Advertisement

- United States

- /

- Software

- /

- NYSE:CRM

Salesforce (CRM): Assessing Valuation After Recent Pullback and Ongoing Business Momentum

Salesforce (CRM) shares have pulled back over the past month, with the stock recently closing at $228.15. While some investors may eye the double-digit dip since early spring, the company’s core business trends remain steady.

See our latest analysis for Salesforce.

Although Salesforce has slid 9.3% over the past month and is down 31% year-to-date on a share price basis, the business itself has continued pushing ahead with new partnerships and product enhancements. Momentum has clearly been fading in the short term, but over the past three years, total shareholder return has still been a solid 59%. This highlights Salesforce's long-term staying power, despite the recent reset in expectations.

If you're interested in where tech innovation might deliver the next wave of returns, it’s a smart move to check out our hand-picked list of tech and AI stocks See the full list for free.

With Salesforce trading at a notable discount to analyst price targets and showing strong revenue and net income growth, investors are left wondering if the recent dip is a genuine buying opportunity or if the market is simply pricing in future growth.

Most Popular Narrative: 15% Undervalued

According to the most widely followed narrative, Salesforce's fair value is set at $268.76, noticeably above the last close price of $228.15. This creates a narrative where strong financial performance meets market skepticism.

Salesforce (NYSE: CRM) delivered another strong quarter, proving it can grow revenue while expanding profitability, something investors have demanded for years. For Q2 fiscal 2026 (ended July 31, 2025), revenue climbed 10% year-over-year to $10.2 billion, with subscription and support revenue up 11% to $9.7 billion.

Curious how this bold price target compares? There is a key financial forecast within the narrative, pointing to expanding margins and steady revenue growth. Which critical metric could be pivotal to the story? See what drives the model behind this fair value call.

Result: Fair Value of $268.76 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, competitive pressure from rivals like Microsoft and tightening enterprise IT budgets could challenge Salesforce, affecting its continued revenue growth and margin expansion.

Find out about the key risks to this Salesforce narrative.

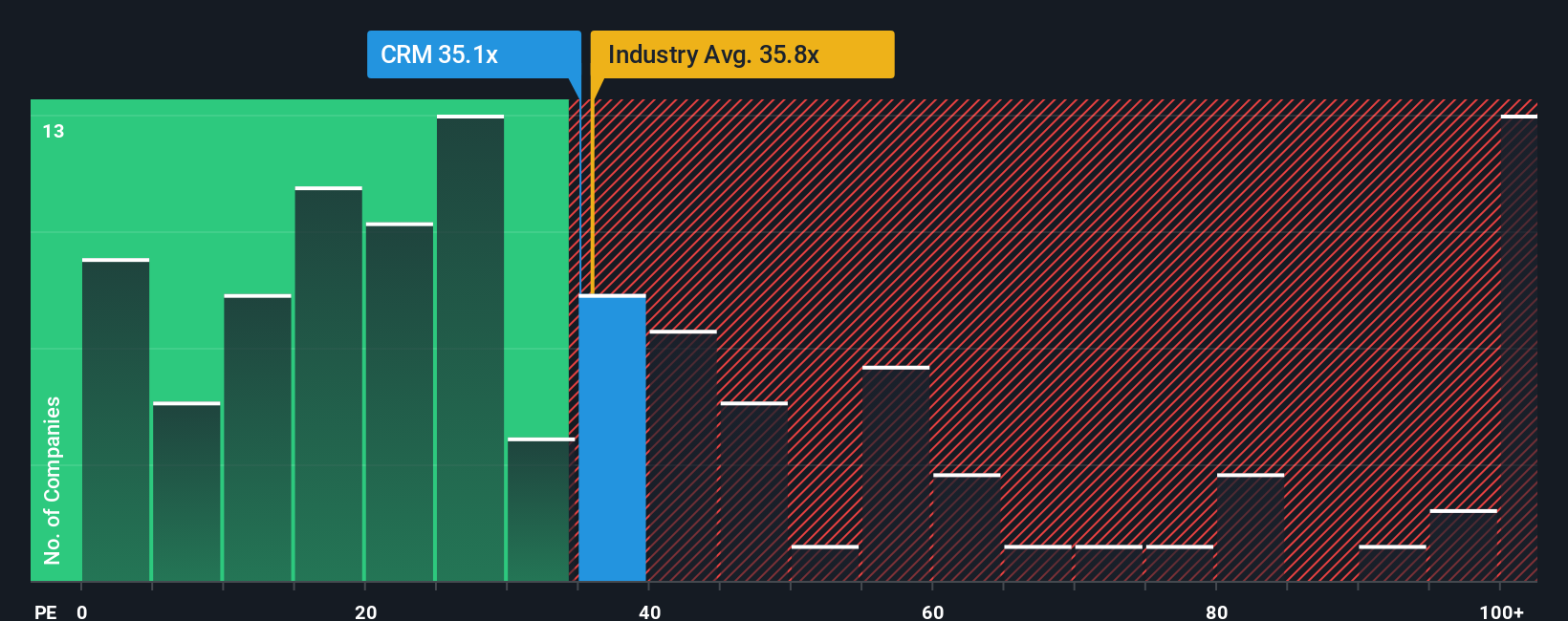

Another View: Market Ratios Send a Mixed Signal

While the narrative suggests Salesforce is undervalued, a look at its price-to-earnings ratio offers a different perspective. At 32.6x, Salesforce trades above the software industry average of 30.8x but below peers averaging 52x. This positions the stock as more expensive than most in its sector, though not the priciest among big names. The fair ratio, a market benchmark our models suggest could be an eventual target, currently sits at 43.7x. Does this gap highlight value yet to be realized, or is it a warning that the price may stall?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Salesforce Narrative

If you see the story unfolding differently, or want to dig into the numbers on your own, you can put together a narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Salesforce.

Looking for more investment ideas?

Stay ahead by moving beyond the obvious choices. If you’re after real opportunities, now is the time to see what other smart investors are searching for, before the crowd.

- Unlock growth potential by checking out these 25 AI penny stocks that are setting the pace in artificial intelligence and powering tomorrow’s digital breakthroughs.

- Find hidden value gems by reviewing these 928 undervalued stocks based on cash flows companies that financial models point to as trading below their true worth.

- Fuel your portfolio with passive income. Consider these 15 dividend stocks with yields > 3% boasting attractive yields over 3% for steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRM

Salesforce

Provides customer relationship management technology services that connect companies and customers together in the United States, Europe, and the Asia Pacific.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

54 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

22 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on NVR ·

NVR 05-2026

Fair Value:US$3.76k72.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Capricor Therapeutics ·

The Exosome Pioneer: Why Capricor (CAPR) is Poised for an August FDA Breakthrough

Fair Value:US$5862.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Rollins ·

ROL 05-2026

Fair Value:US$16.2174.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

87 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative