Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SNPS

Synopsys (SNPS) Stock Could Trade Below Fair Value Despite Rich Earnings

Reviewed by Bailey Pemberton

Synopsys stock has pulled back over the past year, yet there is a clear split on value, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to meaningful upside while market multiples suggest the shares are on the expensive side.

- Over 5 years, Synopsys has delivered a gain of 48.1%, which puts the recent weakness into a longer track record of positive returns.

- The shift away from legacy manufacturing analytics toward AI driven chip design tools may support future cash flow, but the execution risk around product transitions and new licensing models could weigh on how much investors are willing to pay for that story.

- On Simply Wall St's broader checks, Synopsys screens cheap on only 2 of 6 valuation tests, which leans more toward a rich pricing than a clear bargain.

The issue now is whether you treat Synopsys as undervalued based on its intrinsic value estimate or as a fully priced stock based on current market multiples.

Find out why Synopsys' -29.2% return over the last year is lagging behind its peers.

Does Synopsys Look Undervalued on Cash Flow?

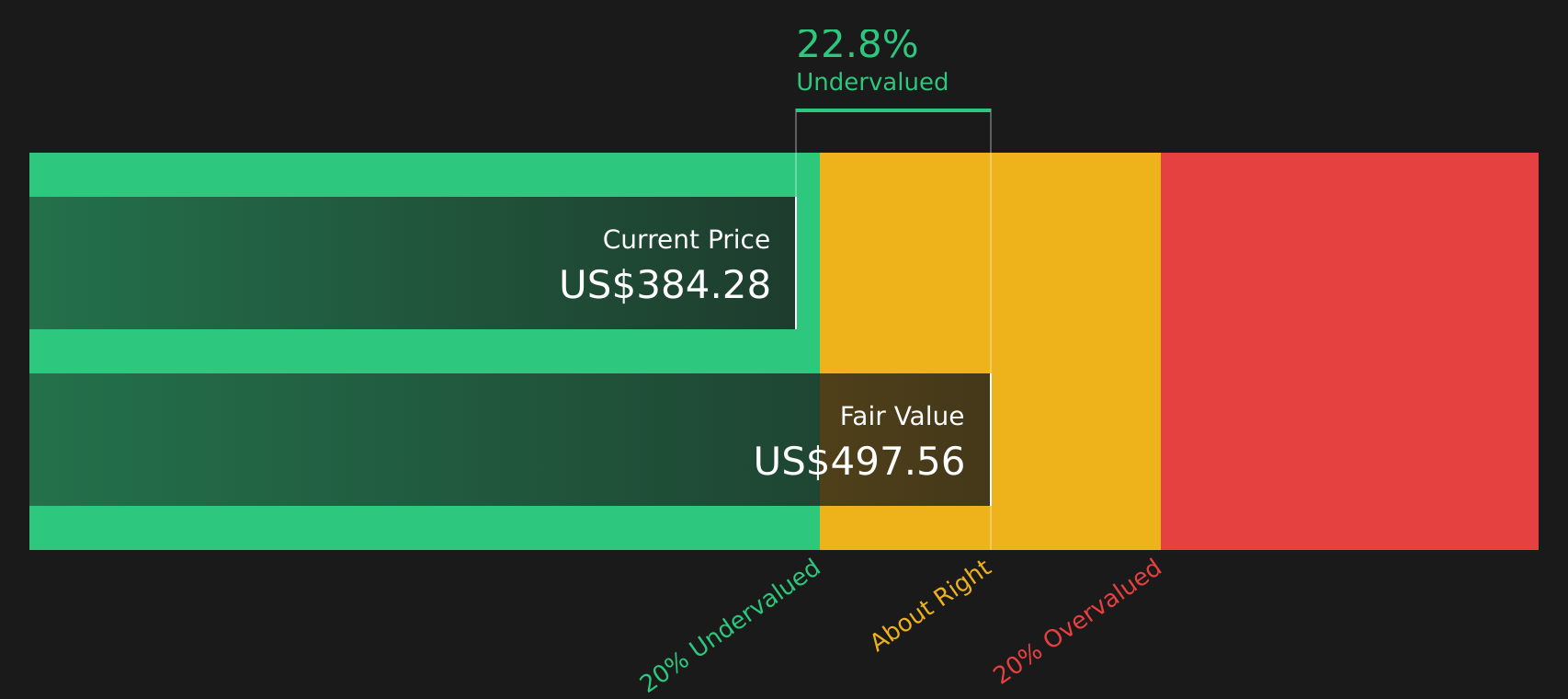

The Discounted Cash Flow (DCF) approach estimates what Synopsys is worth based on projected future cash generation, adjusted back to today. For Synopsys, the latest twelve month free cash flow sits at about $2.6b, and the 2 Stage Free Cash Flow to Equity model assumes that cash flow continues growing rather than shrinking, then tapers to a steadier pace over time.

On those assumptions, the DCF model points to an intrinsic value of about $496 per share, which sits above the current share price and implies the stock is 15.9% undervalued. Because Synopsys is reallocating capital into higher margin, AI driven chip design tools and new licensing structures, the market may be cautious about how smooth that transition will be. This can be the case even if the cash flow profile in the model looks supportive.

On the cash flow numbers used here, Synopsys stock screens as undervalued relative to its DCF based intrinsic value estimate.

Our Discounted Cash Flow (DCF) analysis suggests Synopsys is undervalued by 15.9%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Does Synopsys Look Pricey on Earnings?

P/E is a useful yardstick for Synopsys because earnings remain the main anchor for how investors value established software companies. On this measure, Synopsys trades on a P/E of about 103.3x, which is well above the wider software industry average of roughly 28.8x and a peer group average closer to 33.5x.

The fair P/E ratio, which blends factors such as growth profile, margins, size and risk, is estimated at about 49.0x. That is still well below where Synopsys currently trades, so the stock sits at a marked premium even relative to a tailored benchmark rather than just a sector average. This indicates that the market is already pricing in a strong narrative around AI driven chip design tools and licensing changes, with limited room in this framework for additional optimism without a higher earnings base.

On the P/E multiple, Synopsys stock currently screens as overvalued.

See what the numbers say about this price — find out in our valuation breakdown.

The Synopsys Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Synopsys are designed to connect that split between DCF and earnings multiples by spelling out which paths for Synopsys' growth, margins and earnings would need to hold for the stock to justify a higher or lower price than today. They sit on the company’s Community page, and each one treats its fair value as a clear, testable view on how the business might develop over time, so you can track how that view holds up.

If you have a number driven view on whether Synopsys' push into AI focused chip design tools and new licensing models pays off, share a Narrative in the Simply Wall St community and spell out the case you want to track as results come through. Adding your voice now lets you set a clear yardstick for how Synopsys' story and valuation line up over time.

Do you think there's more to the story for Synopsys? Head over to our Community to see what others are saying!

The Bottom Line

For Synopsys, the Discounted Cash Flow (DCF) intrinsic value suggests some upside, while the P/E based view flags the stock as overvalued relative to peers and a tailored fair ratio. That tension, combined with weaker results from broader valuation checks, means investors are weighing a supportive cash flow profile against already full expectations in the market multiples. The key question is whether Synopsys can execute smoothly on its shift toward AI focused chip design tools and new licensing models. If that transition delivers the earnings base implied by the current P/E, today’s premium may look justified; otherwise it risks proving too rich.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SNPS

Synopsys

Provides design IP solutions in the semiconductor and electronics industries.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1944.7% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

58 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.9% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.0% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RI

Ricktorious on IREN ·

IREN: AI Infrastructure Growth vs. Valuation Risk

Fair Value:US$120.0771.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4851.3% undervalued

200 followersusers have followed this narrative

16 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RD

rdiab on Fortinet ·

FTNT Is The Cybersecurity Powerhouse A Buy?

Fair Value:US$125.5628.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75026.5% undervalued

94 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5456.6% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

58 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0