Advertisement

- United States

- /

- IT

- /

- NasdaqGS:RXT

Assessing Rackspace Technology (RXT) Valuation After Its Return To Quarterly Profit

Rackspace Technology earnings spark fresh interest in the stock

Rackspace Technology (RXT) has drawn renewed attention after reporting first quarter 2026 earnings, shifting from a net loss a year ago to net income of US$8.3 million on sales of US$678.1 million.

See our latest analysis for Rackspace Technology.

The strong first quarter result has come alongside very sharp share price swings, with a 30 day share price return of 139.35% and a very large 90 day gain. However, a 5 year total shareholder return of 87.58% in the red suggests the longer term picture remains challenging.

If Rackspace Technology’s rebound has caught your eye, it can also be useful to see what else is moving in related areas, such as 38 AI infrastructure stocks

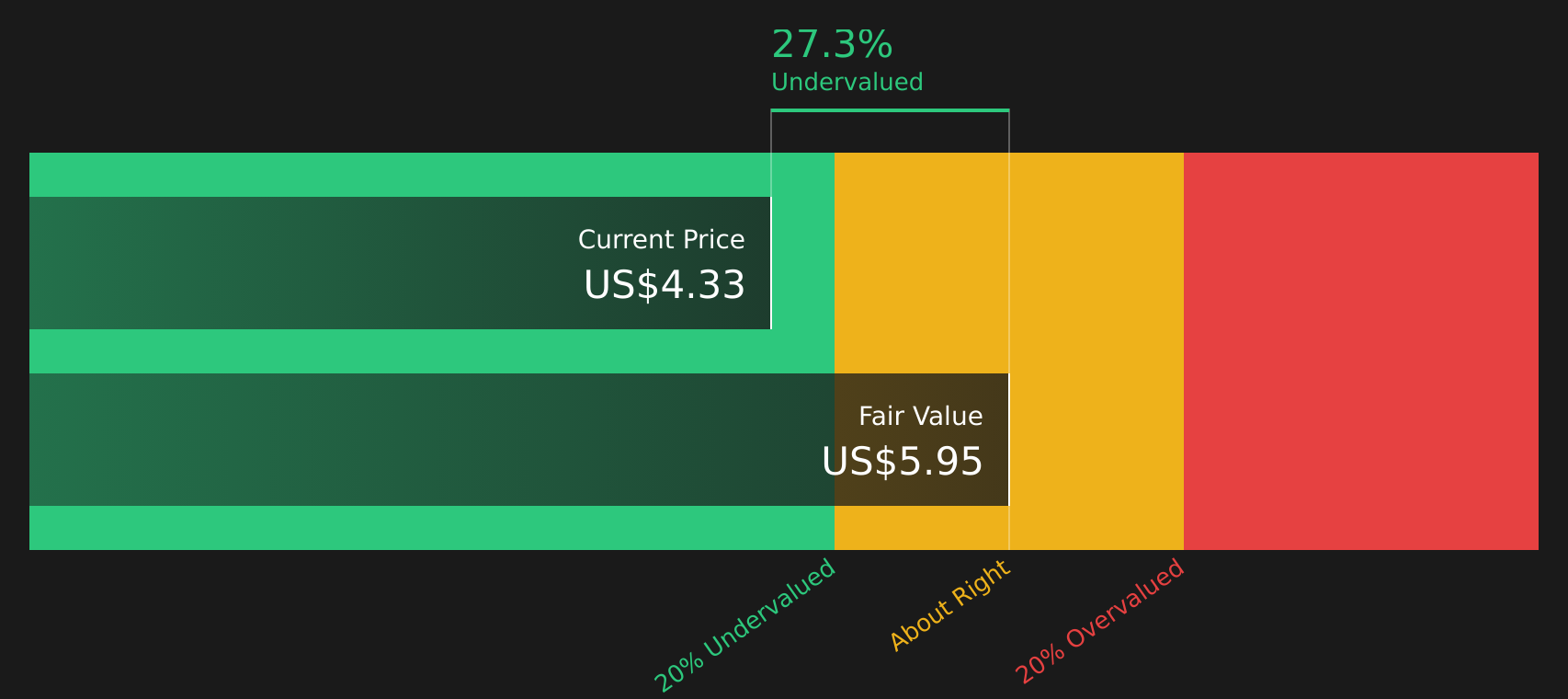

With Rackspace now reporting quarterly profit and trading at a 47% discount to one estimate of intrinsic value, your key question is simple: is this a genuine mispricing or is the market already banking on future growth?

Most Popular Narrative: 5% Overvalued

Rackspace Technology’s most followed narrative points to a fair value of about $2.17 per share, slightly above the last close of $2.27. This puts more focus on the assumptions behind that number.

Ongoing digital transformation and increasing complexity of hybrid/multi-cloud environments are driving strong demand for Rackspace's managed cloud services, as evidenced by double-digit year-over-year bookings growth and a shift toward larger, longer-term enterprise contracts. This is likely to support a sustained rebound in revenue and enhance revenue visibility.

Curious what turns that bookings strength into a higher fair value? The narrative leans heavily on modest revenue growth, firmer margins and a future earnings multiple that sits well below many US IT peers.

Result: Fair Value of $2.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear pressure points, including year over year revenue declines in both cloud segments, as well as ongoing margin and cash flow strains that could easily challenge this rebound story.

Find out about the key risks to this Rackspace Technology narrative.

Another Angle on Value

The popular narrative says Rackspace Technology looks about 5% overvalued at $2.27 based on future earnings assumptions, yet our DCF model points the other way, with a fair value estimate of $4.32 that implies the stock trades at a wide discount. Which story do you think holds up better under your own assumptions?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With the story still finely balanced between rebound potential and real risks, now is the time to look through the details yourself and decide where you stand. You can start with the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Rackspace has sharpened your focus, do not stop here. Use curated stock lists to spot other opportunities that match how you like to invest.

- Capture potential mispricings by checking out 44 high quality undervalued stocks before other investors focus on them.

- Prioritise resilience by scanning 74 resilient stocks with low risk scores so you are not caught off guard by hidden vulnerabilities.

- Hunt for future standouts early by reviewing the screener containing 23 high quality undiscovered gems while they are still off most investors’ radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:RXT

Rackspace Technology

Operates as a hybrid cloud and artificial intelligence solutions company in the United States, the United Kingdom, and internationally.

Slight risk and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5360.2% undervalued

137 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.4% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.313.7% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2451.0% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

YA

Yaser on Jarir Marketing ·

Future P/E of 15.5x Reflects Jarir's Balanced Growth Expectations

Fair Value:ر.س15.040.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$20.0468.0% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Paradigm Biopharmaceuticals ·

I am a shareholder and my investment thesis is maintained

Fair Value:AU$183.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.9% undervalued

110 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74016.4% undervalued

37 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6112.2% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative