Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Is Varonis Systems (VRNS) Fully Priced On Its Rebound Or Still A Bargain?

Varonis Systems (VRNS) is back in focus after recent trading, giving investors a fresh chance to reassess this data security software stock in light of its recent share performance and underlying financial profile.

See our latest analysis for Varonis Systems.

The recent 7.1% 1 day share price return and 13.0% 30 day share price return put Varonis Systems back on traders’ radars, although the 1 year total shareholder return declined 30.1%. This suggests that recent momentum contrasts with a weaker longer term record.

If this rebound in Varonis Systems has you rethinking your tech exposure, it may be a good time to broaden your watchlist with 35 AI small caps.

With Varonis Systems trading near its recent rebound and showing an intrinsic value estimate that is 13.0% below the current share price, investors have to ask: is there real upside left here or is the market already pricing in future growth?

Most Popular Narrative: 3.5% Undervalued

Varonis Systems is trading at $35.03 versus a narrative fair value of $36.32, so this widely followed view sees only modest upside anchored in specific growth and margin assumptions.

Continued SaaS transition and high NRR (notably for SaaS customers), combined with robust upsell momentum across cloud and multi-cloud environments, enhance ARR visibility and predictability. This is described as driving durable earnings and margin expansion as the SaaS mix climbs and operational leverage improves post-transition.

Investments in R&D and expansion of platform capabilities (for example, next-gen database security, MDDR, AI-driven integrations with Microsoft Copilot and OpenAI, cross-platform coverage for AWS, Azure, Snowflake, Databricks, and others) are said to be increasing customer wallet share and accelerating new logo acquisition, supporting consistent top-line and free cash flow growth.

Want to see what underpins that fair value for Varonis Systems? The narrative leans heavily on sustained double digit revenue growth, rising margins, and a rich future earnings multiple. Curious how those ingredients combine to justify only a small discount to today’s price? The full story connects these projections into one tight valuation case.

Result: Fair Value of $36.32 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Varonis Systems story still depends on its SaaS transition not weighing too heavily on margins, and on larger platforms not squeezing its competitive position.

Find out about the key risks to this Varonis Systems narrative.

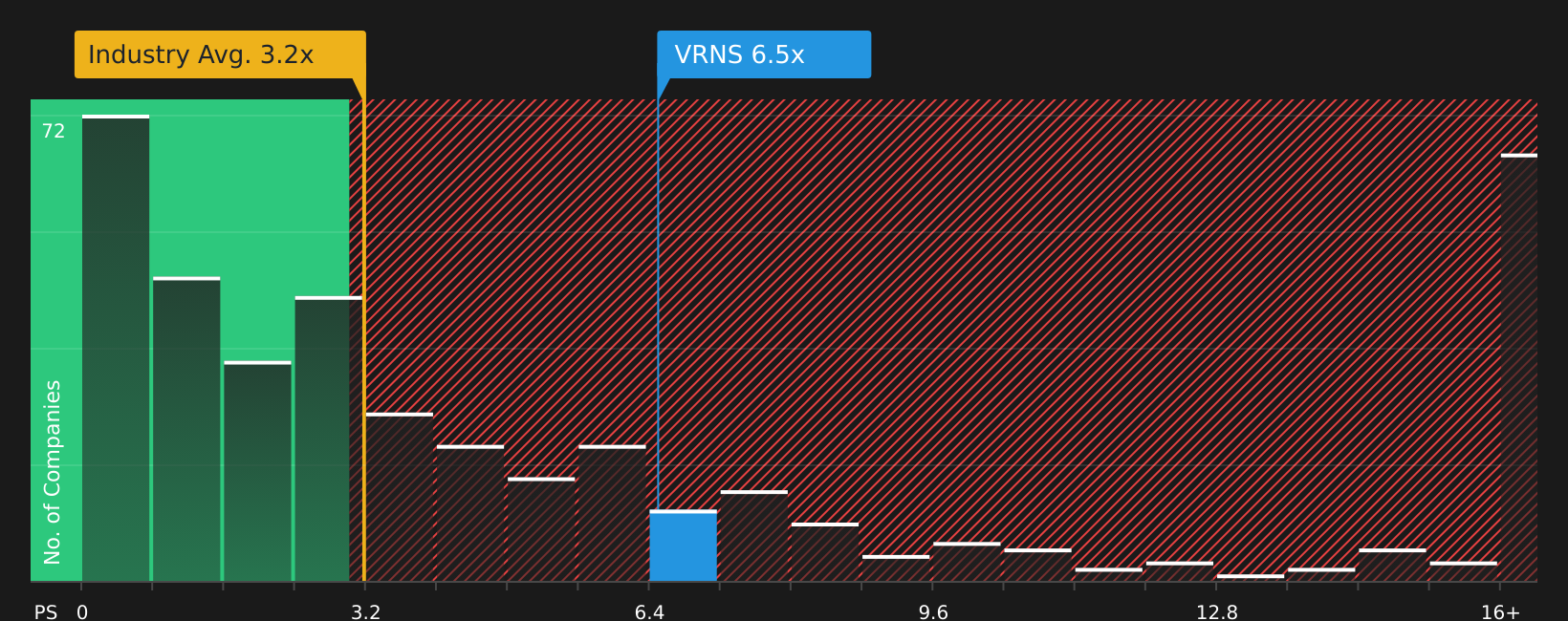

Another View: Varonis Systems Looks Expensive on Sales

While our DCF work suggests Varonis Systems is trading about 13% below an estimated future cash flow value of $40.28, the simple sales based view tells a different story. The current P/S ratio is 6.1x versus 5.3x for peers and 3.2x for the broader US software group.

Our fair ratio sits at 5.2x, which is lower than where the stock trades now. Anyone leaning on sales multiples is therefore looking at a valuation that reflects more optimism than either peers or that fair ratio imply. This raises the question of which lens you trust more when risk and return do not fully line up.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seeing both optimism and concern around Varonis Systems, it makes sense to review the underlying data yourself and decide how the risk reward trade off looks. To round out your view, take a close look at the balance of potential upside and downside flagged in our 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Varonis Systems?

If Varonis Systems has sharpened your thinking, do not stop there. The right mix of other opportunities could make a real difference to your portfolio.

- Target potential mispricings by scanning companies that combine quality with discounts using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that feature robust payouts in the 7 dividend fortresses.

- Reduce portfolio stress by focusing on resilient businesses with sturdier risk profiles through the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Excellent balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.551.2% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.9% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.9% undervalued

58 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2782.0% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

MA

Maturity_Koala_snzw on VivoPower ·

Rating: Speculative Buy

Fair Value:US$937.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Arr Planner ·

Forecasting another record year in FY1/2027

Fair Value:JP¥1.49k4.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Iino Kaiun Kaisha ·

New MTP outlines a period of transformation

Fair Value:JP¥1.22k14.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.6% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.3% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17057.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative