Advertisement

- United States

- /

- Software

- /

- NasdaqGM:VERI

Is Veritone (NASDAQ:VERI) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Veritone, Inc. (NASDAQ:VERI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Veritone

What Is Veritone's Net Debt?

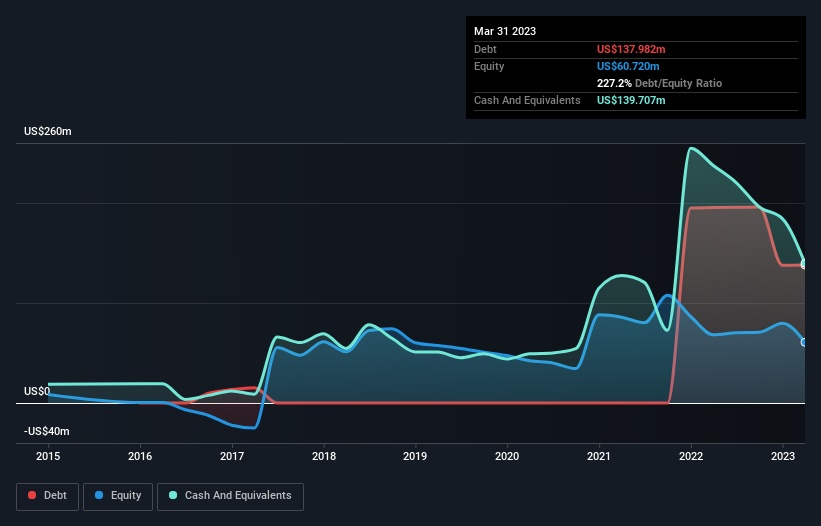

As you can see below, Veritone had US$138.0m of debt at March 2023, down from US$195.4m a year prior. But it also has US$139.7m in cash to offset that, meaning it has US$1.73m net cash.

A Look At Veritone's Liabilities

Zooming in on the latest balance sheet data, we can see that Veritone had liabilities of US$152.1m due within 12 months and liabilities of US$149.7m due beyond that. On the other hand, it had cash of US$139.7m and US$67.1m worth of receivables due within a year. So it has liabilities totalling US$95.0m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$153.9m. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. Despite its noteworthy liabilities, Veritone boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Veritone's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Veritone reported revenue of US$146m, which is a gain of 11%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Veritone?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Veritone lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$46m of cash and made a loss of US$26m. However, it has net cash of US$1.73m, so it has a bit of time before it will need more capital. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Veritone (including 1 which is significant) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:VERI

Veritone

Engages in the provision of artificial intelligence (AI) computing solutions and services in the United States, the United Kingdom, France, Australia, Israel, and India.

Good value with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.4% undervalued

292 followersusers have followed this narrative

1 commentusers have commented on this narrative

45 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

107 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.9% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KI

KiwiInvest on NVIDIA ·

NVIDIA's future hinges on $400b revenue and AI software dominance

Fair Value:US$339.935.4% undervalued

188 followersusers have followed this narrative

11 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0943.4% undervalued

28 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

KI

KiwiInvest on Xero ·

Xero will multiply its profitability with a 25% net profit margin

Fair Value:AU$133.3837.7% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

107 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.228.1% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.6% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative