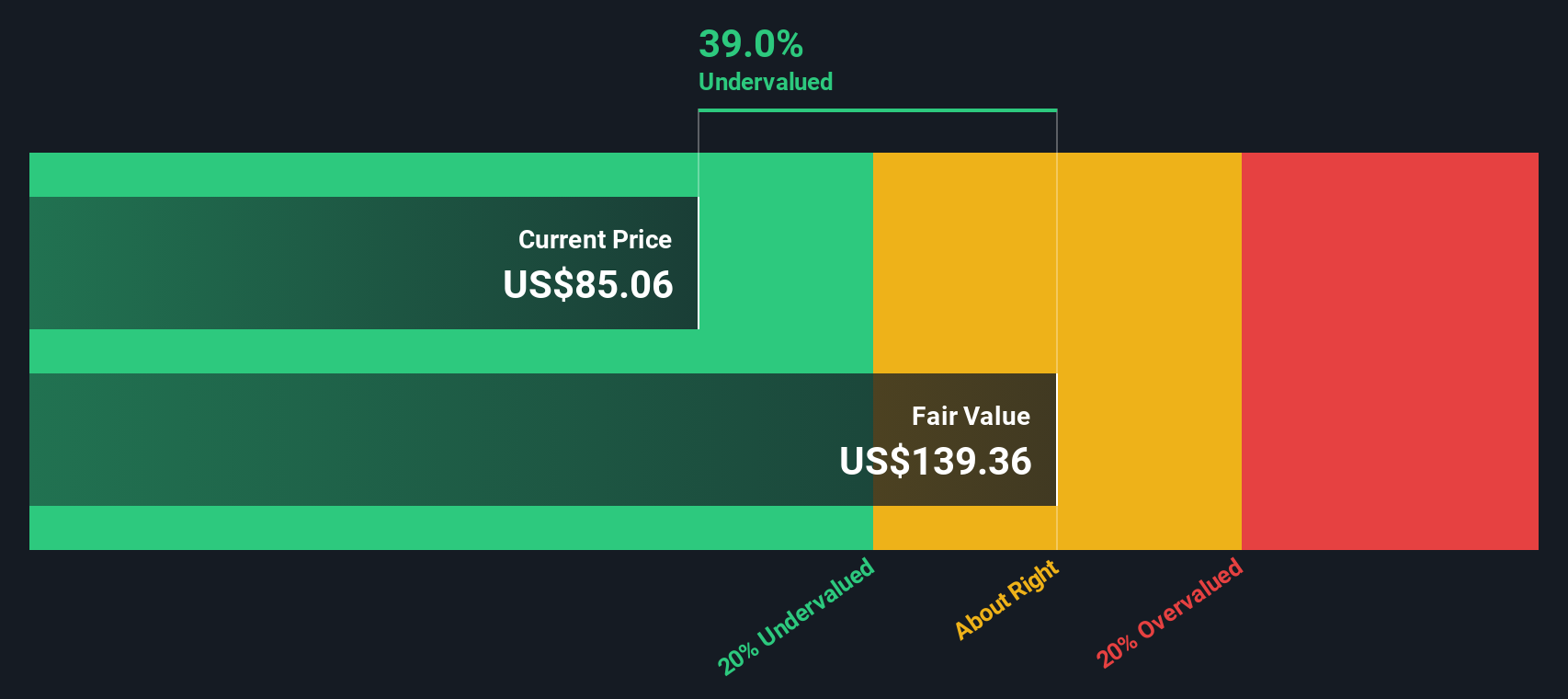

Most Popular Narrative: 19.2% Undervalued

According to the community narrative, Elastic is currently viewed as significantly undervalued by analysts, with a fair value estimate that is almost 20% higher than its recent trading levels. This assessment is based on expectations of high growth and margin improvements fueled by the company's expansion into AI and serverless technologies, discounted at a rate of 8.1%.

Elastic's focus on generative AI (GenAI) applications and enabling search innovations, such as Retrieval Augmented Generation (RAG), positions them as a key player in new AI-driven workflows. This is likely to boost future revenues as the sector grows. The company’s strategic changes in field segmentation and renewed focus on enterprise and high-potential mid-market customers have improved sales execution, indicating potential revenue and earnings growth from increased customer commitments and better sales efficiency.

Think the only story here is hype? Consider a deeper look. The positive valuation is supported by bold growth forecasts and a future profit multiple that is attracting significant attention in the tech sector. If you’re interested in the specific numbers that have analysts optimistic, and what factors could move shares beyond the current consensus, the key drivers—and the challenges that could affect this narrative—lie just beneath the surface.

Result: Fair Value of $108.65 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent sales execution hiccups or sluggish growth in the small-business segment could quickly temper optimism and challenge this undervalued outlook.

Find out about the key risks to this Elastic narrative.Another View: What Does Our DCF Model Say?

While analyst price targets suggest that Elastic is undervalued, our DCF model arrives at a similar conclusion by valuing future cash flows. However, every model has its flaws, and subtle risks could potentially tip the balance.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Elastic Narrative

If you see things differently or want to dive deeper into the details, you can easily craft your own perspective based on the latest figures. Do it your way.

A great starting point for your Elastic research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Seize the moment and don’t let unique opportunities slip by while others uncover standout investments. Take the next step with these powerful tools to find your edge in today’s markets:

- Uncover high-potential bargains by tapping into undervalued companies whose cash flow strength could lead to outsized returns with the help of undervalued stocks based on cash flows.

- Spot emerging leaders in artificial intelligence and follow groundbreaking companies shaping tomorrow’s innovations through AI penny stocks.

- Lock in reliable income for your portfolio with access to companies offering robust yields above 3 percent using dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Elastic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:ESTC

Elastic

A search artificial intelligence (AI) company, provides software platforms to run in hybrid, public or private clouds, and multi-cloud environments in the United States and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion