- United States

- /

- IT

- /

- NasdaqGS:KC

Kingsoft Cloud Holdings (NASDAQ:KC) one-year losses have grown faster than shareholder returns have fallen, but the stock swells 12% this past week

Kingsoft Cloud Holdings Limited (NASDAQ:KC) shareholders will doubtless be very grateful to see the share price up 38% in the last quarter. But that is minimal compensation for the share price under-performance over the last year. In fact, the price has declined 15% in a year, falling short of the returns you could get by investing in an index fund.

The recent uptick of 12% could be a positive sign of things to come, so let's take a look at historical fundamentals.

Check out our latest analysis for Kingsoft Cloud Holdings

Kingsoft Cloud Holdings isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually expect strong revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

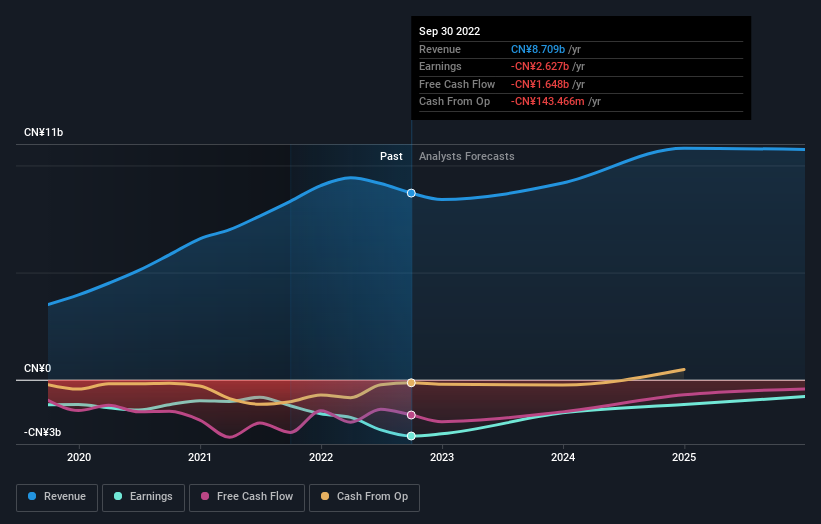

Kingsoft Cloud Holdings grew its revenue by 4.6% over the last year. That's not a very high growth rate considering it doesn't make profits. Given this lacklustre revenue growth, the share price drop of 15% seems pretty appropriate. It's important not to lose sight of the fact that profitless companies must grow. So remember, if you buy a profitless company then you risk being a profitless investor.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Kingsoft Cloud Holdings is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. Given we have quite a good number of analyst forecasts, it might be well worth checking out this free chart depicting consensus estimates.

A Different Perspective

We doubt Kingsoft Cloud Holdings shareholders are happy with the loss of 15% over twelve months. That falls short of the market, which lost 12%. That's disappointing, but it's worth keeping in mind that the market-wide selling wouldn't have helped. Putting aside the last twelve months, it's good to see the share price has rebounded by 38%, in the last ninety days. Let's just hope this isn't the widely-feared 'dead cat bounce' (which would indicate further declines to come). It's always interesting to track share price performance over the longer term. But to understand Kingsoft Cloud Holdings better, we need to consider many other factors. Even so, be aware that Kingsoft Cloud Holdings is showing 2 warning signs in our investment analysis , you should know about...

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Kingsoft Cloud Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:KC

Kingsoft Cloud Holdings

Provides cloud services to businesses and organizations primarily in China.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Community Narratives