Advertisement

- United States

- /

- Software

- /

- NasdaqCM:NTWK

NetSol Technologies (NASDAQ:NTWK) Could Easily Take On More Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies NetSol Technologies, Inc. (NASDAQ:NTWK) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for NetSol Technologies

How Much Debt Does NetSol Technologies Carry?

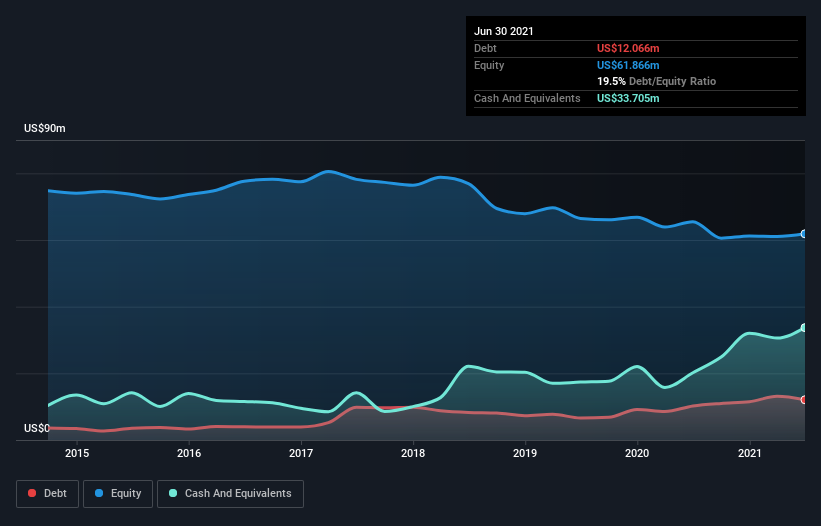

As you can see below, at the end of June 2021, NetSol Technologies had US$12.1m of debt, up from US$10.2m a year ago. Click the image for more detail. However, it does have US$33.7m in cash offsetting this, leading to net cash of US$21.6m.

A Look At NetSol Technologies' Liabilities

The latest balance sheet data shows that NetSol Technologies had liabilities of US$23.5m due within a year, and liabilities of US$1.26m falling due after that. Offsetting this, it had US$33.7m in cash and US$18.5m in receivables that were due within 12 months. So it can boast US$27.5m more liquid assets than total liabilities.

This surplus liquidity suggests that NetSol Technologies' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, NetSol Technologies boasts net cash, so it's fair to say it does not have a heavy debt load!

Even more impressive was the fact that NetSol Technologies grew its EBIT by 154% over twelve months. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is NetSol Technologies's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. NetSol Technologies may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, NetSol Technologies actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While it is always sensible to investigate a company's debt, in this case NetSol Technologies has US$21.6m in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of US$13m, being 170% of its EBIT. The bottom line is that NetSol Technologies's use of debt is absolutely fine. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with NetSol Technologies .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if NetSol Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:NTWK

NetSol Technologies

Engages in the design, development, marketing, and export of enterprise software solutions to the automobile financing and leasing, banking, and financial services industries in North America, Europe, and Asia Pacific.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.9% undervalued

147 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0327.9% undervalued

32 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.3% undervalued

42 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.8% undervalued

16 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.9% undervalued

264 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.0% overvalued

129 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.7% undervalued

160 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0