Advertisement

- United States

- /

- Software

- /

- NasdaqGS:INTU

Is Intuit (INTU) Attractive After Recent Share Price Pullback And AI Partnership Hopes

Reviewed by Bailey Pemberton

- If you are wondering whether Intuit's current share price lines up with its underlying value, you are not alone. This article is built to help you weigh what you are really paying for.

- Intuit's share price closed at US$554.58, with returns of a 15% decline over the past 7 days, a 17.1% decline over 30 days and an 11.9% decline year to date, while the 1 year return sits at an 8.1% decline and the 3 and 5 year returns are 49.4% and 49.9% respectively.

- Recent moves in the stock sit against an ongoing flow of product updates and ecosystem expansions across its platforms. This keeps attention on how much investors are willing to pay for that breadth. Evergreen coverage like this is aimed at giving you a stable reference point, separate from short term headlines, so you can focus on what the current price may or may not reflect.

- On our internal checks, Intuit scores a 5/6 valuation score. Next we will walk through the standard valuation approaches that feed into that result, before finishing with a way of thinking about valuation that can sometimes be even more useful than any single model.

Find out why Intuit's -8.1% return over the last year is lagging behind its peers.

Approach 1: Intuit Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth by projecting its future cash flows and then discounting those back to today’s dollars. It is essentially asking what all those future cash flows are worth right now.

For Intuit, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about US$6.3b. Analysts have supplied several years of forecasts, and these are extended further out by Simply Wall St to build a ten year path of Free Cash Flow, reaching a projected US$11.8b around 2030, again all in US$.

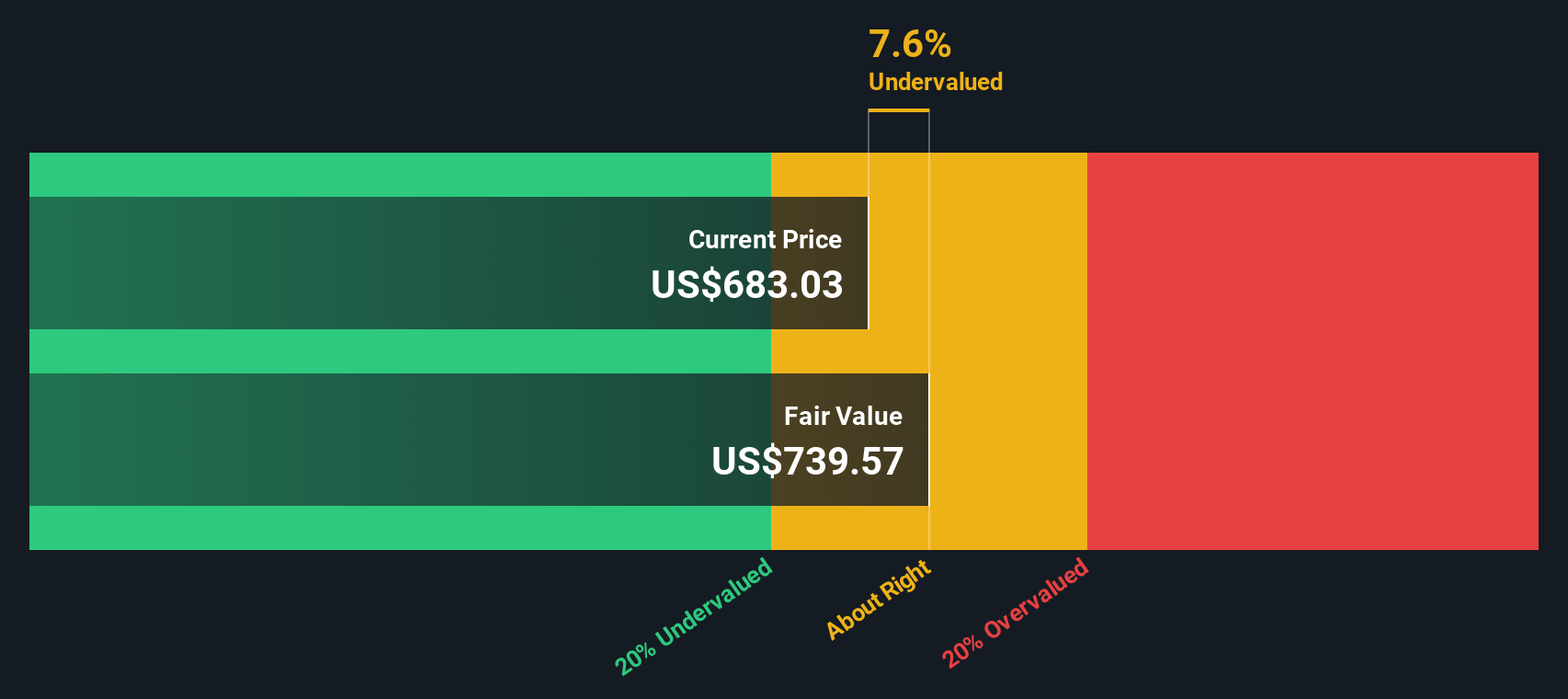

Those projected cash flows are discounted back using the DCF method, which produces an estimated intrinsic value of about US$760.75 per share. Compared with the recent share price of US$554.58, the model suggests the stock is about 27.1% undervalued under this set of assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Intuit is undervalued by 27.1%. Track this in your watchlist or portfolio, or discover 871 more undervalued stocks based on cash flows.

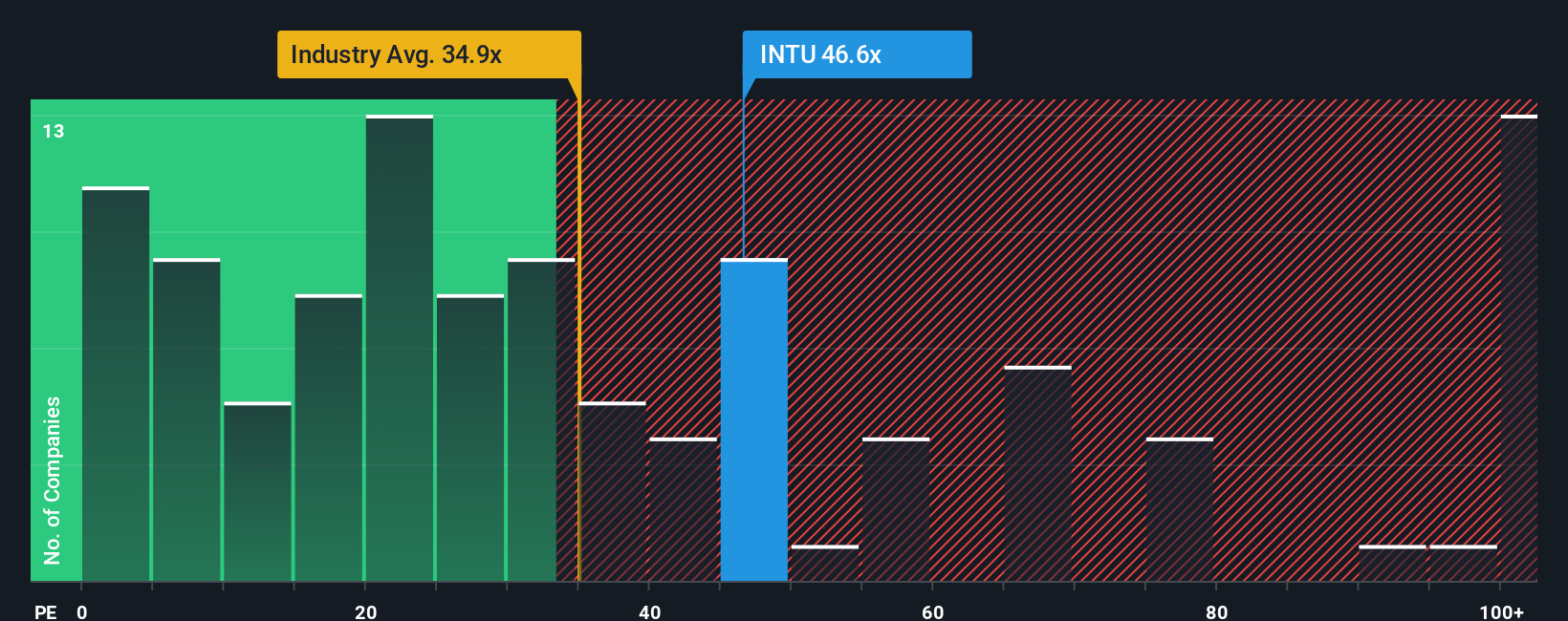

Approach 2: Intuit Price vs Earnings

For profitable companies, the P/E ratio is a straightforward way to link what you pay per share to the earnings the business is currently generating. It helps you see how many dollars investors are paying for each dollar of earnings today.

What counts as a normal or fair P/E usually reflects two things: how quickly earnings are expected to grow and how risky those earnings are perceived to be. Higher expected growth and lower perceived risk can justify a higher P/E, while slower growth or higher risk generally points to a lower multiple.

Intuit currently trades on a P/E of 37.48x. That sits above the broader Software industry average of 31.77x, but below the peer group average of 47.81x. Simply Wall St also calculates a Fair Ratio of 39.20x for Intuit, based on factors like its earnings growth outlook, industry, profit margins, market cap and risk profile. This Fair Ratio is more tailored than a simple comparison with peers or the industry, because it adjusts for the specific characteristics of the company rather than assuming one size fits all. Compared with the current P/E of 37.48x, the Fair Ratio of 39.20x suggests Intuit may be slightly undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Intuit Narrative

Earlier we mentioned that there is an even better way to think about valuation. Narratives on Simply Wall St let you turn your view of Intuit into a clear story that links what you think about its products, AI agents, tax exposure and Credit Karma to a specific forecast for future revenue, earnings and margins. This then flows through to a fair value you can compare with the current price to decide whether the stock looks attractive or expensive, all within an easy tool on the Community page that updates automatically as new news or earnings arrive.

For example, one investor might build a Narrative that leans into AI adoption, the OpenAI deal and analyst assumptions that revenue grows around 12.8% a year with margins in the low 20s and a fair value near US$797 per share. Another might focus more on Mailchimp softness, international headwinds and cautious P/E assumptions, arriving at a lower fair value closer to the bearish analyst target of US$600. You can see both side by side and decide which story, and which fair value, feels closer to your own view.

Do you think there's more to the story for Intuit? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INTU

Intuit

Provides financial management, payments and capital, compliance, and marketing products and services in the United States.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3450.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.3% overvalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.651.0% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£163.7% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

DI

Didier_Lambert_private_inv on Novo Nordisk ·

Relatively mispriced taken into account its intrinsic growth profile, providing a defensive, cash-generative entry point for investors

Fair Value:DKK 35019.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36035.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IS

iStock on Cboe Global Markets ·

Cboe Global Markets will thrive with a future PE of 28.91x leading to growth

Fair Value:US$241.959.6% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.2% undervalued

56 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.3% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

AC

ACV on Alignment Healthcare ·

high medical loss ratios, and negative free cash flow signal that scaling profitably remains elusive...

0

|0