Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SPLK

Strong week for Splunk (NASDAQ:SPLK) shareholders doesn't alleviate pain of three-year loss

Splunk Inc. (NASDAQ:SPLK) shareholders will doubtless be very grateful to see the share price up 49% in the last quarter. But that doesn't help the fact that the three year return is less impressive. After all, the share price is down 34% in the last three years, significantly under-performing the market.

While the stock has risen 12% in the past week but long term shareholders are still in the red, let's see what the fundamentals can tell us.

View our latest analysis for Splunk

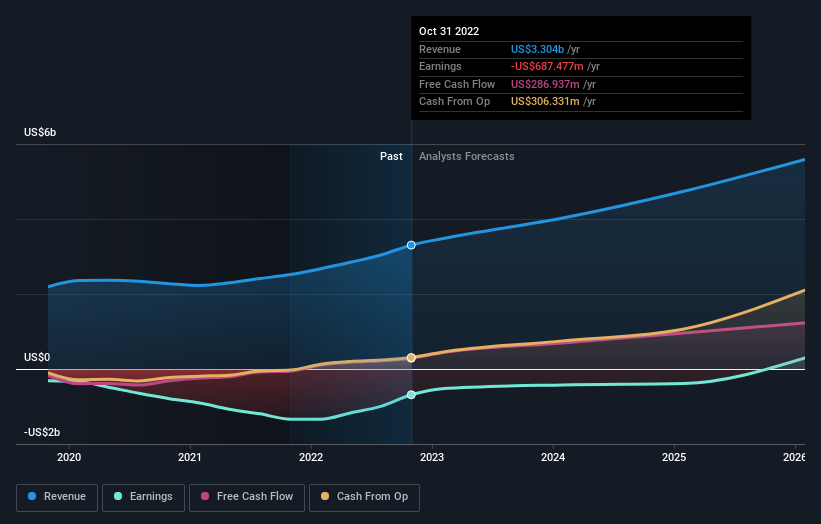

Given that Splunk didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually expect strong revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last three years, Splunk saw its revenue grow by 12% per year, compound. That's a fairly respectable growth rate. Shareholders have seen the share price fall at 10% per year, for three years. So the market has definitely lost some love for the stock. However, that's in the past now, and it's the future is more important - and the future looks brighter (based on revenue, anyway).

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Splunk is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. Given we have quite a good number of analyst forecasts, it might be well worth checking out this free chart depicting consensus estimates.

A Different Perspective

We regret to report that Splunk shareholders are down 9.2% for the year. Unfortunately, that's worse than the broader market decline of 7.0%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Longer term investors wouldn't be so upset, since they would have made 4%, each year, over five years. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. For instance, we've identified 2 warning signs for Splunk that you should be aware of.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SPLK

Splunk

Splunk Inc., together with its subsidiaries, develops and markets cloud services and licensed software solutions in the United States and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WA

wahyud on Perusahaan Perkebunan London Sumatra Indonesia ·

LSIP Revenue to Rise a Whopping 43.92% Amid Market Dynamics

Fair Value:Rp3.6k63.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Charoen Pokphand Indonesia ·

Charoen Pokphand Indonesia will soar with a 12.94% growth and a 10.67x future P/E

Fair Value:Rp4.53k4.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Medco Energi Internasional ·

Medco Energi's Revenue Will Increase by 2.45% Doors Opening

Fair Value:Rp1.75k23.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative