- United States

- /

- Software

- /

- NasdaqGS:IREN

Is Analyst Uncertainty Around High-Performance Computing Deals Shifting the Investment Narrative for IREN (IREN)?

Reviewed by Simply Wall St

- JPMorgan recently shifted its rating on IREN from "Overweight" to "Neutral," citing uncertainty about the timing of a potential high-performance computing deal as a key reason.

- Despite some caution, analysts pointed to long-term growth prospects tied to IREN's ability to participate in emerging digital infrastructure trends.

- Now, we'll consider how analyst attention on potential high-performance computing growth could shape IREN's forward-looking investment case.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

IREN Investment Narrative Recap

For anyone considering IREN as a long-term holding, the key belief centers on its transition from cryptocurrency mining to a broader role in digital infrastructure and AI-driven data center services. JPMorgan’s recent downgrade, tied to uncertainty around a major high-performance computing contract, does not appear to materially shift the short-term catalyst: successfully converting infrastructure and capital allocation into revenue from AI and cloud opportunities. The biggest risk remains IREN's ongoing reliance on volatile mining revenues until this pivot fully materializes.

Most recently, the company's move to appoint J.P. Morgan Securities and Citigroup as co-lead underwriters for a US$500 million fixed-income offering stands out. This aligns with the near-term need to secure funding for large-scale infrastructure projects like Sweetwater and Childress, which are core to realizing AI and high-performance computing ambitions highlighted in current analyst attention. This financing news is directly relevant to both the company's biggest risk and catalyst, underlining that execution and funding go hand in hand for IREN’s future.

However, even with fresh analyst attention on new business lines, investors should be mindful that the company’s heavy dependence on volatile mining revenues could still...

Read the full narrative on IREN (it's free!)

IREN's outlook anticipates $1.4 billion in revenue and $547.2 million in earnings by 2028. This scenario requires annual revenue growth of 55.2% and an earnings increase of $582.9 million from the current level of -$35.7 million.

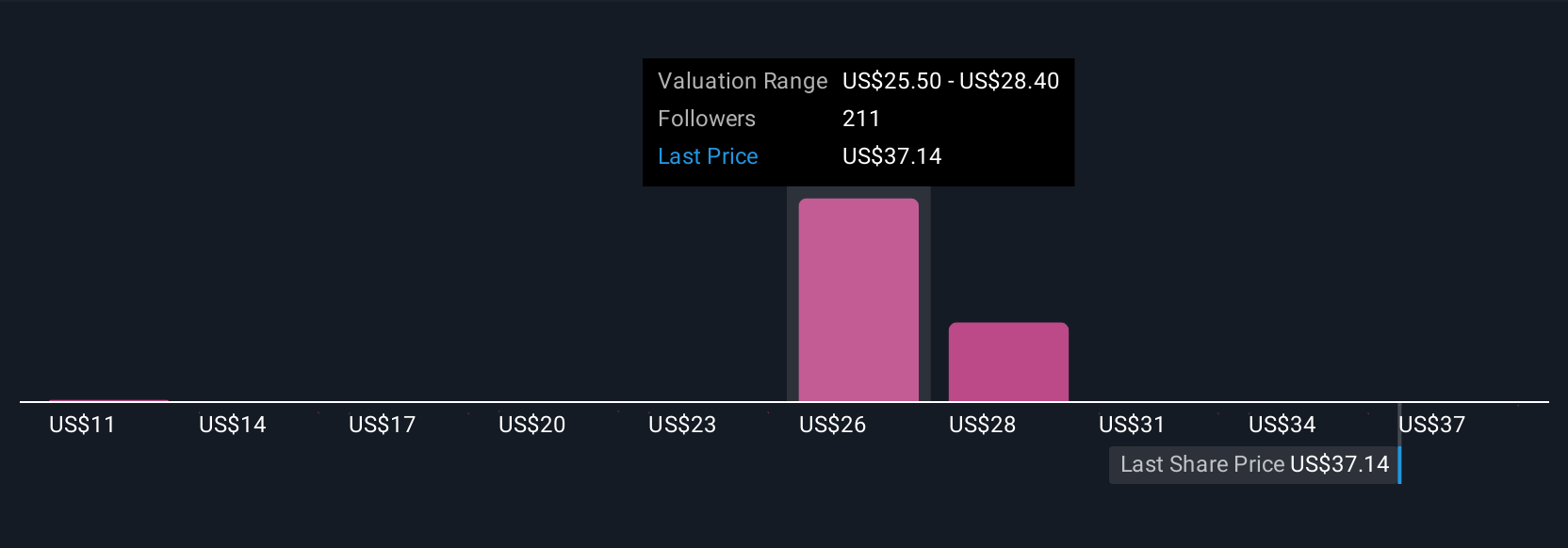

Uncover how IREN's forecasts yield a $22.00 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members posted 12 fair value estimates for IREN, spanning from US$11.00 to US$26.54 per share. Your view may differ widely, especially with upcoming funding decisions shaping the company’s progress in AI infrastructure, consider how these opposing perspectives might affect your outlook.

Explore 12 other fair value estimates on IREN - why the stock might be worth 33% less than the current price!

Build Your Own IREN Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your IREN research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free IREN research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IREN's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 25 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IREN

IREN

Operates in the vertically integrated data center business in Australia and Canada.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion