- United States

- /

- Software

- /

- NasdaqGS:ZS

Is Zscaler's (ZS) Deeper Peraton Tie-Up Quietly Reframing Its Zero Trust Platform Ambitions?

Reviewed by Sasha Jovanovic

- Earlier this month, Peraton announced an expanded partnership with Zscaler to combine its hybrid multicloud platform with Zscaler’s cloud-native Zero Trust Exchange, aiming to secure mission-critical government and enterprise environments while simplifying network and security architectures.

- This collaboration highlights how Zscaler’s Zero Trust and AI-driven security stack is becoming embedded in large-scale digital modernization projects across national security and defense-related operations.

- Next, we’ll examine how this deepened Peraton partnership may influence Zscaler’s investment narrative, particularly around Zero Trust adoption and platform demand.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe cloud-delivered Zero Trust and AI security will keep gaining share as organizations modernize away from legacy appliances. The expanded Peraton alliance reinforces that thesis by anchoring Zscaler inside complex, mission-critical environments, but it does not materially change the key near term catalyst, which remains broader Zero Trust platform adoption, or the biggest risk, which is intensifying competition and bundled offerings from large cloud and security vendors.

Among recent developments, Mizuho’s upgrade to “Outperform” with a US$310 price target stands out in this context, since it explicitly ties its view to Zscaler’s position in Secure Access Service Edge and Zero Trust. That aligns closely with what partnerships like Peraton, HCLTech, and T-Mobile are signaling about demand for unified cloud security, even as questions remain about competition, valuation, and the path from strong revenue growth to sustained profitability.

Yet beneath these encouraging signals, one risk investors should be aware of is how aggressively bundled security from hyperscale cloud providers could...

Read the full narrative on Zscaler (it's free!)

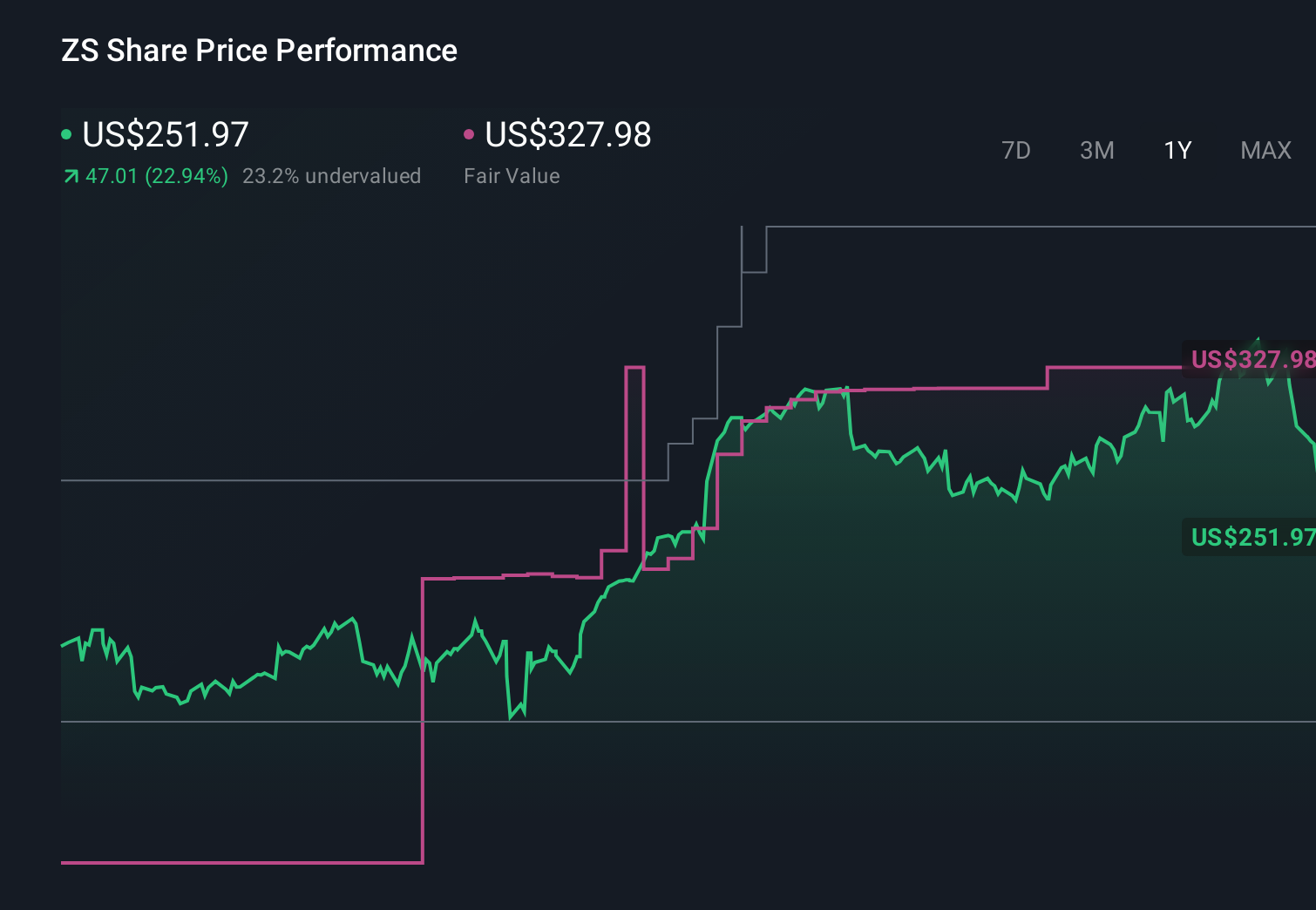

Zscaler's narrative projects $4.7 billion revenue and $139.8 million earnings by 2028.

Uncover how Zscaler's forecasts yield a $328.22 fair value, a 45% upside to its current price.

Exploring Other Perspectives

Ten fair value estimates from the Simply Wall St Community range from US$89.53 to US$328.22, underscoring how far apart investors can be. Against that wide spread, Zscaler’s growing role in Zero Trust partnerships may support the bullish camp, but you should weigh it carefully against competitive and margin risks before forming your own view.

Explore 10 other fair value estimates on Zscaler - why the stock might be worth less than half the current price!

Build Your Own Zscaler Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Zscaler research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zscaler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ZS

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion