Advertisement

- United States

- /

- Software

- /

- NasdaqGS:MAPS

Results: WM Technology, Inc. Confounded Analyst Expectations With A Surprise Profit

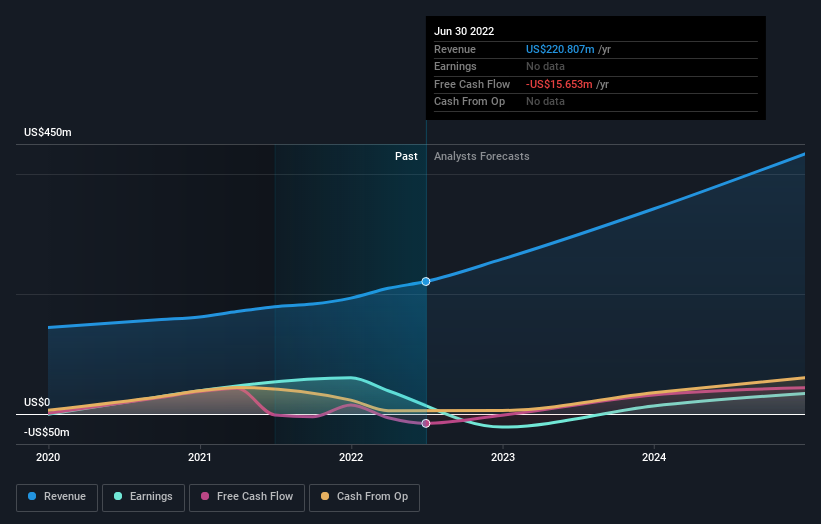

Shareholders in WM Technology, Inc. (NASDAQ:MAPS) had a terrible week, as shares crashed 29% to US$2.59 in the week since its latest second-quarter results. Revenues of US$58m reported a marginal miss, falling short of forecasts by 6.0%, but earnings were better than expected - statutory profits came in at US$0.13 per share, a nice change from the loss the analysts expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for WM Technology

Following the latest results, WM Technology's six analysts are now forecasting revenues of US$258.1m in 2022. This would be a notable 17% improvement in sales compared to the last 12 months. The company is forecast to report a statutory loss of US$0.22 in 2022, a sharp decline from a profit over the last year. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$260.4m and losses of US$0.20 per share in 2022. So it's pretty clear consensus is mixed on WM Technology after the new consensus numbers; while the analysts held their revenue numbers steady, they also administered a pronounced increase to per-share loss expectations.

The consensus price target fell 44% to US$5.04per share, with the analysts clearly concerned by ballooning losses. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on WM Technology, with the most bullish analyst valuing it at US$10.50 and the most bearish at US$7.00 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that WM Technology's rate of growth is expected to accelerate meaningfully, with the forecast 37% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 23% over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 13% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that WM Technology is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for WM Technology going out to 2024, and you can see them free on our platform here..

It is also worth noting that we have found 2 warning signs for WM Technology that you need to take into consideration.

Valuation is complex, but we're here to simplify it.

Discover if WM Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:MAPS

WM Technology

An online cannabis marketplace, provides ecommerce and compliance software solutions to retailers and brands in cannabis market in the United States and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.671.8% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.234.8% undervalued

43 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2685.8% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3412.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AV

avt on TROPHY GAMES Development ·

TROPHY GAMES Development Will See Revenue Rise by 22% in the Next 3 Years

Fair Value:DKK 21.0133.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.234.8% undervalued

43 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.593.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3954.1% overvalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3130.0% undervalued

1362 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.2k% overvalued

38 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative