Advertisement

- United States

- /

- Software

- /

- NasdaqGS:WDAY

Workday (WDAY): Evaluating Valuation After Paradox Acquisition Expands AI Hiring Strength

Reviewed by Kshitija Bhandaru

Workday (WDAY) completed its acquisition of Paradox, a move that expands its AI-driven hiring solutions and signals the company’s serious push into streamlined recruitment tools. Investors are already tuning in to see how this shapes earnings potential.

See our latest analysis for Workday.

With momentum around its AI hiring suite and upbeat earnings outlook, Workday has attracted renewed investor attention in recent months. Although the latest share price return has been muted, a stellar 3-year total shareholder return of nearly 60% highlights its longer-term growth story as the business expands its reach and capabilities.

If news like Workday’s latest acquisition has you looking beyond the headline, this is a great chance to discover See the full list for free.

But with shares trailing their three-year performance and analyst targets still well above current levels, investors must ask if Workday is primed for a breakout or if today’s price already reflects tomorrow’s potential.

Most Popular Narrative: 16% Undervalued

Workday’s most widely followed narrative points to a fair value of $282, comfortably above the last close price of $236.48. The stage is set for bulls as the company’s future potential is mapped out by consensus voices in the market.

Broad adoption of Workday's AI-enabled HR and finance products (with over 70% of customers using Workday Illuminate and more than 75% of net new deals including at least one AI product), along with acquisitions like Paradox and Flowise, is fueling cross-sell and upsell activity, increasing average contract values and bolstering future topline growth.

Curious about what’s driving this bold upside? The secret sauce is hidden in aggressive profit forecasts, ambitious margin boosts, and an eye-watering future earnings multiple. The underlying growth projections go far beyond the obvious. See what’s behind this confident fair value.

Result: Fair Value of $282 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, competition from established players and emerging AI-driven software firms, as well as evolving data regulations, could threaten Workday’s momentum and long-term earnings outlook.

Find out about the key risks to this Workday narrative.

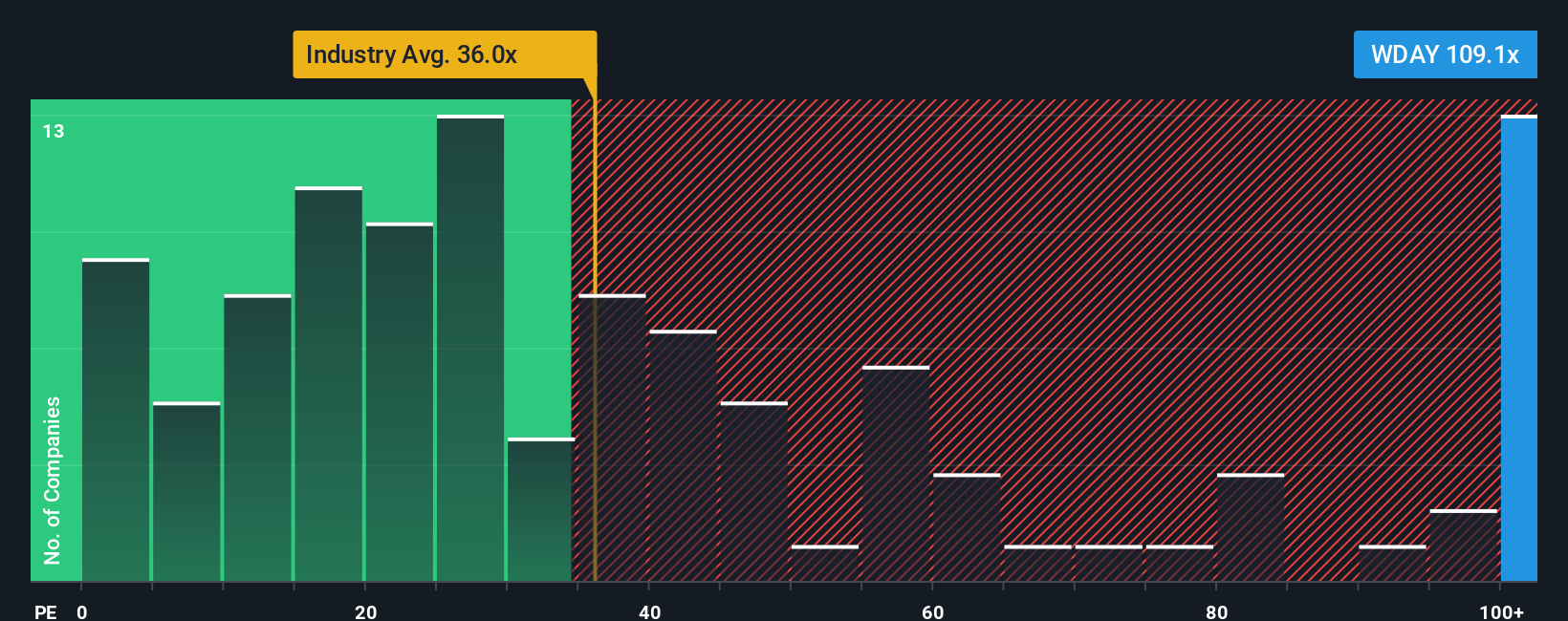

Another View: Valuation Through Multiples

While some see Workday as undervalued based on future cash flows, the main price-to-earnings ratio paints a different picture. The current P/E stands at an elevated 108.3x, far above both industry peers at 35.7x and the fair ratio of 55.3x. This signals a premium and raises questions about upside potential versus valuation risk.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Workday Narrative

If you see this differently or want to dig into the numbers yourself, you can craft your own view in just a few minutes, Do it your way

A great starting point for your Workday research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Take control of your financial future and beat the crowd by checking out other high-potential stocks using the Simply Wall Street Screener.

- Capitalize on robust cash flow opportunities by checking out these 886 undervalued stocks based on cash flows that may offer compelling value right now.

- Uncover promising healthcare breakthroughs by browsing these 32 healthcare AI stocks leading innovation with transformative AI solutions in the medical sector.

- Tap into the rise of digital wealth by reviewing these 78 cryptocurrency and blockchain stocks driving mainstream adoption of blockchain technology and cryptocurrency advancements.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Workday might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WDAY

Workday

Provides enterprise cloud applications in the United States and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.0% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.1618.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Sanyo Trading ·

Delivering steady performance

Fair Value:JP¥1.59k2.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

birdflustocks on Arcturus Therapeutics Holdings ·

Arcturus Therapeutics: Strategic opportunities beyond CSL

Fair Value:US$3076.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.1% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6118.3% undervalued

1195 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.4% undervalued

25 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative