Advertisement

- United States

- /

- Software

- /

- NasdaqGS:INTU

Is Intuit Fairly Priced After Latest Product Launches and Five Year 88% Gain?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have ever wondered whether Intuit stock is fairly priced or has hidden value, you are not alone, especially with the tech sector constantly in motion.

- Intuit’s share price has seen some modest movement lately: down 0.4% over the last week, slipping 5.2% in the past month, but still up 4.1% year-to-date and delivering an impressive 88.1% gain over the last five years.

- Recent headlines have ranged from product launches aimed at expanding Intuit's small business platform to strategic acquisitions designed to strengthen its cloud presence. These moves have caught the attention of both investors and analysts, providing useful context for understanding the company’s recent price moves.

- When it comes to valuation, Intuit currently scores a 3 out of 6 on our valuation checks, suggesting a mix of strengths and stretches. Stick around as we break down what goes into that number and why there may be a smarter way to think about the stock’s true value.

Find out why Intuit's 2.5% return over the last year is lagging behind its peers.

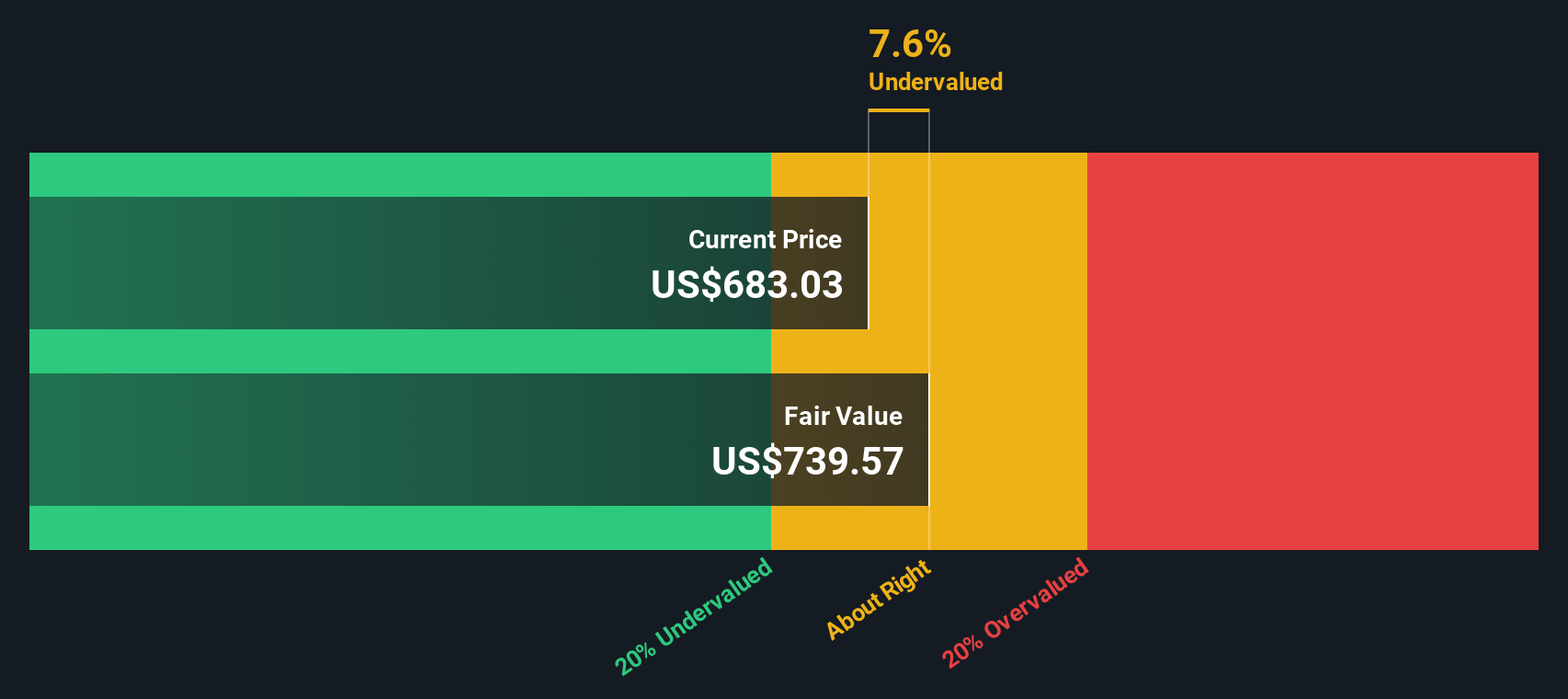

Approach 1: Intuit Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and then discounting those estimates back to their value today. This approach seeks to estimate what all of Intuit’s future profits are worth in today's dollars, giving investors a sense of whether the stock price fairly reflects the business’s earning power.

For Intuit, the 2 Stage Free Cash Flow to Equity model was used, based on cash flow projections. The company’s trailing twelve-month Free Cash Flow stands at $6.3 Billion. According to available forecasts, analysts expect Intuit’s annual Free Cash Flow to grow, reaching approximately $11.7 Billion in 2030. Up to five years of estimates are analyst-driven; further into the future, projections are based on Simply Wall St’s extrapolations.

After crunching the numbers, the DCF analysis yields an intrinsic per-share value of $762.73. Compared to the current market price, this implies Intuit is trading at a 15.0% discount. This suggests the stock may be undervalued by the market right now.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Intuit is undervalued by 15.0%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

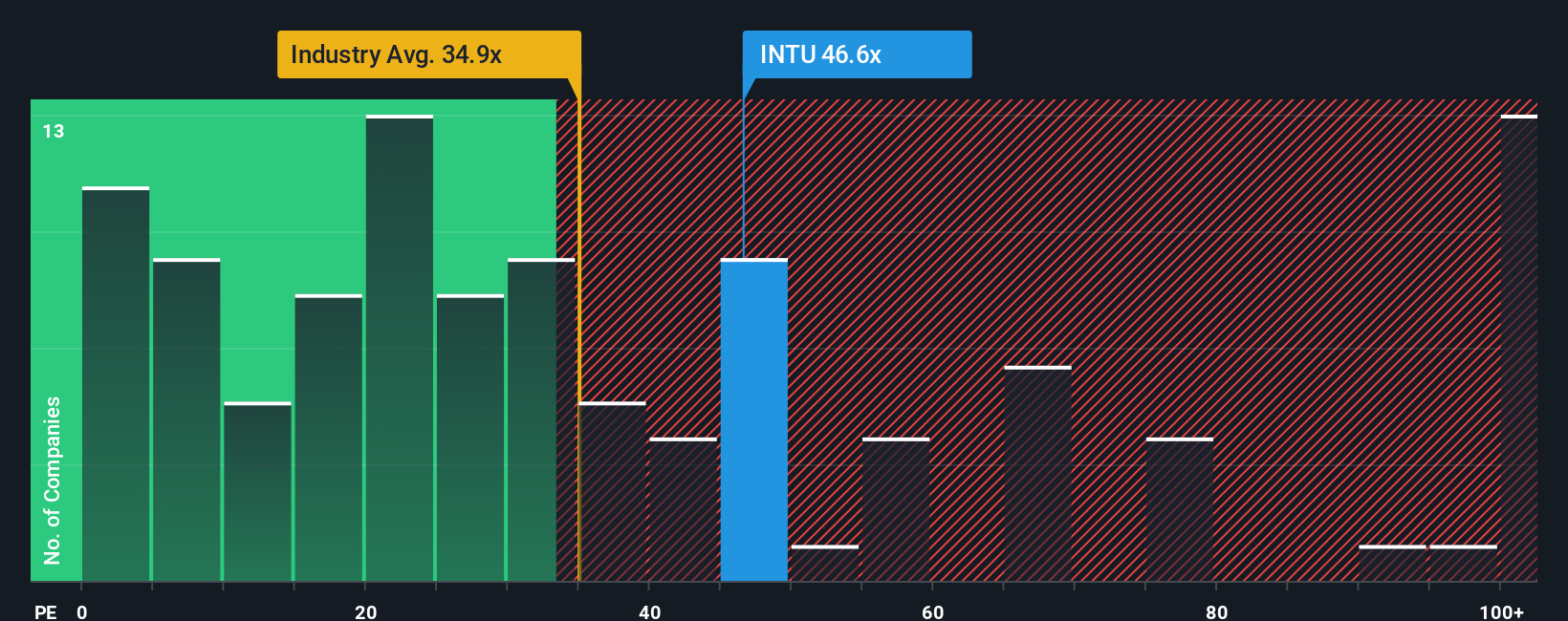

Approach 2: Intuit Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used metrics for valuing profitable companies like Intuit because it relates a company’s share price to its current earnings. It is especially useful for established technology firms, where consistent profits make earnings a reliable gauge of value.

Determining what constitutes a “normal” or “fair” PE ratio depends on expectations for growth and the amount of risk investors are willing to take on. Higher growth companies typically justify higher PE ratios, while increased risk can hold the ratio down, even if the company is profitable.

Currently, Intuit trades at a PE ratio of 43.8x. That is noticeably higher than the Software industry average of 29.8x and the average among peers at 48.8x. Looking deeper, Simply Wall St’s proprietary “Fair Ratio” for Intuit is 43.0x, which is specifically calculated for the company based on its growth outlook, profit margin, industry position, and market capitalization.

The “Fair Ratio” goes beyond traditional comparisons to industry or direct competitors by factoring in what truly drives long-term value for shareholders, such as unique growth characteristics, profitability, sector trends, and scale. This approach can often provide a more tailored and accurate view of whether a stock is trading at a reasonable price.

Comparing Intuit’s current PE of 43.8x with its Fair Ratio of 43.0x, the difference is slight, suggesting the stock is trading at close to its intrinsic value based on these key factors.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1435 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Intuit Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple, story-driven approach that allows you to express your own perspective about a company, connecting your beliefs about its future—such as how fast revenue and earnings might grow and what margins are achievable—with a quantified financial forecast and a calculated fair value.

Narratives make valuation personal and accessible. Instead of only relying on analyst models or traditional ratios, you outline your story about Intuit’s future, then see how your numbers compare with the current stock price. This approach not only links what’s happening at a business and industry level directly to your investing decisions, but also helps you recognize which assumptions drive the biggest differences in value.

Available on Simply Wall St’s Community page, a platform used by millions, Narratives are updated automatically when new news or earnings land, so your investment logic always stays relevant. For example, you might create a bullish Narrative if you think Intuit’s AI innovations and expanding financial services will accelerate earnings, supporting the higher end of analyst price targets. Others may prefer a more conservative Narrative if they see risks in Mailchimp’s performance or international growth, aligning with lower fair value estimates.

Do you think there's more to the story for Intuit? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INTU

Intuit

Provides financial management, payments and capital, compliance, and marketing products and services in the United States.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

84 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

921 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative